When is the cancellation revocation applicable?

Page Contents

When is the cancellation revocation applicable?

Procedure for Implement Revocation for GST cancellation

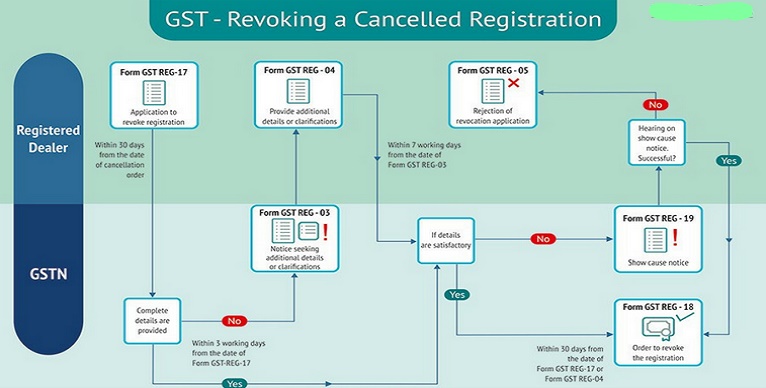

- This applies only if, on its own motion, the tax officer has cancelled the registration of a taxable person. Such taxable person may apply to the cancellation officer within 30 days from the date of the cancellation order.

Note: Application for revocation cannot be filed if the registration has been cancelled due to failed to submit returns. Such returns must be made in the first place along with the payment of all amounts of tax, interest and penalty due. Such returns must be made in the first place and all amounts of tax, interest and penalty due must be paid.

- A registered person may submit a request for cancellation in FORM GST REG-21 if his registration has been cancelled by the appropriate officer.

- It must be submitted to the Common Portal within thirty days from the date of the provider of the cancellation order.

- If the proper officer is satisfied, he may cancel the registration by order in FORM GST REG-22 within 30 days from the date of receipt of the application. Revocation of the cancellation of the registration must be recorded in writing.

- Proper officer may by order in FORM GST REG-05 reject the request for revocation and may convey the same with the applicant.

- Before rejecting the application, the competent authority must send a statement of cause in FORM GST REG–23 to show the applicant why the application must not be refused. The candidate must reply to FORM GST REG-24 within 7 working days of receipt of the notification service.

- Judgement of the appropriate officer shall be taken within thirty days from the date of receipt of the explanation from the application form in FORM GST REG-24.

Read also : Registration of GST under Goods and Service Act, 2017

- Finally after receipt of the request for GST registration Revocation, in the form GST REG-21, if the Proper officer is completely comfortable with the reason/revocation of the GST Registration, the cancellation of the registration in the form FORM GST REG-22 shall be revoked.

- After the receipt of Revocation Request, in Form GST REG-21, if the officer is satisfied by the reason/ grounds for revocation of GST Registration, then he shall revoke the cancellation of registration in FORM GST REG-22

- Be Caution: If you are a GST registered person who has a good deal and a stock in hand and by any error (due to a lack of consciousness of GST law) your GST number is cancelled.

- it is recommended that before proceeding with the submission of any reply to the GST Officer, please ensure that you have sufficient knowledge of GST law or consult with the GST Expert even though, nowadays,

- GST Department is quite serious in GST compliance and compliance, By placing a wrong reply may cancel your GST registration that can be harsh to the GST Registered person according to its Stock holding by the Business owner & GST tax liability on his stock in hand.

GSTN allowed CAs, advocates, applicants, & members of the general public may visit Delhi GST Dept.

- The GST Dept. issued a public notice on April 4, 2024, permitting CAs, advocates, applicants, and members of the general public to visit the Delhi GST Department.

- GST Dept Competent Authority is able to allow members of the public, applicants, advocates & CAs in the CRC Branch, on Mondays & Thursdays, between 3:00 and 4:00 PM, to provide clarification on their GST New Registration application via relevant Goods and Services Tax Officer of the Delhi GST Department.

please feel free to contact us on 9555 555 480 or singh@carajput.com