Situations Lead To a GST Refund Claims

Page Contents

SITUATIONS WHICH LEAD TO A GST REFUND CLAIMS

What’s the GST refund?

GST refund situation arises when we paid GST is more than the GST liability raised, In the reference GST fund, the process of claiming a GST Refund is standardized to avoid confusion. The GST refund Mechanism is online & deadlines for GSt refund have also been set by the GST department for the same.

What is the GST ARN number?

- the GST ARN No refer to a 15-digit Application Reference Number (ARN) that is recognized by the GST portal while filling the GST Registration application.

- Application Reference Number (ARN) helps to track the status of the GST portal application for registration. If the applicant already knows the number of his application for registration, it is much better, but if the applicant does not know his ARN, then this is the process to know the number of the application.

What is Inverted Duty structure

The term “inverted tax structure” refers to a situation in which the tax rate on purchased inputs (i.e. the GST rate paid on inputs received) is higher than the tax rate on outbound deliveries (i.e. GST rate payable on sales).

| Products | GST on | ||

|---|---|---|---|

| Finished Goods (Output) | Raw Materials (Input) | Finished Goods | Raw Materials |

| Fabric Bag | Non-Woven Fabric | 5% | 12% |

Situations that may lead to a refund of claims

A appropriate GST refund process is necessary for successful tax administration, as trade is encouraged by the release of restricted funds for the modernization, growth & capital needs of a company.

In some situation in which GST refunds can be claimed. Here are some of them. Here are some of them the circumstances which could lead to claims for a refund include:

- The excess tax payment is due to error or omission.

- Exports of Product/Services

- Dealer Exports (including deemed export) goods/services on the basis of a refund or refund

- GST Refund if the embassies buy.

- Supplies to developers and units in special economic zones

- Refund of the accrued input tax credit on account of inverted duty structure

- Refund of pre-deposit if any

- Refund will be arising from court order/judgment/direction and decree of the Appellate Tribunal, Appellate Authority, or any court of law

- Refund of taxes when embassies make purchases

- Finalization of provisional assessment

- Excess payment because of an error

- Refund due to issuance of refund vouchers for taxes paid on advances against which commodities or services haven’t been supplied

- Finalization of the provisional assessment

- Tax refund for international tourists who paid GST on commodities within the country and carried to an international location when they depart India

- Refund of SGST and CGST paid by considering the supply in the course of interstate commerce or trade

- ITC accumulation on the basis that the output is tax-exempt or zero-rated

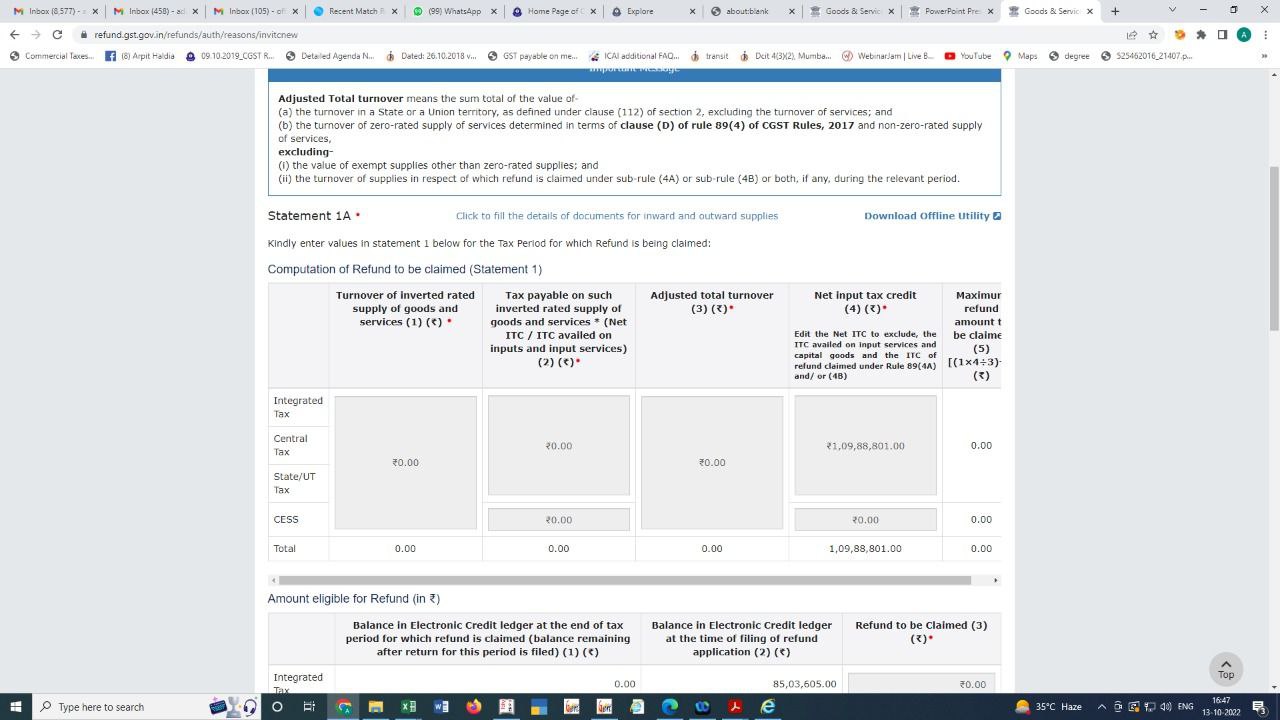

What is Documents Requirement for GST refund application

- Applicants who wish to make a claim will have to submit detailed documents in addition to a refund claim. The documents prescribed for the same are standard documents. Therefore, for each claim, the primary document to be submitted is a statement of the relevant invoices relating to the claim.

