All about Financial Forensics & its Applications

Page Contents

All about Financial Forensics & its Applications

Financial Forensics and Forensic Audit Techniques

Financial forensics and forensic audit techniques are critical components of investigative processes aimed at uncovering financial irregularities, fraud, or misconduct within organizations or financial transactions. The field of financial forensics, outlining its purpose, applications, and techniques.

Financial Forensics Explained:

- Combines accounting and investigation skills to uncover financial crime.

- Investigates individuals’ and organizations’ finances to determine truthful financial management.

- Aims to prevent financial crime, recover lost assets, and identify investment opportunities for

Applications of Financial Forensics:

- Financial theft: Investigating instances of stolen money from organizations (e.g., employee stealing cash).

- Securities fraud: Examining potential misrepresentation of information to investors (e.g., misleading stockbroker advice).

- Money laundering: Detecting the process of concealing illegal income as legitimate (e.g., investing stolen cash into businesses).

- Corporate valuation disputes: Analyzing a business’s true value during acquisitions (e.g., ensuring fair purchase price and uncovering hidden financial issues).

- Tax evasion: Investigating attempts to avoid paying taxes (e.g., hiding profits in shell corporations).

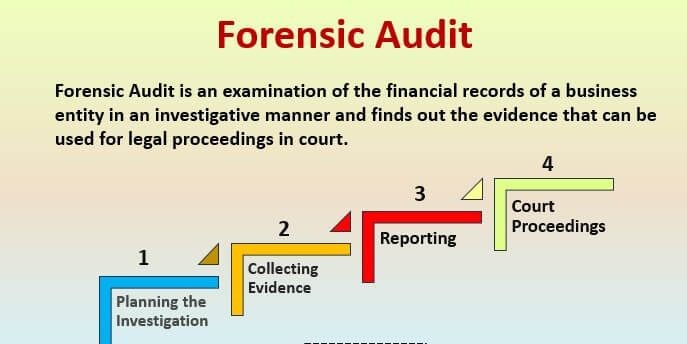

Forensic Auditing Techniques:

- This acknowledges the growth of financial crime and the need for in-depth analysis, highlighting the rise of forensic accounting as a specialist

- Defines forensic accounting/auditing as cross-checking financial records to detect fraud and providing in-depth analysis for legal purposes.

- Compares forensic accountants to economic and business detectives who scrutinize transactions to uncover illegal

- Overall, financial forensics and forensic audit techniques play a crucial role in uncovering financial fraud, ensuring financial transparency, and safeguarding the integrity of financial systems and organizations.

Benefits of Forensic Accounting:

- Reduces losses: Uncovers fraudulent activity and minimizes financial

- Improves efficiency: Identifies areas for improvement and optimizes business

- Increases profitability: Leads to better financial health and potential for

- Prevents future fraud: Provides insights to strengthen internal controls and deter future

Qualities of a Forensic Accountant:

- Logical mind: Ability to think critically and analyze information

- Attention to detail: Meticulous observation of financial records, identifying potential discrepancies.

- Strong morals: Upholding ethical principles and resisting

- Inquisitiveness: Constantly questioning and seeking deeper understanding of

- Spontaneity: Adaptability and ability to think creatively when encountering unexpected

- Accounting knowledge: Comprehension of accounting principles and their impact on financial statements.

These qualities, combined with investigative techniques, equip forensic accountants to uncover financial wrongdoing.

Investigative Techniques in Forensic Accounting:

- Public document review and background checks: Scrutinizing publicly available information (corporate records, online data) to understand the company’s history and potential red flags.

- Detailed interviews: Conducting thorough interviews with relevant individuals to gather information and understand the context of alleged

- Gathering information from confidential sources: Utilizing information from reliable confidential sources, while ensuring their anonymity to protect

- Evidence analysis: Examining gathered evidence (documents, statements, etc.) to identify patterns, inconsistencies, and potential leads.

- Surveillance: Monitoring communications (emails, messages) or physical activity to gather further evidence, but only with proper legal authorization.

- Undercover operations: Involving an undercover agent to infiltrate and gather information, but this should be a last resort due to its complexity and potential

- Financial statement analysis: Scrutinizing financial statements for irregularities, inconsistencies, or unusual patterns that might indicate

Ethical Considerations and Code of Conduct in Forensic Audit:

-

Ethical Business Practices:

- Acting with integrity, trust, and

- Respecting diversity, making empathetic

- Aligning compliance with core

· Understanding Ethical Issues:

- Importance of recognizing potential ethical

- Proactive approach to preventing issues and ensuring business

· Common Ethical Issues:

- Harassment and Discrimination:

- Creating a safe and inclusive work

- Complying with anti-discrimination laws (e.g., EEOC in the US).

- Addressing issues like ageism, disability bias, equal pay

Health and Safety:

| OSHA Violation | Description |

| Fall Protection | Unprotected sides and edges, leading edges |

| Hazard Communication | Classifying harmful chemicals |

| Scaffolding | Required resistance and maximum weight limits |

|

Respiratory Protection |

Emergency procedures and respiratory/filter equipment standards |

| Lockout/Tagout | Controlling hazardous energy (e.g., oil and gas) |

| Powered Industrial Trucks |

Safety requirements for fire trucks |

| Ladders | Standards for weight capacity |

| Electrical, Wiring Methods |

Procedures for reducing electromagnetic interference |

|

Machine Guarding |

Guarding for guillotine cutters, shears, power presses, etc. |

| Electrical, General Requirements |

Not placing conductors or equipment in damp locations |

-

Whistleblowing and Social Media:

- Protecting whistleblowers who report ethical

- Balancing free speech with potential harm to the

- Establishing clear social media policies for

Ethics in Accounting Practices

- Maintaining accurate financial records: Crucial for all organizations, especially publicly traded companies.

- Ethical violations: “Cooking the books” can have severe consequences, as exemplified by the Enron scandal.

- Enron scandal: A notorious example of financial statement manipulation that led to immense losses and the downfall of both Enron and its accounting

- Sarbanes-Oxley Act: Established new regulations in the US to protect consumers and shareholders after major corporate

- Importance of accurate records: Even small companies need accurate accounting for tax purposes, attracting investments, and profit-sharing.

Beyond Accounting:

- Non-disclosure agreements: Used to protect confidential information and prevent corporate espionage (illegal distribution of confidential data).

- Technology and privacy: Advancements in technology raise concerns about employee privacy:

- Companies monitor employee activity on company devices (computers, ).

- Finding the right balance between efficiency/productivity and privacy is

- Transparency is key: informing employees about monitoring

Avoiding Ethical Issues in Business:

This highlights the importance of proactive measures to prevent ethical issues in a business.

Leadership and Transparency:

- Top management sets the tone: Ethical behaviour starts with leadership, influencing the overall business

- Written policies and processes: Clear guidelines ensure everyone understands ethical expectations and procedures.

- Communication and enforcement: Regularly communicate the code of ethics and actively enforce

Awareness and Compliance:

- Discrimination laws: Stay informed about and comply with anti-discrimination regulations in your

- Applicable rules and regulations: Understand and follow relevant laws and regulations impacting your

- Transparency with accountants: Maintain open communication and honesty in financial

Continuous Commitment:

- Doing the right thing: Strive to make ethical decisions and uphold high moral standards in all aspects of business

Threats to Ethical Principles

These are situations that can make it difficult for auditors to uphold the above principles.

Threats to Ethical Principles in Auditing

| Threat | Description | Example |

|

Self-interest Threat |

Auditor or close family member has a financial stake in the audited entity, potentially influencing judgment. |

Auditor’s spouse works for the company being audited. |

|

Advocacy Threat |

Auditor becomes overly supportive of the client’s position, compromising objectivity. | Auditor overlooks questionable accounting practices to please the client. |

|

Intimidation Threat |

Auditor is pressured (physically or mentally) to compromise their objectivity. |

Client threatens to withhold audit fees if the auditor doesn’t “sugarcoat” the report. |

Fundamental Ethical Principles:

These are the core values guiding an auditor’s conduct

Fundamental Ethical Principles in Auditing

| Principle | Description | Example |

|

Honesty/Integrity |

Being truthful and transparent in all aspects of the audit process. |

Disclosing accounting errors to relevant authorities despite pressure from the client. |

|

Objectivity |

Remaining unbiased and independent in judgment, avoiding conflicts of interest. |

Conducting a thorough and impartial audit of a close friend’s company. |

|

Professional Competence |

Possessing the necessary skills, knowledge, and experience to perform the audit effectively. |

Regularly attending continuing education courses to stay updated on complex accounting standards. |

|

Due Care |

Performing the audit diligently and thoroughly, adhering to professional auditing standards. | Carefully scrutinizing all supporting documents and conducting appropriate audit procedures. |

|

Professional Behavior |

Acting with respect and professionalism towards all individuals involved in the audit process. |

Maintaining a courteous and respectful demeanor even when dealing with difficult clients or situations. |

Strategies for Mitigating Ethical Risks:

These steps help create an environment where auditors can fulfill their ethical obligations:

- Honestly assess needs and resources: The audit firm acknowledges its limitations and ensures it has the qualified personnel and resources to conduct a thorough and objective

- Establish a strong foundation: The firm creates a code of ethics and clear guidelines outlining expected behavior and procedures for identifying and addressing ethical

- Build a culture of integrity from the top down: Leadership demonstrates a commitment to ethical conduct and holds everyone accountable for upholding these

- Keep a “values focus” in moments big and small: The firm emphasizes ethical decision-making in all aspects of its work, not just during major

- Re-evaluate and revise as needed: The firm regularly reviews its ethical practices, adapting them to evolving industry standards and potential new risk

By understanding these principles, threats, and mitigation strategies, auditors can ensure the credibility and reliability of their work, fostering trust in the financial reporting system.

Major Threats to Auditor Independence and Corresponding Examples

| Threat | Description | Example |

|

Self- Interest Threat |

Financial stake in the client or dependence on outstanding fees. |

Audit team hasn’t received 2019 fees from ABC Company and might pressure a favorable 2020 audit report to secure payment. |

|

Self-Review Threat |

Auditor reviews their own work or work done by others in the same firm. | Same auditor prepares and audits ABC Company’s financial statements, raising concerns about objectivity. |

|

Advocacy Threat |

Promoting the client to the point of compromising objectivity. | Auditor assisting in selling ABC Company while also being their auditor might issue a favorable report to increase the sale price. |

|

Familiarity Threat |

Excessive familiarity with client personnel hinders objectivity. |

Auditor has audited ABC Company for over 10 years and socializes with executives, potentially lacking objectivity. |

|

Intimidation Threat |

Pressure from client to compromise objectivity. |

ABC Company threatens to switch auditors if the report is unfavorable, potentially influencing the auditor’s opinion. |

Challenges of Implementing an Effective Ethics Policy and Corresponding Solutions

| Challenge | Description | Solution | Example |

|

Resistance from Employees |

Employees may feel scrutinized or accused of unethical behavior. |

* Clearly communicate the purpose and impact of the policy. * Develop a values-driven policy focused on positive reinforcement. |

Hold company-wide meetings and Q&A sessions to explain the policy and address concerns. Emphasize the company’s commitment to ethical behavior and creating a positive work environment. |

|

Costs of Training and Implementation |

Training and maintaining an effective program requires ongoing investment. |

* Conduct regular training tailored to different employee roles and departments. * Focus on the long-term value of an ethical culture. |

Partner with external training providers or develop in-house programs to deliver cost- effective training. Regularly measure the impact of the training and update content as needed. |

|

Difficulty Demonstrating ROI |

Measuring the direct benefits of an ethics program can be challenging. | * Link ethics programs to broader performance and corporate strategy. * Focus on building trust | Track and report on metrics like employee satisfaction, whistleblower reports, and ethical decision- |

| and ethical leadership throughout the organization. | making examples. Highlight how these aspects contribute to a positive work environment and improved brand reputation. |

Key to Effective Implementation: Ethical Leadership

- Senior management sets the tone for ethical

- Strong ethical leadership fosters trust and encourages employees to follow the ethics

By understanding these threats and challenges, companies can create and maintain an effective ethics policy that safeguards auditor independence and promotes ethical behaviour throughout the organization.