China’s Tax System vs. India’s Tax System

Page Contents

Overview of China’s Tax System vs. India’s Tax System

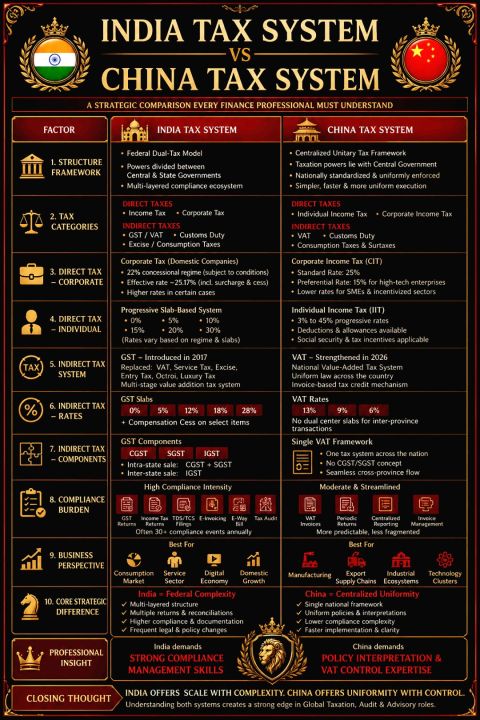

Overall Structure Framework

- India: Federal dual-tax model, Center + state powers, and Multi-layer compliance ecosystem

- China: Centralized unitary system, uniform enforcement, and Simplified framework

- Both countries divide taxes into the following:

- Direct Taxes: Income-based (Corporate Income Tax & Individual Income Tax)

- Indirect Taxes: Transaction-based (Goods and Services Tax in India, Value Added Tax in China)

- Both follow a value-added tax model for indirect taxes across supply chains.

- Practical reality is often missed in theory: (Tax rate ≠ Tax impact) : The real differentiator is Documentation burden, System predictability, audit risk, and administrative efficiency

Expert-Level Interpretation

- India = “Democratic Compliance Complexity”: Multi-authority control leads to litigation, frequent amendments, and interpretation gaps. Which results in high demand for CAs, tax consultants, and compliance systems?

- China = “Policy-Controlled Efficiency”: Centralized design Faster reforms, uniform implementation, and lower interpretational dispute. Which result shows that businesses focus more on execution than compliance firefighting?

Tax Categories

- India: Direct + Indirect taxes (GST-heavy structure)

- China: Direct (Income tax) + Indirect (value-added tax )

Direct Taxes

Corporate Income Tax (CIT)

- India

- 22% (base for domestic companies)

- 15% (manufacturing incentive)

- Foreign companies: ~36–38%

- Additional surcharge + cess

- Concessional rates for certain sectors/entities

- Higher effective rate after surcharge & cess so India has making effective tax due via surcharge/cess,

Corporate Tax

- China:

- 25% standard CIT

- Preferential rates:

- 15% for high-tech enterprises

- 20% or lower for small enterprises

- Incentives for MSMEs

- Fewer add-on levies vs India

- China offers more targeted preferential rates.

Individual Income Tax (IIT)

- Both countries: Progressive tax system + withholding at source

- India

- Two regimes (old/new), rates up to 30% – Progressive slab system (0–30%)

- Includes surcharge (up to 37%) + 4% cess

- India has reducing taxation burden in last few year,

- China

- Progressive 5%–45%, Progressive (3–45%).

- No major surcharge/cess structure

- China’s upper slab is significantly higher → impacts expat structuring & compensation design

- China has higher top marginal rates but a simpler structure.

Indirect Tax System & Indirect Tax Rates :

India – Goods and Services Tax System

- Unified system since 2017

- Three components:

- CGST + SGST (intra-state)

- IGST (inter-state/imports)

- Simple input tax credit rules

- Strong digital system (Goods and Services Tax Network, e-invoicing)

- India has a dual Goods and Services Tax (center + state) structure → slowly – slowly simplifying system

- GST replaced multiple taxes and Still layered with multiple rates and rules

- India GST slabs: 0%, 5%, 12%, 18%, 28% and Compensation cess on select goods

- China: Value-added tax-driven system and Cleaner flow with input credit mechanism

China – VAT System

- Fully unified nationwide

- Standard rates: 13%, 9%, 6% – China Value Added Tax : 6%, 9%, 13%

- Clear takeaway: China = fewer slabs → easier classification.

- No distinction between intra- and inter-regional transactions

- Centralized administration

- China has a single unified Value Added Tax system → simpler.

Tax Components

- India:

- CGST + SGST (intra-state)

- IGST (inter-state)

- China:

- Single VAT system

- No dual layer complexity

- Other Taxes

| Category | China | India |

| Consumption/Excise | Applies to luxury/specific goods | Limited (alcohol, tobacco, etc.) |

| Customs | Moderate (~7% avg), VAT refunds on exports | Higher (e.g., autos >60%), IGST on imports |

| Stamp Duty | Low, national system | High (5–8%), state-specific |

| Surcharges | Local education & infrastructure | Income tax surcharge & cess |

Governance Structure

- India (Federal):

- Central + State taxation powers

- GST governed jointly via Goods and Services Tax Council

- States still levy some independent taxes

- India = decentralized fiscal autonomy

- China (Unitary):

- Centralized tax laws and rates

- Local authorities mainly administer

- China = fully centralized system

Tax Administration & Compliance

India

-

- Highly digitized system: Goods and Services Tax Network platform, E-invoicing (IRN, QR code)

- Frequent filings: Monthly/quarterly + annual (~30+ filings/year possible)

- Strict enforcement: Penalties, audits, real-time invoice matching

- India = frequency compliance burden

- India:

- More compliance intensity

- Goods and Services Tax Returns, TDS, reconciliations, e-invoicing

- Frequent regulatory changes

China

-

- Value Added Tax invoice control system

- Fewer filings: Monthly + annual reconciliation

- More reliance on data monitoring vs frequent filings

- China = streamlined, mature system

- China:

- Moderate, streamlined

- Centralized reporting systems

- Less fragmentation

Business Perspective

- India’s strengths: Services, digital economy, and Domestic consumption growth

- China strengths: Manufacturing, exports, and Industrial clusters

Core Strategic Difference

- India: Compliance-heavy ecosystem

- China: Efficiency-driven system

Key Takeaways China’s Tax System vs. India’s Tax System

- Structure: Similar tax categories but different implementation

- Complexity:

- India: More complex due to federal dual Goods and Services Tax

- China: Simpler, centralized system

- Tax Burden:

- India: moderate due to surcharges/cess

- China: Competitive with targeted incentives

- Compliance:

- India: compliance pressure, strict audit environment

- China: Stable, invoice-driven monitoring

Future Trends

-

- India: Simplification of Goods and Services Tax and New Direct Tax Code under discussion

- China: VAT law modernization, and Continued tax optimization

Impact on MNC Structuring

This comparison is accurate and insightful, but the real-world takeaway is India rewards compliance excellence and China rewards operational efficiency. India challenges your compliance capability. China challenges your system understanding. Global professionals must master both because strategy lies not in tax rates, but in tax behavior.

- India Needs strong compliance teams, Transfer pricing scrutiny is intense and Goods and Services Tax cash flow management is critical

- China: : Requires regulatory understanding, Value Added Tax planning is central and Regional incentives play key role

Very Important is Hidden Strategic Layer

| Factor | India | China |

| Litigation risk | Simple | Moderate |

| Policy predictability | Medium | Moderate |

| Ease of scaling ops | Slower | Normal |

| Data-driven enforcement | Growing | advanced |

Both systems are modern and Value Added Tax driven, but India is more compliance-oriented, while China is more centralized and administrative.