FAQs on Income Tax Return Filling Forms

Page Contents

FAQs on Income Tax Return Filling Forms

Q.1: Does an individual, being an NRI or resident but not ordinary resident (RNOR)), required to disclose details of their directorship in a foreign company not having any income accruing or arising in India?

Ans: Yes.

Q.2: In case unlisted equity shares is acquired or transferred by way of gift, will, amalgamation, merger, demerger, or bonus issue etc., how to report the “cost of acquisition” and “sale consideration” in the relevant column?

In such a case, provide zero value or the appropriate value against “cost of acquisition” or “sale consideration”. It is provided that the details of unlisted equity shares held during the year are required only for the purpose of reporting.

Q.3: Where a person hold shares in an unlisted foreign company which has been duly reported in the Schedule FA, shall be required to report the same again in the column requiring information of unlisted shared held during previous year?

Yes.

Q.4: I have held unlisted equity shares as stock-in-trade of business during the previous year. Whether I have to report the same in the column requiring information of unlisted shared held during previous year?

Yes.

Q.5: what is the reporting requirement as to equity shares of a Co-operative Bank or Credit Societies, that are unlisted?

The taxpayer is required to report the details of equity shares held in any entity which is registered under the Companies Act, and is not listed on any recognised stock exchange.

Q.6: Does sale of land and building to a non-resident require reporting of PAN of buyer in the table A1/B1 in Schedule CG?

It is mandatory for every taxpayer, to quote the PAN of buyer, provided the said transaction requires deduction of TDS under section 194-IA or is mentioned in the documents.

Q.7: whether a resident required to report the details of sale of property held outside India, and identity of buyer in Schedule CG?

It is provided that reporting of details of property and name of buyer is mandatory to be mentioned. However, PAN of buyer be mandatorily quoted, where the same is subject to deducted of TDS under section 194-IA or is mentioned in the documents.

Q.8: Whether details of assets held as stock-in-trade of business, be reported by an unlisted company along with the details of assets and liabilities in the Schedule AL-1 of ITR-6?

In case jewellery/motor vehicle etc. constitutes the stock-in-trade of business, the drop-down value “stock-in-trade” be selected and reported “purpose for which used”. However, the aggregate values be provided.

Q.9: Where the foreign assets held during the previous year has been reported in the Schedule FA, whether same be reported again in the Schedule AL?

Yes.

Q 10: Does an unlisted foreign company required to furnish details of shareholding in the Schedule SH-1 of ITR-6?

Not required.

Q.11: Does an unlisted foreign company required to furnish details of assets and liabilities in the Schedule AL-1 of ITR-6?

Not required.

Q.12: Does a farmer producer company defined under section 581A of Companies Act, 1956, required to furnish details of shareholding in the Schedule SH-1 of ITR-6?

No, however, the applicant shall place a tick for the option ‘Yes’ against the particular “whether the company is a producer company as defined in section 581A of Companies Act, 1956?” in Part-A.

Q.13: does a company required to disclose break-up of only payments and receipts during the year, in foreign currency, as per Schedule FD of ITR-6?

Yes, the taxpayer is required to furnish the break-up of receipts and payments in foreign currency in Schedule FD, only in respect of business operations in India.

Q.14: what is the important of filing income tax returns?

The IT department made it mandatory for all the assessee to file their return, provided their income exceeds the basic exemption limit applicable or where they meet with certain criteria in the form of expenditure on foreign travel being more than Rs 2 lakh or electricity consumption of Rs 1 lakh or more, or deposit of an amount/aggregate of an amount above Rs 1 crore in one or more current accounts and the same be applicable from FY 2019-20 onwards.

Some other benefits of fling ITR are –

- Properly filed ITR acts as a valid proof of income.

- It also helps in getting loans from banks and financial institutions.

- ITR is mandatory documents for applying for credit cards in banks.

- It is also a required document in VISA applications etc.