- If the refund is made on account of the export of services, not including the invoice declaration, the relevant bank accounting certificates verifying receipt of payment in foreign currency should also be provided.

- In the event that a claim is made by the Supplier to the Special Economic Zones (SEZ) unit, the Authorized Officer will have to confirm receipt of such goods or services in the SEZ and submit the same along with the other documents.

- In addition, the SEZ unit will also have to make a declaration stating that the ITC tax paid by the supplier has not been used.

List of documents required for GST Refund E-Processing-

- Copy of Form RFD 01 A filed on the common portal-

- Copy of Statement 3 A of Form RFD 01 A generated on the common portal-

- Copy of Statement 3 of Form RFD 01 A

- Invoices relating to input and output services-

- BRC / FIRC for export of services-Company / Declaration in Form RFD 01 A

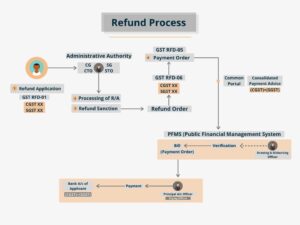

Refund Process under GST

In order to process a refund claim, the following procedure must be followed:

- Visit the GSTN portal and fill in the application form to claim the refund.

- You will receive an email or an SMS containing an acknowledgment number after the application has been filed electronically.

- The Cash and Return Ledger will be adjusted and the “Input Tax Credit Carry Forward” will be reduced automatically.

- The request for a refund, together with the documents you have submitted, will be examined by the authorities for a period of 30 days after the request for a refund has been filed.

- “Unjust enrichment” (explained below) is a concept that will be thoroughly scrutinized by the authorities. In the event that the application is not eligible, the refund will be transferred to the Consumer Welfare Fund (CWF).

- In the event that the refund claimed by the individual exceeds the predetermined amount of the refund, a pre-audit procedure will be carried out before the refund is punished.

- The payment of the refund shall be made electronically to the applicant’s account through NEFT, RTGS, or ECS.

- Individuals are allowed to submit their applications for a refund at the end of each quarter.

- If the amount of the refund is less than Rs.1000, no refund will be granted to the individual.

GST Return filing process in the case of exports sale pursuant:

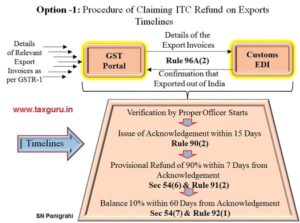

As per New GST Amendment, I has been introduced that the time period from the date of filing of Application on GST Refund under Form RFD 01 till the date of issuance of Deficiency Memo (RFD 03) shall now be removed while computing the limitation period of 2 Year while computing the limitation period of 2 years when a fresh refund application is filed after removal of deficiency.

It is more advantageous for exporters who file their GST Refund application toward the end of the limitation period, i.e. within 2 years after the date of export.

New Formula for Inverted duty Refund reflected on the portal & its reflecting in earlier period refund applications as well.

- Earlier , common ITC was disallowed for Exempt supply including for MEIS sale Now common ITC shall not be disallowed for MEIS sale

- Slight change in Formula in case of INVERTED DUTY STRUCTURE REFUND will increase refund Amt. compare to earlier

Unjust Enrichment

- Due to the fact that GST is an indirect tax structure and that the consumer has to bear its incidence, it is usually assumed that the owner of the business will transfer the incidence of tax to the final consumer.

- For the same reason, any refund claim (excluding specified exceptions) is required to pass the “unjust enrichment” test. If such claims are punished, they shall first be transferred to the Consumer Welfare Fund.

- The test shall not apply to refund of accumulated ITC, a refund of payment of incorrect tax, refund on account of exports, the refund of tax paid on supplies, etc.

- In addition to the above-mentioned incidents, the “unjust enrichment” test must be carried out if the claim amount is to be received by the applicant.

FAQs on GST Refund

Q.1 What if the taxpayer fails to deliver the invoice and invoice within one month, will he add the details in the next month and get the refund?

Ans: Actually, the taxpayer will add the details in the following month and may be refunded.

Q.2 Do GSTR 2 and GSTR 3 Return do have to be filed for refund claims under GST?

Ans: If the Assess have filed GSTR 1 and GSTR 3B, they do not require to fill out any other forms to claim refunds.

Q.3 Is the Assess entitled to receive IGST refunds charged for the export of products if GSTR 3B has been submitted?

Ans: Actually, the taxpayer is entitled to obtain refunds if he has given details of the export products in GSTR 1 Table 6A and has filed GSTR 3B with the related tax details.

Popular blog:-

all you know about documents required under the GST Refund System

Refund mechanism under GST service export

GSTN alerts taxpayers to beware of looking at similar websites and fake messages on GST Refund

Guidance on GST Refund under inverted duty structure in GST