Impacts of GST E-Invoicing System

Page Contents

Impacts of E-Invoicing System for businesses under the GST

What is an electronic invoice?

The documentation required for e-Invoicing and reporting to the Invoice Registration Portal (IRP):

- The supplier’s credit notes,

- Debit notes from retailer,

- Invoices from suppliers

- A specific mention should be disclosed under the statute, or any other necessary document, by a specific mention.

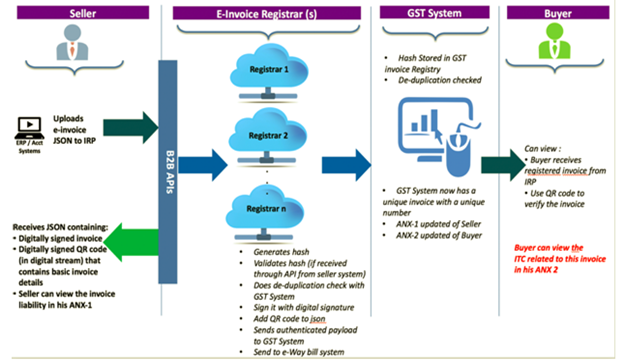

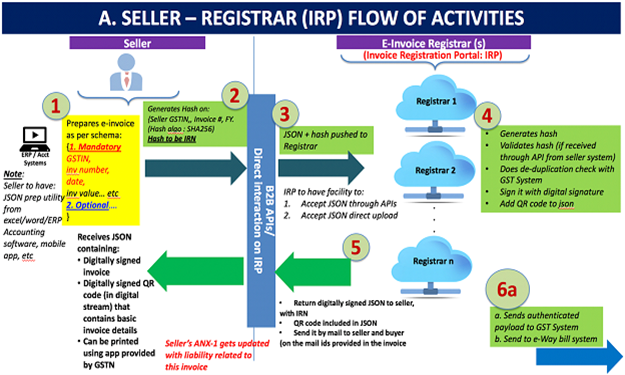

Workflow of invoice

-

Interaction between supplier/seller with IRP & GST/E-Way Bill System

Step 1:

- The invoice is created by the billing or accounting software of the Seller. This can be proprietary or third-

- party software that is aligned with the Standard of GST e-Invoice requirements or those using the utility program offered by EXCEL or GSTN.

- It needs to have the appropriate parameters/fields req. By the laws of the GST Council, if not the optional ones. And most significantly, to submit to the IRP, the seller’s program must be able to create a JSON of the final invoice.

- JSON is a text format in which data between servers flows. You can later reconvert this text format to JAVA Script Objects. Only the JSON, not the entire invoice is uploaded.

Step 2:

- An optional step that generates the Invoice Reference Number (IRN) (e.g. SHA256). The generation of IRN-Supplier GST Identification Number, Supplier Invoice Number, and the financial year includes three parameters.

Step 3:

- The seller uploads the JSON of the invoice along with the IRN (if generated) into the IRP. This can be done directly on the IRP or through GSPs-developed third-party applications (GST Suvidha Provider).

Step 4:

-

- To ensure that the same invoice is not repeated in the system, the IRP will validate the hash on the uploaded JSON and check the hash from the Central Register of the Central Registry.

- The Invoice Data adds a signature and the IRP adds a QR code to the JSON.

- This will include the GSTN number of the seller and buyer, invoice number and date, number of line products, major product HSN classified by hash, weight, etc.

- For the e-Invoice, which is unique to each invoice, this hash provided by the IRP will become the final IRN (Invoice Reference Number).

- The uniqueness is kept by maintaining a record in a central repository of invoice hashes.

Step 5:

In the backend, the uploaded data is shared with the server maintained by the GSTN.

Step 6:

along with the QE Code, a digitally signed JSON with IRN is given back to the seller. Also, the registered invoice is sent to both the buyer and the seller by e-mail.

-

Interaction between buyer with IRP & GST/E-Way Bill System

Step 1:

- The GST system and the E-Way Bill System share the JSON of the uploaded e-Invoice along with the IRN.

Stage 2:

- Update of ANX – 1 and ANX 2 with the purchaser automatically by the GST method to evaluate the liability and the sum of the input tax credit.

Step 3:

- Using this information, the E-Way bill system will create Part-A of the E-Way bill to which only the vehicle number should be attached in Part-B of the e-way bill.