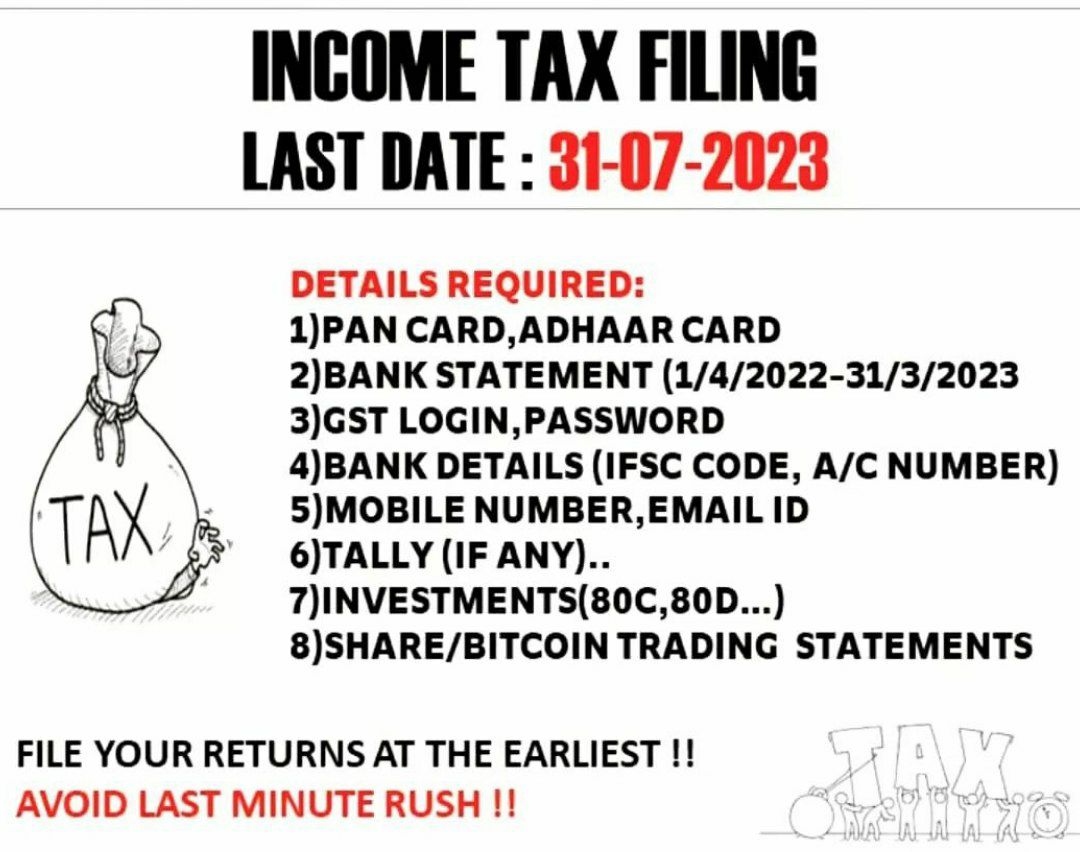

Q.15: what is the procedure for filing ITR online?

The taxpayer is required to pay self-assessment tax before filing of their ITR. In case of salary income, the tax liability is generally deducted from the salary in the form of TDS and the same is paid by the employer to the government.

Where the person is liable to pay advance tax, then an amount equal to 90% of tax liability is required to be paid before the 31st March of the relevant financial year. Once the tax filing window opens, the taxpayer can login into IT portal and can file their return before the applicable due date. However, the due date is extended, the IT department will notify the same by sending a notification.\

For filing return the taxpayer is required to log in to the IT portal https://www.incometaxindiaefiling.gov.in/home and download the excel or java utilities of the ITR form applicable.

After this, a ZIP file will get downloaded and the person can enter their details in that file. After completing the form, the person is required to validate the form, so that the amount of tax gets calculated. Then, the person shall generate and save the XML utility and the said save file be again uploaded on the IT portal for e-filing. Once the form is successfully uploaded, the person is required to verify the same using the options available on the platform.

Q.16: What is the procedure for getting the copy of income tax return filed?

- The person is required to log in to comusing the credentials provided to them.

- Under this, select View Returns/ Form.s

- In that, select the option of “Income tax returns” and choose the relevant assessment year and click submit.

- The portal will redirect to a page, containing the list of ITR filed by the said person.

- On this page, select the ITR-V acknowledgement number and download the file.

- ITR V PDF file will get downloaded and the same will act as the copy of ITR filed.

