Form 26 (Tax Audit Report) under the Income‑tax Rules, 2026

Page Contents

Form 26 (Tax Audit Report) under the Income Tax Rules, 2026

The new Form No. 26, introduced under the Income‑Tax Rules, 2026, represents a major structural overhaul of tax audit reporting. Overall, Form No. 26 shifts tax audit reporting from a narrative, clause‑heavy format to a data‑driven, schedule‑based, and system‑aligned framework, fully synced with the new Income Tax Act, 2025, and contemporary compliance architecture.

The objective of a tax audit is to ensure that income, expenses, and statutory compliances are accurately reported and supported by proper books of account. Section 44AB of the Income‑tax Act, 1961, mandates a tax audit for certain taxpayers based on turnover or gross receipts:

- In Case Businesses: INR 1 crore turnover threshold, Enhanced to INR 10 crore, where cash receipts and payments do not exceed 5% of total transactions

- In case Professionals: Gross receipts exceeding INR 50 lakh

To transition smoothly to Draft Form 26, businesses should Upgrade accounting and ERP systems to capture detailed transactional metadata. Implement robust TDS/TCS tracking and reconciliation mechanisms. Train internal finance and audit teams on the new structure and expectations and Coordinate early with tax technology and compliance software providers to align input formats and reporting logic.

The audit report must be filed and accepted before the ITR can be filed. Any delay in the audit directly impacts return filing. An audit due date extension occurs when the CBDT, through an official notification or circular, grants additional time to file tax audit reports under Section 44AB. These extensions are policy‑based, not case‑specific, and individual taxpayers cannot apply for an extension. However The relief applies only to the categories specified in the CBDT notification.

Features of Form 26 (Tax Audit Report)

Its key features of Form 26 (Tax Audit Report) are as follows:

- Unified and consolidated audit form : All the 3 erstwhile audit forms—Form 3CA, Form 3CB and Form 3CD—have been merged into a single smart and unified New Income tax Form No. 26, ensuring structured and standardised reporting across all categories of assessees.

- Alignment with ITR framework: Audit clauses and disclosures have been rationalised and aligned with the Return of Income structure, ensuring better consistency between the tax audit report and the income‑tax return, and reducing reconciliation mismatches.

- Streamlined disclosure of disallowable expenditure: Disallowable expenditures, which earlier required detailed clause‑wise and item‑wise reporting, have now been consolidated into a single disclosure, simplifying compliance while retaining material transparency.

- Introduction of dedicated Schedules: To improve clarity and analytical transparency, separate schedule-based reporting has been introduced, including schedule—losses, Depreciation and deductions; Schedule—Prior Period Items; Schedule—Computation of Receipts/Income; and Schedule—Computation of Expenses

- Enhanced auditor identification & accountability: Mandatory disclosure of the auditor’s membership number, firm registration number, and UDIN (Unique Document Identification Number). has been introduced to strengthen the audit trail and accountability.

- Explicit reporting of capital receipts and deemed incomes: Dedicated fields have been provided for disclosure of capital receipts and deemed incomes, which are not routed through the Profit & Loss Account, addressing a key gap in earlier audit reporting.

Circumstances That Typically Trigger Extensions:

CBDT extensions are usually announced when widespread or systemic issues affect compliance, such as:

- Technical Problems: Income tax e-filing portal glitches, utility or schema changes, and high traffic close to deadlines.

- External or Extraordinary Events: Natural calamities, large‑scale disruptions affecting business operations, and nationwide or regional emergencies.

- Regulatory or Procedural Changes: Introduction of new forms or reporting formats, significant amendments in audit disclosures, and transition years involving system or law changes. And now CBDT often considers representations from bodies such as ICAI, trade associations, and industry chambers before granting extensions

Structure of Draft Form 26 (Tax Audit Report)

Draft Form 26 signals a fundamental shift in tax audit philosophy—from a disclosure‑based report to a digitally verifiable compliance instrument. Draft Form 26, prescribed under the proposed Income Tax Rules, 2026, retains the core objective of a tax audit but significantly expands the scope, depth, and data granularity of reporting. The form is designed to align tax audit reporting with digital accounting systems, income tax return architecture, and cross-law compliance verification. Broadly, Draft Form 26 is structured into the following key parts:

Part A — Basic Assessee Information : This section captures the legal and identity profile of the assessee, including Legal name and trade name, PAN, Status (company, firm, LLP, proprietor, etc.), residential status, and Registered address and contact details

Part B—General Business and Accounting Information : This section significantly expands beyond earlier audit forms and covers the nature and type of business/profession, accounting system followed (cash/mercantile/hybrid), method of accounting and ICDS applicability, and details of digital accounting infrastructure, such as

-

- Accounting software / ERP used

- System‑generated reports and controls

- Data integrity and audit trail availability

Part C — Income Reporting (Expanded Scope) : Draft Form 26 goes beyond traditional Profit & Loss reporting by requiring explicit disclosure of incomes not routed through the P&L account, including Deemed dividends, Buyback proceeds, Capital receipts chargeable to tax, Government grants and subsidies and Other deemed or statutory incomes

