CORPORATE AND PROFESSIONAL UPDATE FEBRUARY 26, 2016

Page Contents

CORPORATE & PROFESSIONAL UPDATE FEBRUARY 26, 2016

Direct Tax

- When the issue has been decided by the CIT(A) then only CIT(A) can rectify the order u/s 154, AO has no jurisdiction to rectify such order – Tribunal.[M/s. NHPC Ltd. vs Asstt. Commissioner of Income Tax, Circle-II, Faridabad And vica-versa – 2016 (2) TMI 676 – ITAT DELHI]

- Section 292C inter alia provides that where any books of accounts or other documents are found in possession or control of any person in the course of search u/s 132 or survey under Section 133A of the Act it may be presumed that such books or documents belong to such person. Undisputedly such presumption is rebuttable- (PR. Commissioner of Income Tax Versus M/s Delco India Pvt. Ltd. – 2016 (2) TMI 607 – DELHI HIGH COURT)

- Loss on revaluation of investments – valuation of stock in trade – the securities of the Banks are investment and have to be valued at costs or market price whichever is less – claim of loss allowed- (The Commissioner of Income Tax (Large Tax Payer Unit) Versus M/s Union Bank of India – 2016 (2) TMI 606 – BOMBAY HIGH COURT)

- IT:Expenses allowable as revenue expenditure u/s 37 – there is no concept of deferred revenue expenditure in the Act except under certain specified sections where amortization is specifically provided. Normally the ordinary rule would be that the revenue expenditure incurred in a particular year is to be allowed in that year – CIT Vs. Vadilal Enterprises Ltd (2016 (2) TMI 631 Gujarat High Court)

- IT:Non-deduction of tax at source u/s 194H – non-cash payment to dealers – impugned proceedings were beyond prescribed time limitation and thus the same deserve to be annulled – ACIT 51(1), New Delhi Vs. Samsung India Electronics (P) Ltd (2016 (2) TMI 629 ITAT Delhi)

- No disallowance of penalty paid for procedural non-compliances. [Mangal Keshav Securities Limited vs. ACIT (ITAT Mumbai)]

- No charity in initial years cannot be sole basis for trust registration denial.[M/s Prabhat (A House of Hope for Special Children) vs CIT (Exemptions), (ITAT Chandigarh)].

- Expenses can be allowed once business is setup despite it’s non-commencement. [M/s. Multi Act Realty Enterprises Pvt. Ltd. vs. ITO (ITAT Mumbai)]

- Section 54EC deduction allowed if cheques presented within 6 months. [Neela S. Karyakarte vs ITO (ITAT Mumbai)].

- No reassessment on ground that assessee didn’t offer any disallowance under sec. 14A in respect of tax free income

Indirect Tax

- Services having indirect nexus with business are Input services. [Sudarshan Chemical Industries Ltd. vs. CCE Appeals (CESTAT Mumbai)]

- Export benefit cannot be denied on re-processed damaged goods. [M/s Uniworth Textiles Ltd. Vs. Commissioner of Central Excise, Nagpur (CESTAT Mumbai)]

- No CENVAT reversal under Rule 6 on SEZ supply with effect from 10/09/2004. [Commissioner of Central Excise vs. M/s. Mather Platt Pumps Ltd. (CESTAT Mumbai)]

- Testing cost of returnable durable cylinders not includible in AV. [M/s Bombay Oxygen Corporation Ltd. vs. Commissioner of Central Excise (CESTAT Mumbai)]

- Mandatory recovery of advertising cost should be included in AV. [M/s Rathi Transpower Pvt. Ltd. vs. Commissioner of Central Excise (CESTAT-Mumbai)]

- Demand of service tax on management, maintenance or repair service collected from flat owners, in this fact the appellant is not liable for service tax – Tribunal.[M/s Omega Associates vs Commissioner of Service Tax, Mumbai – 2016 (2) TMI 690 – CESTAT MUMBAI]

- Business Auxiliary Service – Activity of maintaining complete Toll Operation supply of Man Power and maintenance of Toll Collection System including Plaza maintenance etc. – NHAI is not running any business – Activity is not taxable – Shri Jivanlal Joitaram Patel Versus Commissioner of C. Ex. & Service Tax, Ahmedabad-III – 2016 (2) TMI 611 – CESTAT AHMEDABAD)

- Whether a single Member of the Appellate Tribunal Value Added Tax (AT) can legitimately function as the AT in terms of Section 73(1) of the Delhi Value Added Tax Act 2004 – Held Yes – HC – Bharat Bijlee Limited. Versus Commissioner of Trade & Taxes, Govt. of N.C.T. of Delhi & Others – 2016 (2) TMI 655 – DELHI HIGH COURT)

Service Tax And Excise Laws

- ST: Refund of un-utilized CENVAT Credit – the assessee is not a registered C.E. or S.T. assessee and therefore cannot come under the purview of CENVAT Credit Rules 2004 and therefore cannot claim refund under Rule 5 of the Cenvat Credit Rules 2004 – Shams Healthcare Software Pvt Ltd Vs. CCE&ST, Nagpur (2016 (2) TMI 658 CESTAT Mumbai)

- ST: CBEC has amended the negative list e.f. 1st April, 2016 to exempt services provided by Govt. or a Local Authority to a business entity with a turnover up to rupees ten lakh in the preceding financial year from ST leviable thereon under Section 66B of the said Act.

- RBI:RBI has decided to upward revise the threshold for monitoring and reporting of frauds in NBFCs from Rs. 25 Lac to Rs. 1 Crore with immediate effect.

- Leading bourse National Stock Exchange (NSE) today said that ‘one person company’ can act as stock broker provided the entity has at least two directors.

- However, such broker would not be allowed to trade in his proprietary account.

- “One Person Company (OPC) as described under the Companies Act is eligible to be registered as a stock broker, provided it satisfies the condition of minimum two directors, as stipulated under…Securities Contract (Regulation) Rules, 1957,” NSE s ..

- Partial recovery of rent of leased vehicles from employees couldn’t be chargeable to ST under ‘renting services’.

- CENVAT credit on foreign commission to foreign agent allowed. [Monarch Catalyst Pvt. Ltd. vs. Commissioner of Central Excise (CESTAT-Mumbai)]

- CENVAT of Inputs & Input services for producing electricity captively consumed allowed. [M/s JSW Steel Coated Products Ltd. vs. CCE (CESTAT Mumbai)].

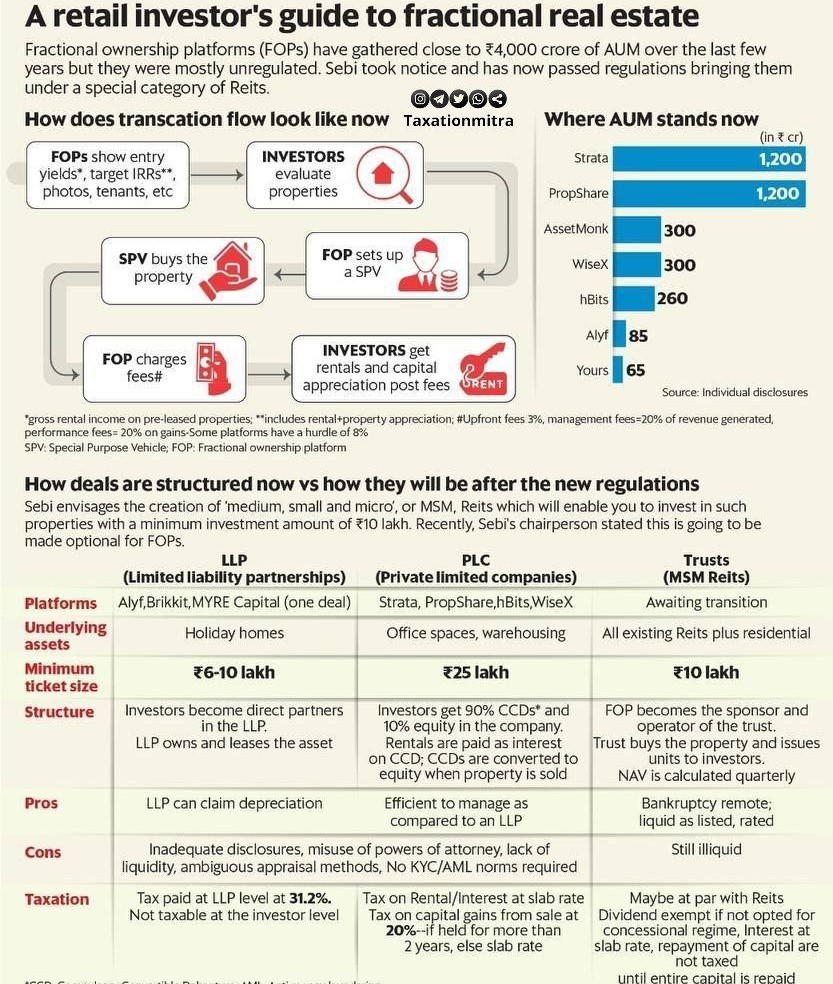

SEBI – Fractional Ownership, Accommodating Larger Platforms

Securities and Exchange Board of India’s approval for MSM Reits formalizes fractional ownership, accommodating larger platforms like Strata & PropShare and smaller investors via structures like ALYF & Brikkit, offering opportunities in India’s commercial real estate sector.

FAQ on Company Law

Query: We have a query regarding the Board meeting of a Small company. As peCr SectioCn Small company.173(1), every company is required to hold 4 Board meetings in a year while Section 173(5) provides that OPC, Small companies & Dormant companies are required to conduct one meeting in each half of the calendar year and gap between two meetings should not be less than 90 days. Does it mean that Small Company cannot hold two Board meetings within a period of 90 days?

Answer: This is an optional provision which gives an option to the Small companies to either conduct minimum four Board meetings in a year and maximum gap between two consecutive meetings cannot be more than 120 days as per Section 173(1) of Companies Act 2013 or conduct one meeting in each half of the calendar year and gap between two meetings should not be less than 90 days as per Section 173(5) of the Companies Act 2013.

However, it does not mean that a company cannot hold two Board meetings within a period of 90 days. But if it holds two meetings within a period of 90 days, it has to comply with Section 173(1) of the Companies Act 2013.

Banking & Corporate Laws

- SFIO is solely empowered to investigate into affairs of co., it supersedes over other investigations under Cos Act: HC

- Director can’t run parallel business to compete with own Co. due to her animosity against co-director

- Deduction u/s 80-IA-Whether the Tribunal was right in holding that the deduction under Section 80-IA is not allowable at all to the assessee since there was no taxable income though the unit eligible for deduction had net profit-Held Yes – Sanra Software Ltd.vs. DCIT, Chennai (2016 (2)TMI 574 Madras High Court).

- Registration petition u/s 80G(5) is denied where assessee is not an institution expressed to be for the benefit of any particular religious community or caste u/s 80G(5)(iii) or having any purpose the whole or substantially the whole of which is of religious nature under explanation 3 there in –Tribunal .[Shri Yamunaji Mandir , Trust –Moviya vs Commissioner of Income Tax-I-2016(2)TMI 569 ITAT RAJKOT]

- Interest from surplus fund is taxable as income from other sources. [M/s Himalayan Expressway Limited vs. ITO (ITAT Chandigarh), ITA No. 690/ Chd/2014, AY 2009-2010]

- Securities Premium is not accumulated profits u/s 2(22)(E): ITAT.[M/s Jeans Knit Pvt. Ltd. vs. ACIT (ITAT Bangalore ), ITA No.1105/Bang/2013 & ITA No. 1244/Bang/2013, AY 2008-09].

- Daughter have equal rights in parents property prospectively: SC. [ Prakash & Ors vs. Phulavati & Ors (Supreme Court), Civil Appeal No.7217 of 2013 & others.].

- Debentures, whether fully or partly or optionally convertible, are nothing but debt till the date of conversion and any interest paid on these debentures is allowable as normal business expenditure – [ITAT Delhi in case of DCIT, New Delhi Vs. M/s Alcobex Metals Ltd.]

- Expenditure incurred on the issue of Foreign Currency Convertible Bonds (FCCB) is revenue expenditure allowable under section 37(1) of the I.T. Act –Gati Ltd. vs. ITO , W -2(2)Hyderabad (2016 (2) TMI 404 ITAT Hyderabad).

- Non TDS deduction disallowance is not sustainable if payee discharges his tax liability. [Kurian Ulahannan Moothukuzhi yil vs. ITO (ITAT Ahmedabad), I.T.A. No.2524/Ahd/2014,AY 2010-11]

- Penalty u/s 271AAA is not tenable where no search was conducted.[DCIT vs. M/s Sam India Abhimanyu Housing (ITAT Delhi) ITA No.1257/Del./2015,AY2011-2012.

- Supreme Court on deemed registration u/s 12AA in case 6 months deadline in not adhered to( SOCIETY FOR THE PROMN. OF EDN. CASE).& another case is Delhi High Court on reopening u/s 148 on quality of reason & live link requirement (in SABHARWAL PROPERTIES case) .

- Exempts services provided by Government or local authority to a business entity with a turnover up to rupees ten lakh in the preceding financial year w.e.f.1.4.2016-Notification No. 07/2016- Service Tax dated 18th February,2016 Department of Revenue.)

- CENVAT credit eligible on furniture & fittings used for output service.[ICICI Lombard General Insurance Company Ltd. vs. Commissioner of service Tax [Mumbai CESTAT].

- All the services provided by the Government or local authority to a business entity, except the services that are specifically exempted,or covered by any another entry in the Negative List ,shall be liable to service tax w.e.f. 1.4.2016-Notification No.06/2016-Service Tax ,dated 18th February ,2016 Department o revenue.

- Sebi prohibits an Auditor from issuing any certificates required under securities laws, directly or indirectly .

- Union Bank of India invites applications from CA firms for concurrent audit of its branches. Start date 22.02.2016 end date 05.03.2016.

- The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances; Hope the information will assist you in your Professional endeavors. For query or help, contact: singh@carajput.com or call at 011-233 433 33