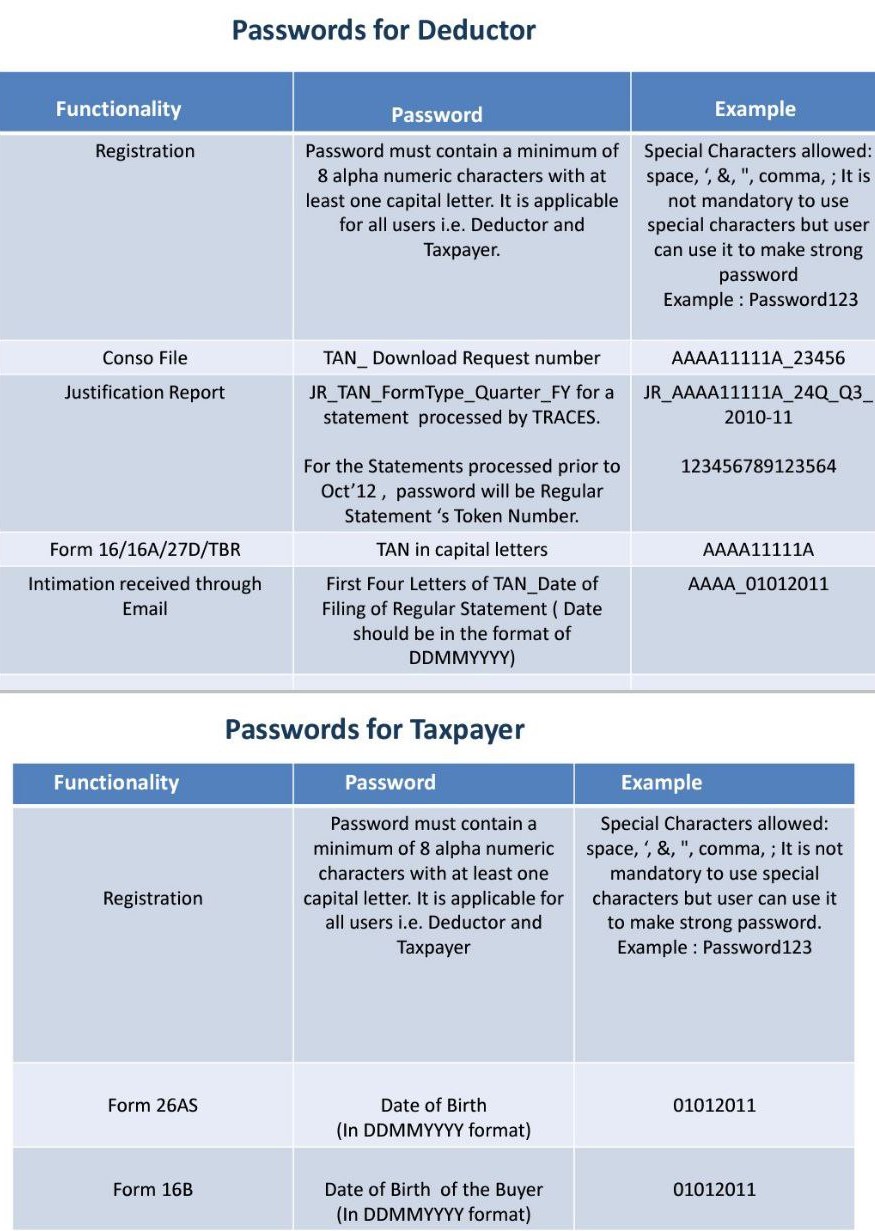

Password Format for Deductor and Tax Payer for Various Services on TRACES Portal

Q.17: You have are 6 way how you can e-verify your Income tax return ?

You have 6 way how you can e-verify your Income tax return :

- EVC generated through e-filing portal:

- EVC generated through Demat Account:

- Sending signed ITR-V/Acknowledgement receipt through post: send it to address -CPC, Post Box No – 1, Electronic City Post Office, Bangalore – 560100, Karnataka, India.

- EVC generated through ATM:

- EVC generated through Net Banking:

- Aadhaar based OTP:

It’s worth mentioning that you don’t needed to send any supporting documentation with your ITR-V. Once the tax department receives your ITR, you will receive an SMS to your mobile number and an email to your email address. This notification is solely for ITR-V receipt. When your tax return is processed, you will receive a separate intimation.

Popular Article :More read for related blogs are:

- All about the Income taxation on capital gain

- Provision-of-capital-gains-charts

- Govt needed to introduce changes in NSP Budget 2021

- All about the Income taxation on capital gain

- Deduction u/s 80CCD of Income Tax Act, 1961

- All about the Income taxation on capital gain

- Delay in the deposit of Employer provident fund during the lockdown

- Aware of the penalty of Section-234f for late filing of ITR

- What is the process of applying instant free pan through adhaar e-KYC

- Basic of aadhar card significance process aadhaar linking with PAN

- Tax Audit

- Implication of cash transaction under income tax Act

- How to file Revised Return of Income Tax E-Filing: Income Tax Department

- Prevent popular errors while filing an income tax return

- Needed to file Income Tax return of Bitcoin profit earned

Contact Us

For query or help, You may find us via email at singh@carajput.com or by phone at +91 9555 555 480, Get in touch with us today to find out more about the services we offer! Call us at +91-9555 555 480. You can contact our NRI tax consultant in India or NRI tax filing services in India, We also offer Taxation compliance & Registration services!