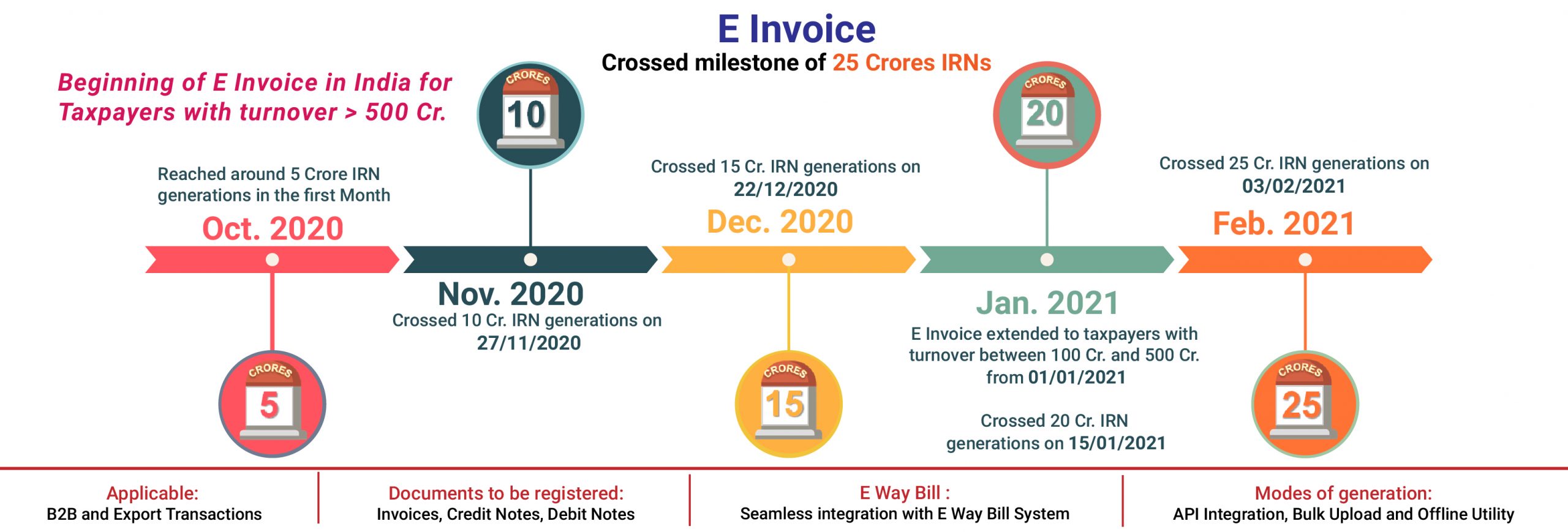

Timeline & Impact of Business Based on Turnover

- The e-Invoice system is scheduled to be carried out on a volunteer basis from January 2020.

- Mandatory complexity of the program will be gradually enforced in phases to bring the entire system acclimatized to the new level of software changes in its accounting standards and business practices.

- Initially, the scheme will be made compulsory for businesses over a specific turnover, on a voluntary basis for everyone else.

- After that, it will gradually become uniformly mandatory.

- It is important to keep in mind that small and medium-sized taxpayers (with an annual turnover below Rs 1.5 Crores) can make use of GSTN’s cost-free financial reporting and billing systems.

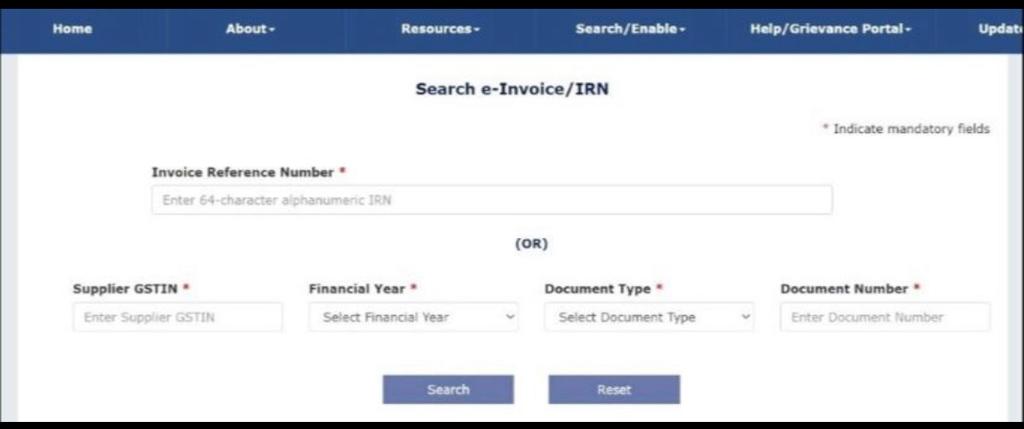

GSTN has enabled the functionality to find the Invoice Reference Number (IRN) Via Document Number

Popular blog:-