Change GSTR-3B Report of ITC availment reversal, Ineligible

Page Contents

What are the new Change GSTR-3B on Reporting of ITC availment, reversal & Ineligible ITC?

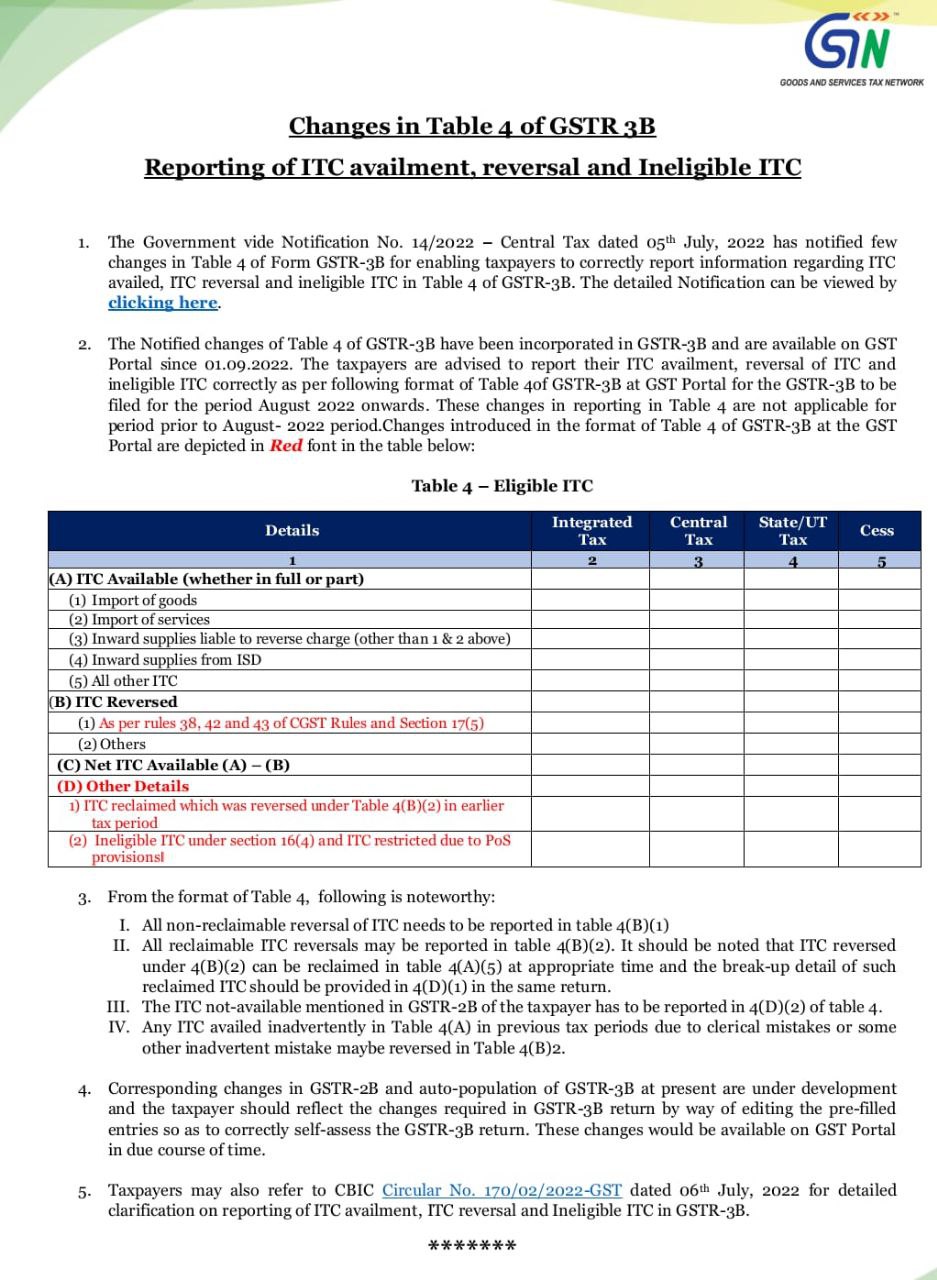

- Indian Govt issued Notification No. 14/2022 (dated on July 5, 2022.) purpose of the notification to allow taxpayers to accurately disclose information regarding ITC claimed, ITC reversed, and ineligible ITC in Table 4 of Form GSTR-3B,

- Above notified amendment in the GSTR 3B Table 4 have been added in GSTR-3B & are same changes are available on GST Portal with effect from Sept 01, 2022.

