All about Fines/ Penalties associated with TDS

Page Contents

TAX DEDUCTION AT SOUSES DUE DATES

| QTR | Due date of TDS Fillings | TDS Filling Period |

| 1st QTR | 31st July of FY | 1st April to 30th June |

| 2nd QTR | 31st October of FY | 1st July to 30th Sept. |

| 3rd QTR | 31st January of FY | 1st October to 31st Dec. |

| 4th QTR | 31st May of FY | 1st January to 31st March |

What is penalty on TDS?

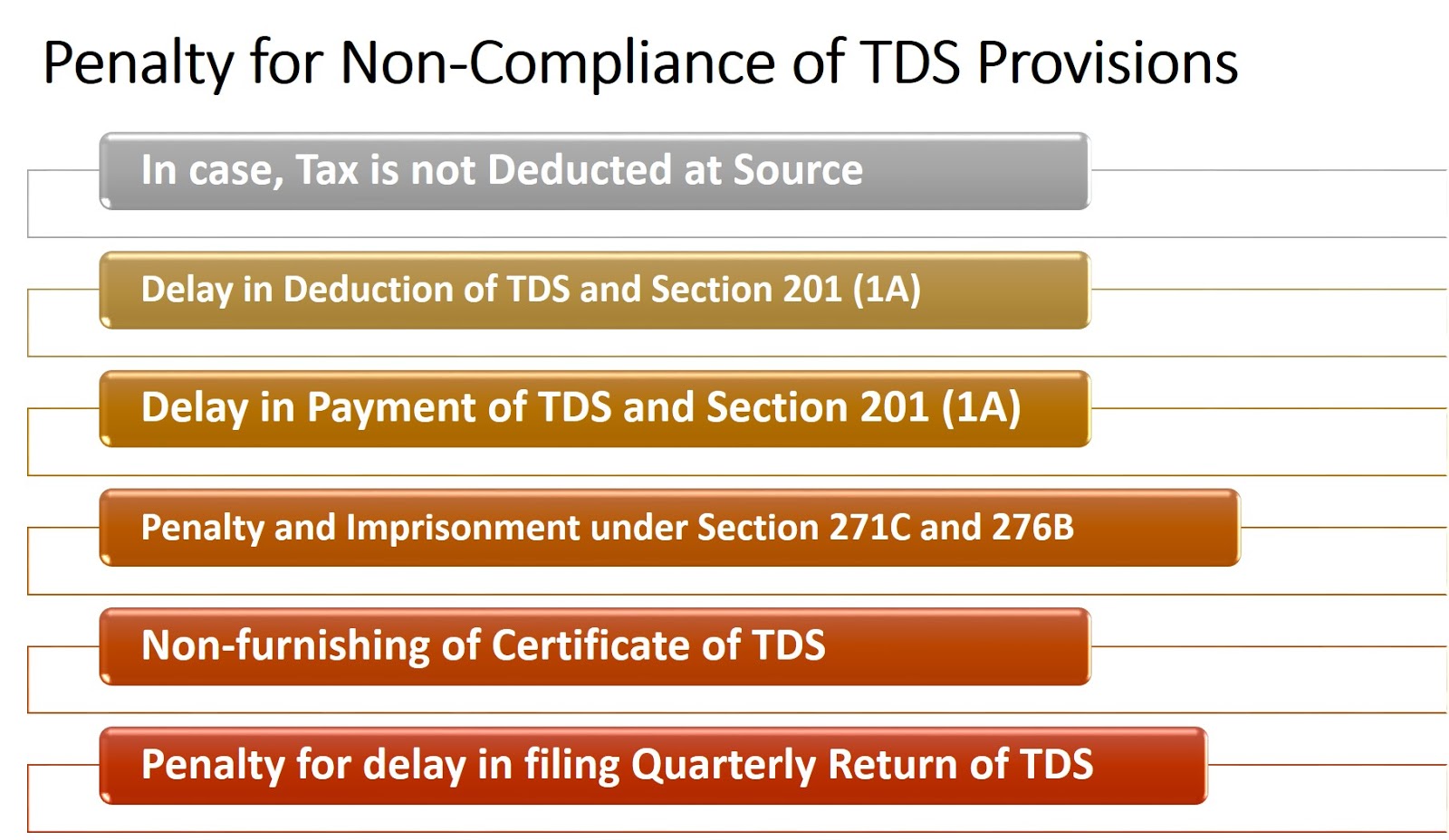

Fines/ Penalties associated with the TDS

The deductor shall be liable for the fine if the TDS deduction and payment deadlines are violated.

