Unjust Enrichment under Goods & Services Tax

Page Contents

Unjust Enrichment under the Goods and Services Tax Act

- Due to the fact that GST is an indirect tax structure and that the consumer has to bear its incidence, it is usually assumed that the owner of the business will transfer the incidence of tax to the final consumer.

- For the same reason, any refund claim (excluding specified exceptions) is required to pass the “unjust enrichment” test. If such claims are punished, they shall first be transferred to the Consumer Welfare Fund.

- The test shall not apply to refund of accumulated ITC, a refund of payment of incorrect tax, refund on account of exports, the refund of tax paid on supplies, etc.

- In addition to the above-mentioned incidents, the “unjust enrichment” test must be carried out if the claim amount is to be received by the applicant

Refund of GST – Doctrine of Unjust Enrichment

- Under Goods and Services Tax, a presumption is always drawn that Owner will shift the incidence of tax to the final consumer, as Goods and Services Tax is an indirect tax whose incidence is to be borne by consumer.

- So, every claim of refund if sanctioned should pass the test of ‘Unjust Enrichment’ and is first transferred to the Consumer Welfare Fund.

- This is not applicable in case of :-

-

- Goods and Services Tax refund of payment of wrong tax (IGST instead of CGST plus SGST& vice versa)

- The Goods and Services Tax refund of accumulated Input Tax Credit

- Goods and Services Tax refund of tax paid on a supply which is not provided.

- TheGoods and Services Tax refund on account of exports

- if the applicant shows that he has not passed on the incidence of tax to any other person:

- For Goods and Services Tax refund claims exceeding INR 2,00,000/-, a certificate from a CA / CWA will have to be given.

- If the Goods and Services Tax refund claim is less than INR 2,00,000/-, then a self-declaration of the applicant to the effect that incidence of tax has not been passed to any other will suffice to process Goods and Services Tax refund claim.

- The Goods and Services Tax refund of tax paid on a supply for which Goods and Services Tax refund voucher is issued.

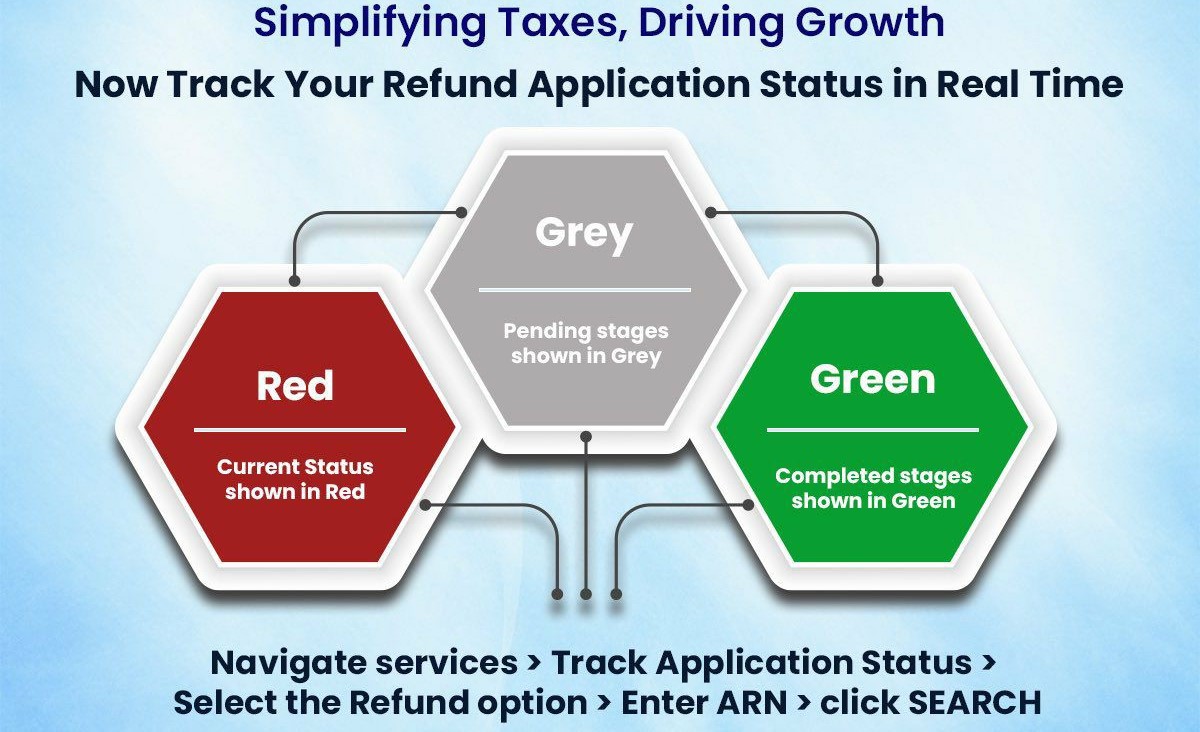

Now you Can Track your GST Refund on real Time Basis

FAQs on GST Refund

Q.1 What if the taxpayer fails to deliver the invoice and invoice within one month, will he add the details in the next month and get the refund?

Ans: Actually, the taxpayer will add the details in the following month and may be refunded.

Q.2 Do GSTR 2 and GSTR 3 Return do have to be filed for refund claims under GST?

Ans: If the Assess have filed GSTR 1 and GSTR 3B, they do not require to fill out any other forms to claim refunds.

Q.3 Is the Assess entitled to receive IGST refunds charged for the export of products if GSTR 3B has been submitted?

Ans: Actually, the taxpayer is entitled to obtain refunds if he has given details of the export products in GSTR 1 Table 6A and has filed GSTR 3B with the related tax details.