FAQS on NRI Taxation Under Income Tax Act

Page Contents

FAQS on NRI Taxation Under Income Tax Act

Q. : Are there any provisions under which NRIs are provided any refund of tax in India?

In India, where the NRIs pays any amount of TDS in a financial year, and at the time of filing their ITR, their tax liability comes to be lower than the amount of TDS deducted, the difference between the said amounts can be claimed as a TDS refund according to their tax slab rates.

Q. : What are the slab rates for taxation of NRIs in India?

The following table shows the applicable tax rate of NRI –

| TAXABLE INCOME (RS) | TAX RATE |

| 0 – 2,50,000 | NIL |

| 2,50,000 – 5,00,000 | 5% |

| 5,00,000 – 7,50,000 | 10% ON EXCESS OF 5,00,000 + 12,500 |

| 7,50,000 – 10,00,000 | 15% ON EXCESS OF 7,50,000 + 37,500 |

| 10,00,000 – 12,50,000 | 20% ON EXCESS OF 10,00,000 + 75,000 |

| 12,50,000 – 15,00,000 | 25% ON EXCESS OF 12,50,000 + 1,25,000 |

| ABOVE 15,00,000 | 30% ON EXCESS OF 15,00,000 + 1,87,500 |

Other taxes charged on the above tax rates are

- HEALTH AND EDUCATION CESS: On the above tax liability, a Health and Education Cess @4%, is charged on the value of the tax liability including Surcharge, if any. This cess is applied on the tax liability of every person irrespective of their age and residency.

- SURCHARGE APPLICABLE: A fixed percentage of Surcharge is levied on the tax liability; in case the total taxable income of the individual exceeds the limit prescribed.

- The rates are as follows –

-

- 10% for Income exceeding Rs 50 Lakh and up to Rs 1 crore.

- 15% for Income exceeding Rs 1 Crore and up to Rs 2 crores.

- 25% for Income exceeding Rs 2 Crore and up to Rs 5 crores.

- 37% for Income exceeding Rs 5 Crore

Such a rate of surcharge is applied and added to the value of Tax liability.

