CORPORATE AND PROFESSIONAL UPDATE FEBRUARY 25, 2016

Page Contents

CORPORATE & PROFESSIONAL UPDATE DATED FEBRUARY 25, 2016

INCOME TAX ACT

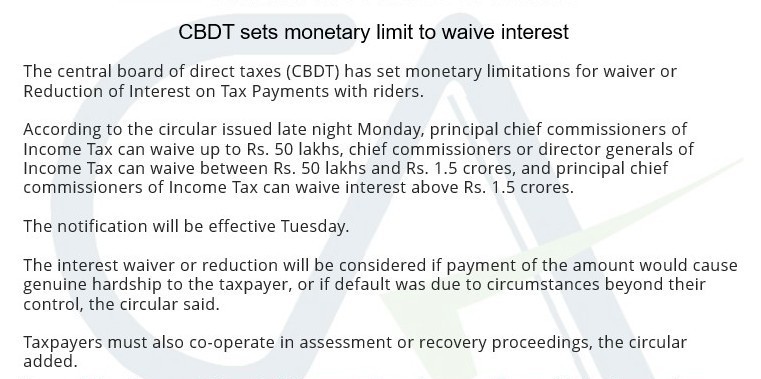

CBDT sets monetary limit to waive interest

SECTION 4

CHARGEABLE AS INCOME

General principle : Tax cannot be levied on assessee at a higher amount or at a higher rate merely because assessee, under a mistaken belief or due to an error, offered income for taxation at that amount or that rate –[2016] 66 taxmann.com 181 (Rajkot – Trib.)

SECTION 92C

TRANSFER PRICING – COMPUTATION OF ARMS LENGTH PRICE

Comprarables and adjustments/Comparables – Illustrations : Where on FAR analysis conclusion that a company is correctly chosen as a comparable remains unassailed, then it is necessary for revenue at that stage to bring some cogent reason, argument or fact justifying that still comparable needs to be excluded

Comparables and adjustments/Comparables – Illustrations : Where assessee (Semco) had provided a comparable summary of FAR analysis undertaken by Semco and Sigma, an overseas enterprise, to show that Semco was less complex entity and in earlier and later years, Semco was taken as tested party, there was no justification for taking Sigma as tested party for benching international transaction

Comparables and adjustments/Safe Harbour rule : Amendment to proviso to section 92C being applicable with effect from 1-10-2009, will have no bearing on benefit of +/- 5 per cent safe harbour given to assessee for year 2005-06

SECTION 220

COLLECTION AND RECOVERY OF TAX – WHEN TAX PAYABLE AND WHEN ASSESSEE DEEMED IN DEFAULT

Waiver of interest : Where order of Commissioner (Appeals) allowing registration to assessee firm was reversed by Tribunal, benefit of waiver of interest in respect of section 220(2) would be allowed up to period provided in this order of Tribunal and it could not be restricted up to date of order of jurisdictional High Court in another case on similar issue

SECTION 268A

FILING OF APPEAL OR APPLICATION FOR REFERENCE BY INCOME-TAX AUTHORITIES

Circular No. 21/2015 : Where tax effect in revenue’s appeal before High Court was below than prescribed monetary limit of Rs. 20 lakhs as per circular No. 21/2015, dated 10-12-2015, appeal was liable to be treated as dismissed as withdrawn

Circular No. 21/2015 : CBDT Circular No. 21/2015, dated 10-12-2015 will apply to pending appeals also

COMPANIES ACT

SECTION 445

WINDING UP – COPY OF ORDER TO BE FILED WITH REGISTRAR

In case of winding up of company, relevant date for computing workmen’s dues will be date of winding up as per section 445(3) and not date of appointment of Official Liquidator

SECTION 529A

WINDING UP – OVERRIDING PREFERENTIAL PAYMENTS

Dues of secured creditors including banks and workers have priority over all other debts including claim of Excise Department – [2016]

SERVICE TAX

SECTION 65(27)

TAXABLE SERVICES – COMMERCIAL TRAINING OR COACHING SERVICES

Flying training services provided by an approved flying training institute are not liable to service tax, as services fall within meaning of ‘qualification recognized by law’

CUSTOMS ACT

SECTION 132

OFFENCES AND PENALTIES – CUSTOMS

Where assessee has been exonerated in adjudication proceedings on merits and charge of holding/importing ‘prohibited goods’ or charge of evasion has been dropped on merits, criminal prosecution cannot continue on same set of facts

CENVAT CREDIT RULES

RULE 5

CENVAT CREDIT – REFUND OF

Provision of onsite services by overseas branch for which payment is received in India in convertible foreign exchange would amount to ‘export of service’ and would form part of ‘export turnover’ as well as ‘total turnover’ in determining cenvat refund under rule 5 of CENVAT Credit Rules, 2004

STATUTES

DIRECT TAX LAWS

Guidelines for Power Generation, Transmission and Distribution in Special Economic Zones (SEZs)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances; Hope the information will assist you in your Professional endeavors. For query or help, contact: singh@carajput.com or call at 011-233 433 33

You may like a few other posts