- Non-deduction of the Tax Deducted at Source(TDS) : In case the deductor/collector fails to collect the tax at source, all these expenses may be disallowed from the assessment of the overall revenue by the tax assessor.

- For the late deduction of the Tax Deducted at Source(TDS): In case the tax at source is deducted within a day or a few days after payment of the profits, simple interest at a rate of One % per month will be charged on the balance of the tax deducted at source.

- In case late payment of the Tax Deducted at Source(TDS): As mentioned above, there is a monthly due date for the TDS to be deposited with the Government. If the deductor fails to do so it must pay simple interest on the amount deducted as tax at a rate of 1.5 percent per month.

- For late-filing of Tax Deducted at Source(TDS) Returns: In case of deductor fails to furnish the TDS return on or before the specified due date, he shall be liable to pay a penalty of INR 200 per day till the date of default. Please note that the total amount of such penalty cannot exceed the total amount of tax deducted at the source.

- In case Non-filing of Tax Deducted at Source(TDS)Returns: in case deductor fails to file TDS return within the due date, then the assessing officer may charge a penalty ranging from INR 10K to 100k.

In the circumstance of a deduction loss at source, the payer would have to relieve his tax liability.

TDS Penalty Payment

- Log in to the e-filing portal for income taxes.

- (https://home.incometaxindiaefiling.gov.in)

- Click the e-Pay tax link in the left sidebar.

- Visit the NSDL’s website.

- Fill in the required details and the TDS penalty amount on Challan ITNS 281.

- Make a payment using the chosen payment mode by clicking on ‘Submit and Proceed.’

- In case you are looking for any kind of expert advice on TDS.

To find the total quantum, search Form 26AS from your e-filing account. This is a very well method of tax collection by the Indian government. To learn more about the current assessment year, free to contact us.

MULTIPLE ADVERSE & SERIOUS CONSEQUENCES OF TDS DEFAULTS:

- TDS is one such thing on that Income tax Act provisions are quite harsh.

- Non deduction of TDS entails several consequences such as, assessee is liable to be held as “assessee in default” meaning thereby TDS can be recovered from him, Interest @ 12%p.a. is mandatorily leviable on such non- deducted TDS, penalty u/s 221 can be levied which can be any amount upto the amount of TDS default, another penalty u/s 271C can also be imposed which is equal to the amount of TDS default.

- Further 30% of such amount on which Tax deduction at source default has happened would be added to business or professional income if such amount is sought to be claimed as expense against business or professional income meaning that TDS defaulter assessee would have to pay tax also accordingly.

- In case, Tax deduction at source via deducted but not paid or short paid or even not paid in time, has got one very serious consequence in the form of prosecution u/ s 276B with minimum rigorous imprisonment of 3 months to 7 years with Fine.

- One such case has been reported today in all leading newspapers where one Session Court at Mumbai has confirmed the conviction to Tax deduction at source defaulter Assessees. This default should be avoided via Professional advice and proper care needs to be exercised in matter of Tax deduction at source in face of severe consequences.

What You Should Know for the purpose of non-compliance of TDS Provision

- Penal interest must be paid to the government prior to filing a TDS return or in response to a TRACES demand.

- The Penal interest paid on non-filing/delayed filling or other TDS penal concerns is not eligible for any deduction, exemption or expenditure under the Income-Tax law.