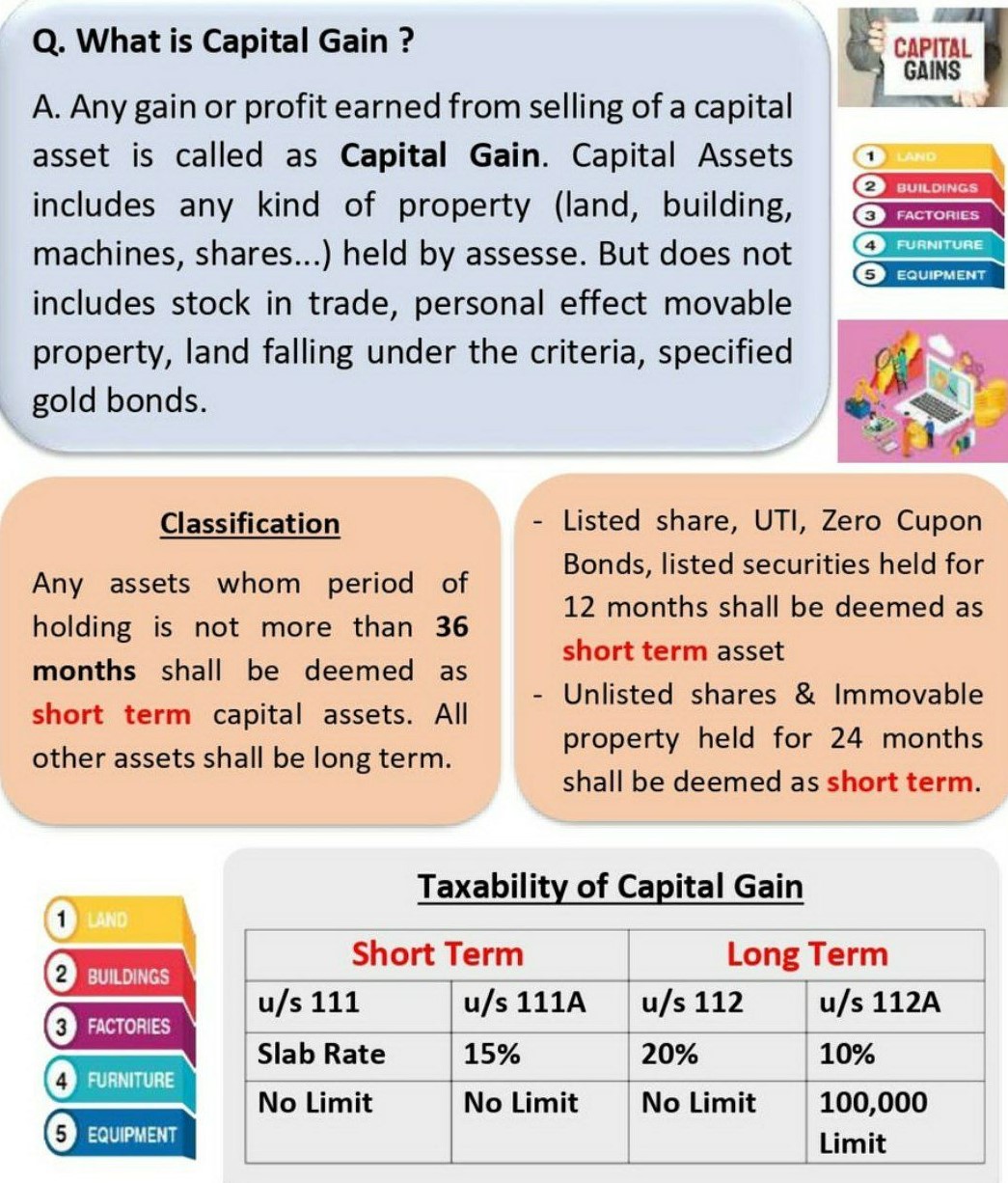

Q. : What are the provisions related to setting off of capital gains for NRIs?

SHORT-TERM CAPITAL GAINS ON EQUITY/EQUITY MUTUAL FUNDS

This amount of capital gain is liable to be set off against their basic exemption limit. They have to pay 15% tax on the said amount of gain, excluding surcharge and cess.

LONG TERM CAPITAL GAINS ON EQUITY/EQUITY MUTUAL FUNDS

In case of LTCG, NRIs can avail exemption up to an amount of Rs 1 lakh, but in case the amount exceeds the prescribed limit, they have to pay tax @ 10%. They cannot set off this gain, with their basic exemption limit.

SHORT TERM CAPITAL GAINS ON DEBT/GOLD/REAL ESTATE

This income is taxed as per their applicable slab rates and the said gain can also be set off against the basic exemption limit.

LONG TERM CAPITAL GAINS ON DEBT/GOLD/ESTATE ETC.

NRIs are not allowed to set off this gain against their basic exemption limit and will have to pay tax @ 20% along with indexation benefit, and @ 10% without the indexation benefit.

Tax planning on capital Gain

Q. : What are the benefits of filing ITR on time?

A NRI is benefited with various advantages, where they file their annual return in a proper and timely manner. Its benefits are –

- FASTER PROCESSING OF REFUND – In case the amount of tax paid is less than the actual tax liability, the IT department issues a refund for the same. In case the ITR is filed within the prescribed time, the refund gets transferred to the linked bank account easily.

- MEANS OF KNOWING THE STATUS – Due to International Agreements, Income Tax Department has access to lot of information, and due to unavailability of information about the status of NRIs, PIOs etc, they send notices to NRIs, PIOs seeking various information about foreign transactions (e.g., Remittance from India to Abroad). Thus, ITR filing can help them in figuring out the residential status and other requisite information automatically.

- MEANS OF ACKNOWLEDGMENT IN VARIOUS ASPECTS – NRIs, PIOs can show the acknowledgement of ITR submission as a requisite or alternative document at various places. It serves as a legal and government document for various purposes.

- TRACKING BY IT DEPARTMENT – Continuous ITR filing helps IT department to keep a track record of the NRI. NRIs, PIOs can keep themselves updated with all Income Tax Updates if they keep filing their ITR regularly.

- CARRY FORWARD OF LOSSES – where a NRI undertakes any transaction in which they incur losses, then filing of ITR will allow them to carry forward that loss to set it off against any future capital gain.

- REMITTANCES TO ABROAD – NRIs PIOs do approach banks for remittance of their NRO account money to outside India, and banks require them for Form 15CA, 15CB. To obtain the forms, the CA asks for ITR filing records to get the Form 15CA and 15CB verified and submitted expeditiously and conveniently.

- LOWER TDS CERTIFICATE – A NRI can apply to the IT department for obtaining a Lower TDS Certificate in order to avoid TDS deduction at a higher rate. In order to obtain the same, ITR records of the last 2-3 years help them for early processing of their lower TDS application.

- MEANS OF COMMUNICATION OF FINANCIAL TRANSACTIONS – ITR Filing also helps in communicating to the IT Department about taxable component of a financial transaction in India

- LOOKING FOR BORROWINGS AND CREDIT CARD IN INDIA – Where a NRI looks for any loan or credit card application, ITR copy is prerequisite.

- EASE IN COMING INDIA AGAIN – once NRI leaves India, there records are thoroughly verified when they return to India again. ITR filing can be very helpful, productive and beneficial as it will keep their Tax Status maintained, and on coming back to India they will have a continuous record of their ITR.

- REPATRIATION – having the details of all the assets of the NRI, the foreign country can easily follow and apply the repatriation provisions on the respective NRI.

Returns & Forms Applicable for NRI Individual for the Assessment Year 2024-25

Q. : What incomes are exempted for an NRI?

The following incomes are exempted for a NRI in India –

-

- Any amount received as interest on NRE & FCNR (Foreign Currency Non- Repatriable) account

- Amount of interest received on government issued savings certificates and notified bonds.

- Amount of dividends from shares of domestic companies (taxable from AY 2021-22)

- Long term capital gains from listed equity shares and equity- oriented mutual funds, up to a certain limit.

Q. : What are the documents required to avail the benefit under DTAA?

There are various documents required to be submitted like –

-

- A Self-declaration cum indemnity format form.

- A Self-attested copy of the PAN card issued in the name of the respective NRI.

- Self-attested copy of the visa and passport of the said NRI.

- Copy of the PIO proof.

- Tax Residency Certificate (TRC) issued by the home country.

It is to be noted that according to the Finance Act 2013, an individual is compulsorily required to have TRC, to claim benefit under DTAA.

To receive the Tax Residency Certificate, an application is to be made in Form 10FA to the income tax authorities. Once the application is successfully processed, the certificate will be issued in Form 10FB.

Take Support from experts who Help with it comes to DTAA

- It gets more difficult to take advantage of DTAA laws after you become an NRI and have numerous income sources in different countries, as well as having spent time in India and overseas.

- If you try to do it yourself, you run the risk of making a mistake and paying less (or more) tax. As a result, I strongly advise you to employ a professional Chartered accountants with experience in DTAA matters and pay them to conduct the computations and tax filing for you.

- I hope that this post has helped you comprehend the various DTAA rules. We also welcome you to look into our NRI financial planning services if you are an Non Resident Indian.

UNITED STATES OF AMERICA TAX RETURN PREPARATION SERVICES

- Wages & Tax Statements Form – W-2

- Estimated Tax Form – 1040-ES

- Non-Profit Corps. Form – 1041

- Employer Quarterly Federal Tax Return Form – 941

- Information Return Form – 5472

- Entity Classification Election Form – 8332

- C-Corporation Form – 1120

- Individual Return Form-1040

- Partnership Form-1065

- S-Corporation Form-1120S

- Treaty-Based Return Positions Disclosure Form – 8833

Popular blog:

- All about the Income taxation on capital gain

- Provision-of-capital-gains-charts

- Govt needed to introduce changes in NSP Budget 2021

- All about the Income taxation on capital gain

- Deduction u/s 80CCD of Income Tax Act, 1961

- All about the Income taxation on capital gain

- Delay in the deposit of Employer provident fund during the lockdown

- Aware of the penalty of Section-234f for late filing of ITR

For query or help, contact: singh@carajput.com or call at 9555555480