Parts D–F — Expenses, Prior Period Items, Depreciation & Losses : These sections introduce schedule‑based, deeper reporting of key computation areas:

Expenses & Disallowances

- Consolidated but structured reporting of statutory disallowances

- Linkage with relevant provisions without excessive item‑wise narration

Prior Period Items

- Separate identification of prior period income and expenses

- Tax treatment reconciliation

Depreciation and Losses

- Block‑wise depreciation data

- Adjustments and differences between books and tax

- Tracking of carried‑forward losses with continuity validation

International Taxation & Cross‑Border Compliance : Draft Form 26 incorporates integrated reporting for international transactions, including Transfer pricing adjustments, thin capitalization checks, Foreign remittances and repatriation details and Cross‑border payments and related compliances

Indirect Tax and GST Linkage : A notable enhancement is indirect tax reporting integration, covering:

- GST registration details

- Composition scheme disclosure

- Exempt/nil-rated supplies

- Internal consistency between turnover reported under GST and income tax

TDS/TCS Compliance Reporting : Draft Form 26 requires detailed and granular tracking of withholding tax compliances, including Nature of payments subjected to TDS/TCS, Short deduction or non-deduction, delayed deduction or deposit and Reconciliation with statutory returns

Impact of Draft Form 26 :

- Greater Documentation and Reconciliation Requirements : Businesses will need robust accounting and compliance systems capable of generating reliable digital trails covering income and expenses, loans and deposits, GST and indirect tax data, TDS/TCS compliances, and international transactions. Manual or fragmented systems will significantly increase compliance risk.

- Expanded Role of Auditors : Auditors will now be required to validate digital accounting infrastructure, ICDS and computation adjustments, TDS/TCS correctness, and cross‑law reconciliations (GST, transfer pricing, and foreign remittances). This transforms the audit from form‑centric to process‑centric assurance.

- Increased Accountability: Clause-wise, data-driven certification means higher responsibility on auditors, greater documentation standards for taxpayers, and reduced tolerance for estimates, informal records, or unsupported claims.

Statutory Deadlines for Audit and Return Filing

For most audit cases, the compliance cycle follows this sequence:

| Compliance Requirement | Form | Standard Due Date |

| Tax Audit Report | Form 3CD (with 3CA / 3CB) | 30 September |

| Income Tax Return | ITR (audit cases) | 31 October |

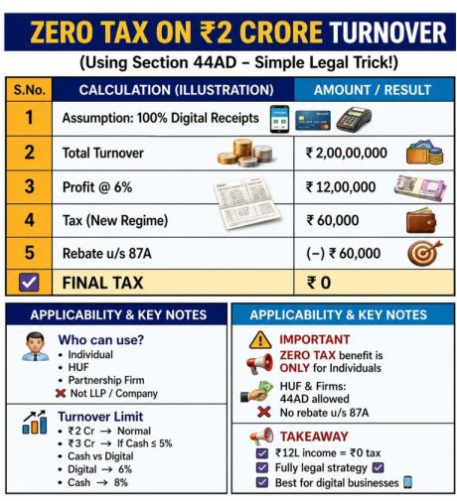

Taxpayers can legally reduce their tax liability u/s 44AD with proper tax planning.

- If your business turnover is up to INR 2 crore (higher threshold available in eligible digital receipt cases), the Presumptive Taxation Scheme u/s 44AD can significantly simplify compliance while optimizing your tax outflow.

- Section 44AD is not just a compliance shortcut; it’s a strategic tax planning tool when used correctly. Key benefits are no requirement to maintain detailed books of accounts, simplified income tax return filing, lower compliance burden, and reduced risk of scrutiny for small taxpayers.

- This scheme is most suitable for small business owners, traders, retailers, and professionals (via Section 44ADA separately).

- With proper planning under u/s 44AD, the declared income (presumptive basis), combined with available deductions and a rebate u/s 87A, can result in nil tax liability in eligible cases . This makes it a powerful tool for tax efficiency + compliance ease.

- Applicability depends on multiple factors such as turnover and nature of receipts (cash vs digital), type of taxpayer (individual, partnership firm, etc.), total taxable income, and eligibility for rebate. Expert consultation is strongly recommended before opting for the scheme or filing returns.

Consequences of Missing the Audit Deadline

Failure to file the audit report by the statutory or extended due date can have serious implications:

- Penalty under Section 271B : 0.5% of turnover / receipts and Maximum penalty capped at INR 150,000

- Impact on Return Filing: A delayed audit report may cause late filing of ITR, and Interest under Section 234A may apply

- Increased Scrutiny Risk : Repeated or habitual delays may invite closer examination in future assessments, a higher compliance burden, and an increased probability of queries and notices.