TDS Deduction Rate Chart for (AY 2023-2024) FY 2022-2023

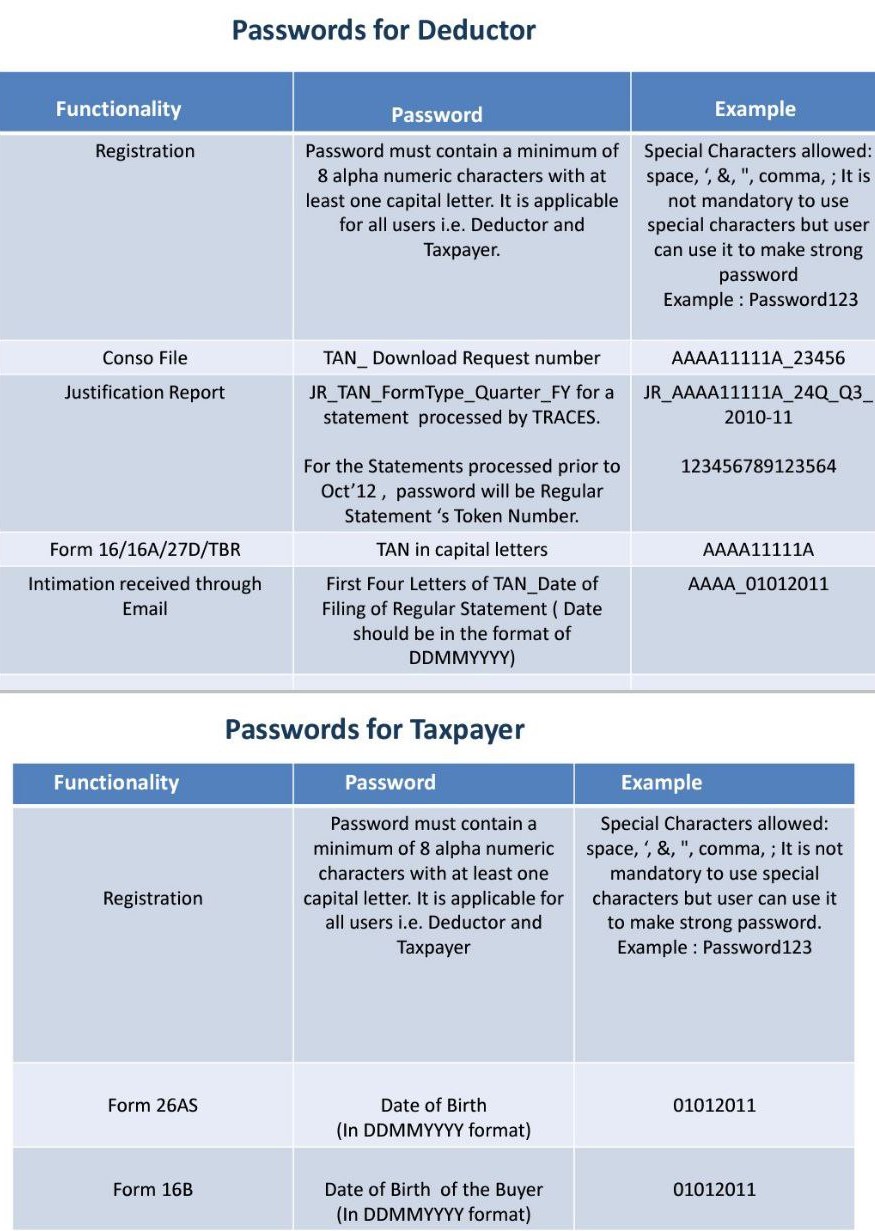

Password Format for Deductor and Tax Payer for Various Services on TRACES Portal

SMS Warnings on Greater Transparency

- The TDS department has sent a text message to the taxpayer from VK-ITDEFL indicating the amount of tax deducted at source (TDS) against the taxpayer’s PAN (Permanent Account Number). The SMS warning will remind you of the TDS credited on your salary, interest, etc. earnings, per quarter. The sum of TDS will be accrued in your Form 26AS for the various financial year.

- This program was initiated by the Ministry of Finance to improve transparency and reduce cases of TDS inconsistencies at the time of income tax filing. Taxpayers should cross-check the details given in the SMS with the payment slip information to ensure that there is no discrepancy. TDS mismatch may be a common explanation for incorrect filing of income tax returns.

- Query share on us an email at singh@carajput.com

Related Articles/pieces of information

-

Tax Deducted at Source (TDS) for Financial Year 2020-21

-

How to file a return of TDS online

-

New revise TDS/TCS due date for filing Return and Payment for the year 2020

-

key features of TCS on goods sale section-206c

-

New TDS deduction No cash transactions exceeding 1 Crore -Section 194N

-

Extention of TDS/TCS statement filing Date