- GST Taxpayers are suggested to report their Input tax credit availment, reversal of Input tax credit & ineligible Input tax credit accurately as per below format of GSTR 3B Table 4 at Online GST Portal filed for the month of August 2022 onwards.

- Above nofified changes in GSTR 3B reporting in Table 4 are not levy for month prior to August-2022. Amendment come in the GSTR 3B format Table 4 at the online GST Portal are showing in the table below:

- Amendment have been made by CBEC on GSTN Portal for GSTR 3B to give the effect of Amendment in respect of reporting of Input tax credit on suggestions by GST Council.

- Change of GSTR 3B Table 4(B) & (D) of Form GSTR – 3B vide CBEC Notification no. 14/2022 dated July 5,2022 & clarification issued in regard to reporting of the same vide CBEC Circular 170/02/2022 is made live on the GSTN portal.

- After the Changes in GSTR 3B Table 4(B), all the Input tax credit as available in GSTR-2B including Input tax credit ineligible in terms of section 17(5), Rule 42,43, 38 & reclaimed Input tax credit (earlier reversed due to ineligibility as per section 16(2)(c) and (d) & GST Rule 37) needs to be reported in GSTR 3B Table 4(A).

Reversal of Input tax credit – GSTR 3B Table 4(B)

- Ineligible Input tax credit (Temporary reversal & Permanent reversal) will be reported separately in GSTR -3B Table 4(B). Resolutely, Net Input tax credit as per GSTR 3B Table 4(C) i.e., [4(A) – 4(B)] shall only be credited to the electronic credit ledger.

- In the GSTR 3B Table 4(D) – Other details, below requirements to be reported-:

(1) Input tax credit reclaimed which was reversed under GSTR 3B Table 4(B)(2) in earlier tax periods

(2) Ineligible Input tax credit U/s 16(4) of GST Law & Input tax credit limited Due to POS provisions.

- Respective Corresponding amendment in GSTR return-2B & GSTR-3B Auto-Populated at currently are under system development & GST taxpayer should reflect above amendment needed in GSTR-3B filling by way of editing pre-filled entries so as to accurate self-assess GSTR-3B filling of online return system implemented. Above amendment will be available on online GST Portal in normal due course time.

- GST Taxpayers might be refer to GST Department Circular No. 170/02/2022- (dated July 06, 2022) for detailed explanation on change in GSTR 3B reporting of Input Tax credit availment, Input Tax credit reversal & Ineligible Input Tax credit in GSTR-3B.

In Summary

Above GSTR 3B From in the given format of GSTR 3B Table 4, below point is important mention here :

- Non-reclaimable reversal ITC: All non-reclaimable reversal of Input tax credit needs to be reported in GSTR 3B on table 4(B)(1)

- Reclaimable ITC : All reclaimable Input tax credit reversals may be reported in GSTR-3B table 4(B)(2). We needed to be remember that Input tax credit reversed under GSTR 3B on 4(B)(2) can be reclaimed in GSTR 3B on GSTR 3B table 4(A)(5) at appropriate time & break-up detail of such reclaimed Input tax credit needed to be provided in GSTR 3B return table 4(D)(1) return.

- ITC Not available: The Input tax credit not-available mentioned in GSTR-2B of GST Taxpayer has to be reported in GSTR 3B of table 4(D)(2).

- Input Tax Credit Availed inadvertently: Any Input tax credit availed inadvertently in GSTR3B Table 4(A) in last GSTR periods due to significant mistakes or other inadvertent mistake maybe reversed in GSTR 3B Table 4(B)2.

