MSME -Buyer fails to make payment in 45 days ?

Page Contents

MSME-Buyer fails to make payment in 45 days

MSME APPLICABILITY CRITERIA

All manufacturing, service industries, wholesale, and retail traders that fulfil the revised MSME classification criteria of annual turnover and investment can apply for MSME registration. Thus, the MSME registration

MSME registration:

- Individuals, startups, business owners, and entrepreneurs

- Private and Public limited companies

- Sole proprietorship Partnership firm

- Limited Liability Partnerships (LLPs)

- Co-operative societies

- Trusts

Note: It is to be note that Registration under MSME act is not mandatory.

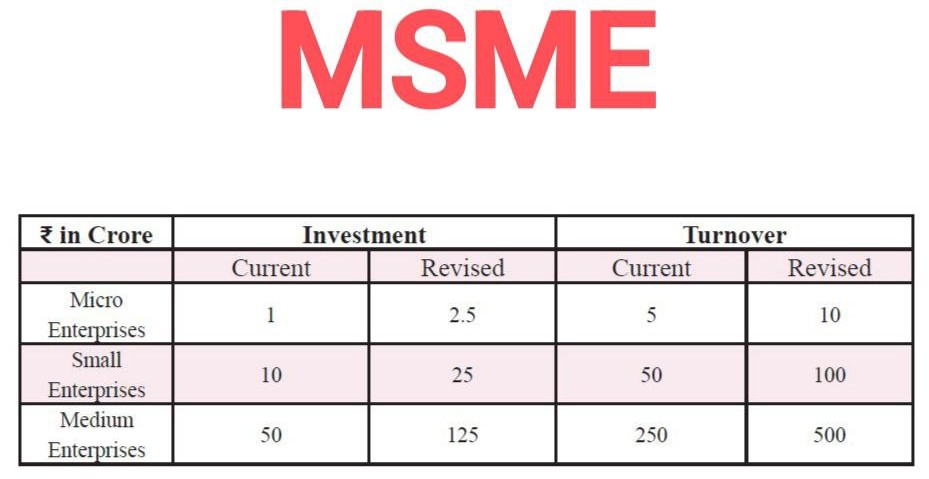

Revised MSME classification criteria of annual turnover and investment

| Revised MSME Classification | |||

| Criteria | Micro | Small | Medium |

| Investment in Plant and

Machinery or Equipment |

Does not exceeds

Rs.1 crore |

Does not exceeds

Rs.10 crore |

Does not exceeds Rs.50

crore |

| Annual Turnover | Does not exceeds

Rs.5 crore |

Does not exceeds

Rs.50 crore |

Does not exceeds Rs.250

crore |

Revision in classification criteria for MSMEs -Budget2025

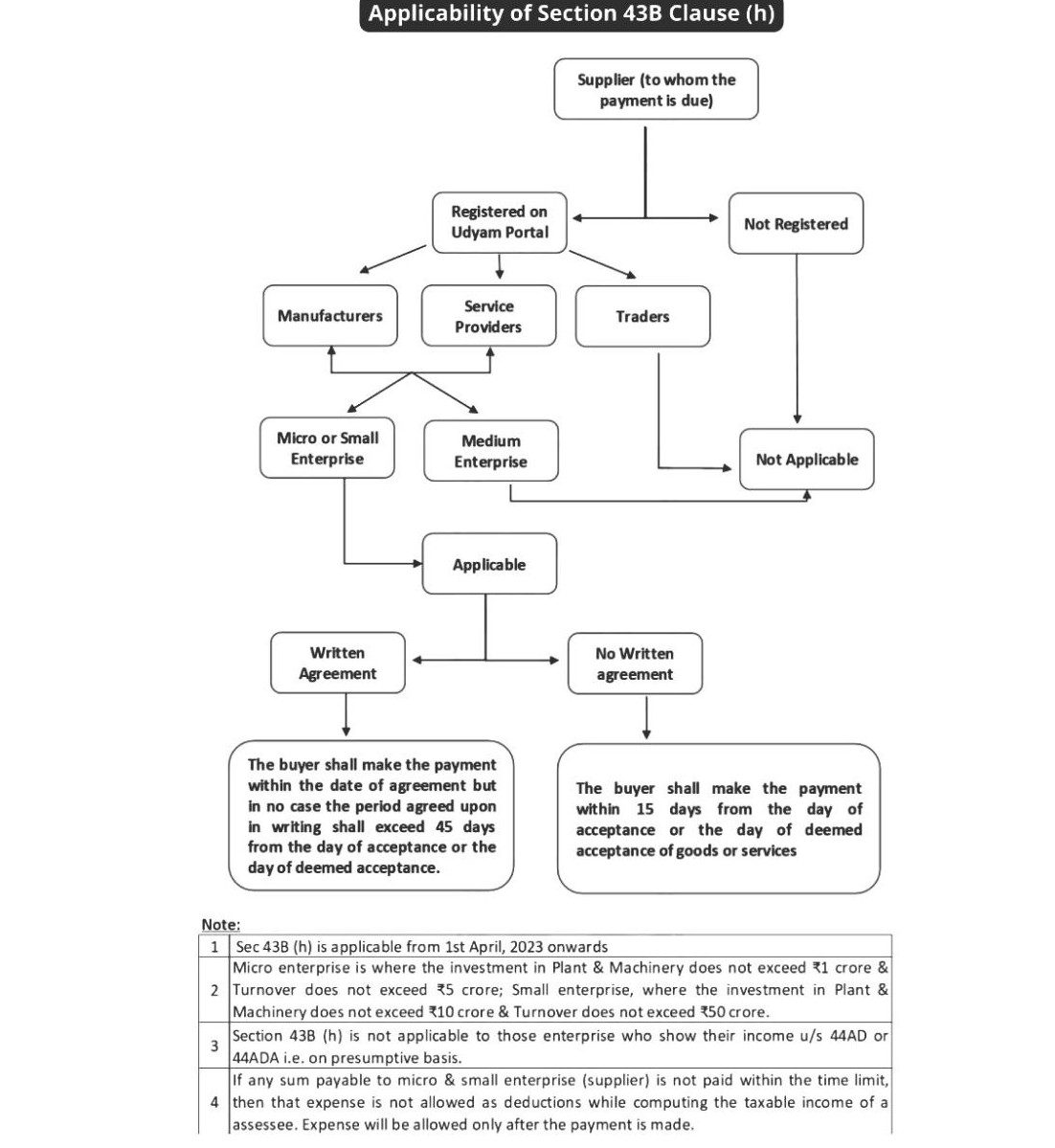

Section 15 of MSME Act, 2006: Liability of buyer to make payment

If written signed agreement is available between buyer and supplier, the buyer should make payment to the supplier of the goods or services within 45 days from the date of acceptance of the goods or services.

Provided that if credit period specified in the agreement between parties exceeds 45 days, then, notwithstanding the agreement, the payment has to be made within the period of 45 days.

Note: If payment made after 45 days but, in the same year of purchase then, in that case deduction shall be allowed in that year itself.

Example to understand the provision.

| Bill Date | Due Date as per

MSME Act (45days) |

Payment Date | Agreement made

with Supplier |

Year of Deduction

of Purchase |

| 15 May 2023 | 30 June 2023 | 31 March 2024 | Yes | FY 2023-24 |

| 15 May 2023 | 30 June 2023 | 3 April 2024 | Yes | FY 2024-25 |

| 1 January 2024 | 15 February 2024 | 15 February 2024 | Yes | FY 2023-24 |

| 1 January 2024 | 15 February 2024 | 31 March 2024 | Yes | FY 2023-24 |

| 1 January 2024 | 15 February 2024 | 10 April 2024 | Yes | FY 2024-25 |

| 20 February 2024 | 5 April 2024 | 5 April 2024 | Yes | FY 2023-24 |

| 20 February 2024

|

5 April 2024 | 6 April 2024 | Yes | FY 2024-25 |

What if buyer fails to make payment in 45 days to supplier registered under MSME?

- Section 16 of the MSMED Act provides that where any buyer fails to make payment to the supplier, as required under section 15, be liable to pay compound interest with monthly rests to the supplier on that amount from the appointed day (the day after expiry of 45/15 days) at 3 times the bank rate notified by the RBI.

- The MSME supplier can also file an application before the Micro and Small Enterprises Facilitation Council (MSEFC) in case of non-payment or delayed payment by the buyer.

Example to understand the provision.

A Ltd purchased goods on credit from B Ltd value Rs. 5,00,000/-. Invoice date 25th February, 2024

| Part Payment made on Following Dates | Allowed as Expenses in the Year | |

| No Agreement Between Buyer & Seller

Due Date: 11th March, 2024 |

Agreement present Between Buyer & Seller

Due Date: 10th April, 2024 |

|

| 1st part – 5th March 2024 Rs. 1,00,000/- | 2023-2024 | 2023-2024 |

| 2nd part – 25th March 2024 Rs 2,00,000/- | 2023-2024 (Int. Payable) | 2023-2024 |

| 3rd part – 10th April 2024 Rs 1,00,000/- | 2024-2025 (Int. Payable)** | 2023-2024 |

| 4th part – 15th April 2024 Rs. 1,00,000/- | 2024-2025 (Int. Payable)** | 2024-2025 (Int. Payable) ** |

**It means that if you fails to pay on due date or till the last date of FY then, interest will payable and purchase/expense will be disallowed as deduction and if payment is made on due date, then no interest liability will get attracted and deduction of purchase/expenses will be allowed in same year but, if payment made after due date and till the last date of FY, then it will result in allowance of such purchase/expense but, interest will be payable on delayed payment.

(Interest payable to the supplier is 3 times of the bank rate notified by the Reserve Bank of India compounding on monthly basis)

Impact on Computation of Total Income

Interest on Delayed Payment

As per section 16 of the MSMED Act, the payment of interest on delayed payment is in the nature of penalty. Therefore, Payment of interest on delayed payment to MSME shall not be allowable as deduction for the purposes of computation of income under the Income Tax Act, 1961.

If, the buyer has claimed such payment of interest as expenses in its statement of profit & loss then, such expenses to be added back to Net Profit while computing the total income under Income Tax Act, 1961.

As per clause 22 of the Tax Audit, Tax Auditor should report the amount of interest inadmissible u/s 23 of the Micro, Small and Medium Enterprises Development Act, 2006 (MSMED, Act 2006).

Delayed payment of Principal

- As per Section 43B (h) of Income Tax Act, 1961, if payments to Micro & Small Enterprises remains outstanding for more than specified time limit** at the end of the financial year (i.e., 31.03.20XX) then, the said amount will be considered as taxable income for the assesse in such financial year.

- The assesse can claim the deduction of the amount declared as income in previous financial year, in the financial year when the payment is made.

** Specified time limit If Written agreement between Buyer & Supplier then, maximum of 45 Days. If No Written agreement between the Buyer & Supplier then, maximum of 15 Days

Changes need to be done in Books of Account by the buyer

From current financial year 2023-24, we need to bifurcate creditors in balance sheet in the following way:

- Creditors of micro enterprises and small enterprises

- Creditors of other than micro enterprises and small enterprises

Compliance Check for all Assesse:

- From the current financial year (2023-24), we need to check bill of each and every party and if they have written UDHYAM no. on their bills then, we need to change HEAD of such creditor account under “Creditors of Micro Enterprises and Small Enterprises”, Rest all creditors should be under creditor of other than Micro enterprises and Small enterprises ?

- From current financial year (2023-24), we need to check bill of each and every party and if they have written UDHYAM no. on their bills then, we need to change HEAD of such creditor account under “Creditors of Micro Enterprises and Small Enterprises”, Rest all creditors should be under creditor of other than Micro enterprises and Small enterprises ?

- We need to send letter to each and every creditor to find out whether they are registered under Udhyam or not and also to all the new creditors. We must have evidence of enquiry with creditors (mail, post, etc.) because it is duty of company.

- If once, we get confirmation from the creditors that they are not registered, and afterward the creditor got himself registered under UDHYAM then it is his duty to inform such thing to company. New and current creditors confirmation is duty of company.

(Caution: Sometimes payment of firms in same group is outstanding, so take care of that as well.)

Creditor is an MSME, and whether its financials need to be reviewed

Many people are confused about how to check whether a creditor is an MSME and whether its financials need to be reviewed. However, it has been clarified in Taxmann’s book on Tax Audit that only a Udyam-registered micro or small enterprise must be considered for section 43B(h)

Essential Compliance Checklist for MSMEs

| Compliance Area | Frequency | Key Deadlines | Summary of Requirements |

|---|---|---|---|

| Udyam Migration | One-time (Mandatory) | Immediate | Migration from the old Udyog Aadhaar (UAM) to the Udyam Portal is mandatory to continue MSME benefits. Old certificates are no longer valid for bank finance, government tenders, or legal protection under the MSMED Act. |

| GST Reconciliation | Monthly | 11th & 20th of every month | Monthly reconciliation of the Purchase Register with GSTR-2B is mandatory. From 2025 onwards, ITC can be claimed only if the invoice appears in GSTR-2B. Missing invoices may result in automated GST notices and ITC reversal. |

| MSME Form-1 | Half-Yearly | 30 April & 31 October | Mandatory for Companies (Pvt. Ltd.) and LLPs. Any payment to Micro or small enterprises exceeding 45 days must be reported. Even if the payment is made later, the delay must be disclosed. |

| Udyam Profile Update | Annual (Post-ITR Filing) | July / August | Update Udyam details with the latest ITR and GST data to ensure correct classification as Micro, Small, or Medium under the revised 2025 thresholds. Incorrect data may lead to loss of MSME benefits. |

Regular compliance not only avoids penalties and notices but also improves Credit eligibility with banks & NBFCs, Access to government schemes & subsidies, & Legal protection for delayed payments