Filling of Form 10-IE for exercise of option in ITR 1&ITR 2

Page Contents

No need to Form 10-IE for exercise/withdrawal of option u/s 115BAC in ITR 1 & ITR 2

- Each individual and Hindu Undivided Family who exercises the option under section 115 AC (The New Tax Regime) is required by Rule 21 AG to submit an application in Form 10-IE via electronic means on their income.

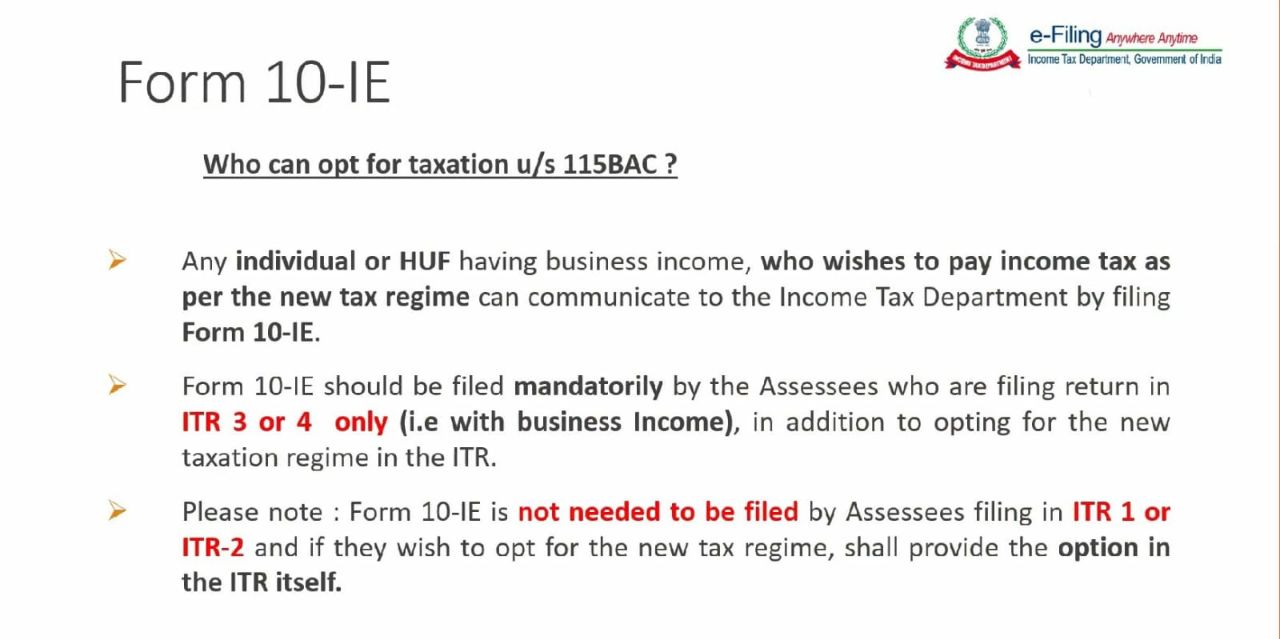

- The Income tax Return filers’ declaration that they have chosen the “New Tax Regime” is made on Form 10IE. If an individual or HUF want to file Form 10IE under the new tax law, they must have business or professional income. They can choose which income tax department to notify by submitting this form.

- On the contrary, taxpayers who do not have business or professional income can simply pick the new regime in the ITR form without submitting Form 10IE.

- Simply expressed, Form 10IE is only required for ITR-3 and ITR-4 filers. Form 10IE is not required from people filing their returns in other Forms like ITR-1 or 2.

Form 10-IE filing is mandatory for exercise/withdrawal of option u/s 115BAC in ITR 3 & ITR 4

- Filing Form 10IE required: Yes, filing Form 10IE is required if you want to use the new tax system and have income falling under the heading “Profits and Gains of Business and Profession.”

- However, a person may exercise an option to opt out of this tax regime under section 115BAC (6) of the Income Tax Act. Every year, a person who does not have a business or a profession can use this choice.

- Note: After exercising the option section 115BAC (6) of the Income Tax Act for the particular assessment year, the Assessee can not be able to withdraw.

How much time do I have to file Form 10-IE?

- As Per Section 139(1) Form 10-IE must be submitted before the return’s due date of ITR,

What is last date of ITR & file Form 10-IE?

- 31st July 2023 is last date of ITR filling

Mandatory Penalty for Late Filing of ITR

Income exceeds basic exemption limit: If the taxpayer’s taxable income exceeds the basic exemption limit, a penalty will be levied for filing a belated ITR. The basic exemption limit depends on the chosen tax regime. The default tax regime is the new tax regime, where income up to Rs 3 lakh is exempted from tax for taxpayers, regardless of their age. Under the Income Tax laws, a late filing fee or penalty is mandatorily applicable if taxpayers miss the ITR filing deadline.

-

Penalty When Income Exceeds the Basic Exemption Limit:

If a taxpayer’s taxable income exceeds the basic exemption limit, they will be subject to a penalty for filing a belated ITR. The basic exemption limit varies depending on the tax regime chosen.

-

Exemption Limits Based on Tax Regime:

The default tax regime is the new tax regime, under which the basic exemption limit is ₹3 lakh, irrespective of the taxpayer’s age. If the taxable income exceeds this limit and the ITR is filed late, the penalty will be imposed.