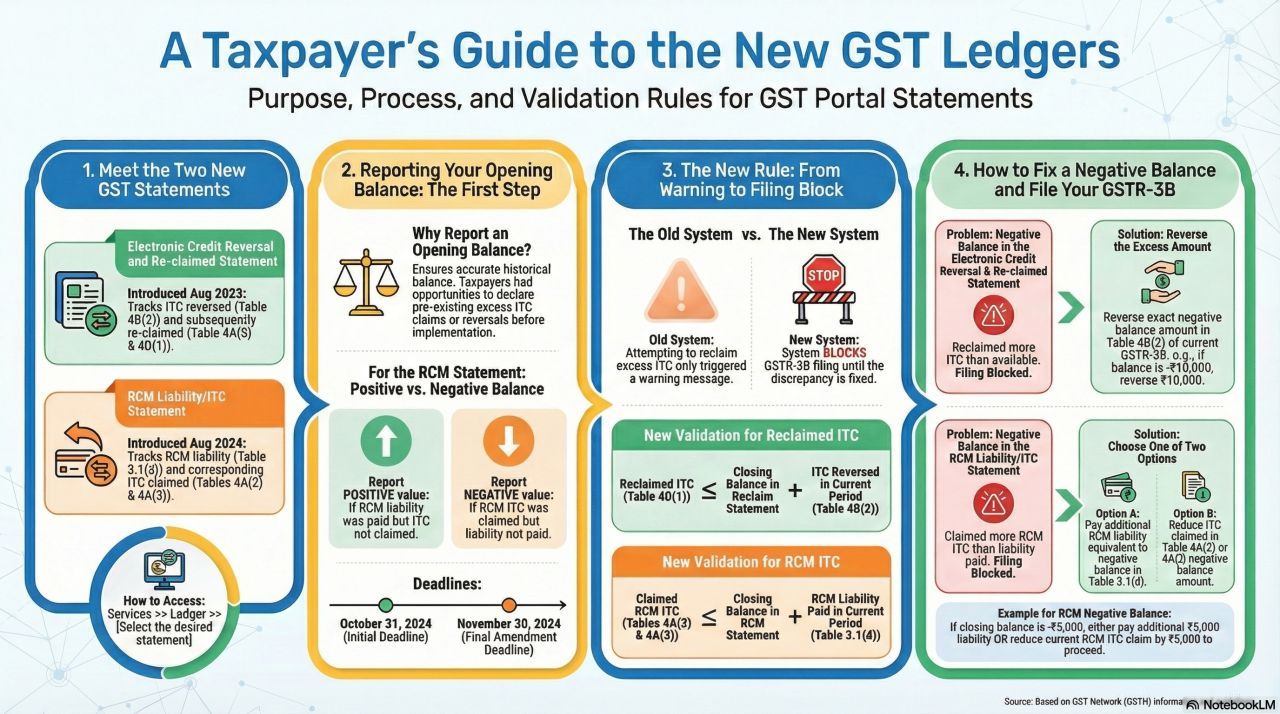

Recent changes in GST compliance related to ITC and RCM validations.

Meet the Two New GST Statements

- Electronic Credit Reversal and Reclaimed Statement Introduced in August 2023. which Covers ITC reversed under Rule 37, 38, 42, 43 and subsequently reclaimed (Rule 4(b) of 4/2018).

- RCM Liability/ITC Statement—Introduced in August 2024 & Tracks claimed ITC and liability under RCM (Rule 4A(b) of 4/2018).

- Access: Navigate to Services → Ledgers → Select the Ledger.

Reporting Your Opening Balance: The First Step

- Why Report an Opening Balance?

- Ensures accurate historical data for validations.

- Avoids discrepancies in future compliance.

- For RCM Statement: Positive vs. Negative Balance Reporting.

- Deadlines:

- October 31, 2024 (Electronic Credit Reversal Statement)

- November 30, 2024 (RCM Statement)

The New Rule: From Warning to Filing Block

- Old System: Allowed filing even if discrepancies existed; only showed a warning.

- New System: Filing of GSTR-3B is blocked if ITC and RCM discrepancies are not fixed.

- New Validation for Reclaimed ITC: Reclaimed ITC (Table 4(B)(2)) ≤ Closing Balance in Electronic Credit Reversal Statement.

- New Validation for RCM ITC: Claimed ITC (Table 4(A)(3)) ≤ Closing Balance in RCM Statement.

How to Fix a Negative Balance and File Your GSTR-3B

- Problem: Negative balance in Electronic Credit Reversal Statement.

- Solution: Reverse excess amount or reclaim more ITC than reversed (filing blocked).

- Problem: Negative balance in RCM Statement.

- Solution: Reverse excess amount, OR Claimed more RCM ITC than liability paid.

- Options: Choose one of two corrective actions before filing.

Above emphasizes validation-based filing blocks, GST taxpayers must reconcile ITC reversals and RCM liabilities before filing GSTR-3B. This is a major compliance shift from warnings to hard stops.

Popular Articles: