CORPORATE AND PROFESSIONAL UPDATE May 4, 2017

Page Contents

Professional Update for the day:

Direct Tax:

- Supreme Court of India held that insertion of Section 35FF makes the provision of Section 35F more balanced because the amount so deposited by the assessee-appellant, will be refunded with interest in case the appeal is allowed in favour of the assessee-appellant and the rate of interest will vary from 5% to maximum of 36% per annum depending upon the notification published by the Central [Satya Nand Jha vs. Union of India and Others (Supreme Court)]

- ITAT Ahemdabad held that the assessee has actually received the salary from his previous employers after deducting the notice period as per the job agreement with them. Therefore, in our considered view, the actual salary received by the assessee is only taxable. [ Shri Nandinho Rebello Vs DCIT]

- Bombay High Court held that the purpose of service is put the other party to notice and to give him a copy of the papers. The mode is irrelevant. The rules and procedure are not so ancient or rigid that only antiquated methods of service through a bailiff or by beat of drum is acceptable. E-Mail & Whatsapp are not formally approved but if service is shown to be effected and is acknowledged it cannot be said that the Defendants had ‘no notice’. Defendants who avoid and evade service by regular modes cannot be permitted to take advantage of that evasion. [Kross Television India Pvt. Ltd. Vs Vikhyat Chitra Production]

Indirect Tax:

- CBEC has issued a circular vide circular no. 16/2017-Customs dated 2nd april, 2017 regarding monitoring of export obligation fulfillment under EPCG and Advance Authorisation Schemes.

- CESTAT Delhi held that, as the relevant provisions (namely section 62 (25a), Section 65 (105)(zzze) and Section 66 of the Act), to the extent these provisions purport to levy service tax in respect of services provided by a club of association to its members is declared ultra vires. Hence, there are no operative legislative provisions of the Act legitimising the levy and collection of service tax from the appellants, for providing Club or association service, in so far as these relate to any services provided to members of these appellants.[M/s DLF Recreational Foundation Ltd. Vs CST, New Delhi]

- Chhattisgarh High Court is of the considered opinion that there is no willful suppression of facts to evade tax on the part of the petitioner and it was bona fide on the part of the petitioner, it was not deliberate and in absence of finding relating to mensrea recorded by the Settlement Commission, the penalty imposed upon the petitioner under Section 78 of the Finance Act, 1994 deserves to be quashed. [Mahadev Logistics, Vs Customs and Central Excise Settlement Commission]

- Services performed in India for a service recipient located abroad are export of services provided recipient does not have any branch or project or business establishment in India and payment for the service has been received in convertible foreign exchange: Gap International Sourcing (India) Pvt. Ltd. Vs. CST- CESTAT NEW DELHI]

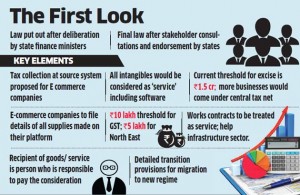

GST Updates:

IGST, CGST, SGST deposited cannot be adjusted against each other. Only IGST, CGST & SGST input tax credit can be adjusted in specified order.

Key dates:

- E- Payment of service tax for April by Cos: 06.05.2017

- Submission of forms received in April to IT Commissioner: 07.05.2017

- Payment of TDS/TCS deducted/collected in April:07.05.2017

- Return of non – SSI assesses for april:10.05.2017

- Return by units paying duty > 1 crore (CENVAT + PLA) for April: 10.05.2017

FAQ on GST

What are the major features of the proposed payment procedures under GST?

Answer: The major features of the proposed payments procedures under GST are as follows:

- Electronic payment process- no generation of paper at any stage

- Single point interface for challan generation- GSTN

- Ease of payment – payment can be made through online banking, Credit Card/Debit Card, NEFT/RTGS and through cheque/cash at the bank

- Common challan form with auto-population features

- Use of single challan and single payment instrument

- Common set of authorized banks

- Common Accounting Codes

Other Updates

- NCLT: Company petition filed by authorized signatory is maintainable where the source of authorization letter is the shareholders’ resolution and the authorized signatory is competent to file company petition. BUHARI ABDUL KHADER KHALID vs. EMIRATES TRADING LLC. CHENNAI BENCH.

- RBI invites applications for Direct Recruitment for the posts of Officers in Grade ‘B’ (General) – DR, DEPR and DSIM in Common Seniority Group (CSG) Streams – 2017. visit rbi.org.in

Quotes of the Day:

“When we give cheerfully and accept gratefully, everyone is blessed.”

“Our character is what we do when we think no one is looking.”

We look forward for your valuable comment www.carajput.com

FOR FURTHER QUERIES CONTACT US:

W: www.carajput.com E: singh@carajput.com T: 011-233-4-3333, 9-555-555-480