Tax Planning Tips towards availing Tax-saving/Benefits

Page Contents

Tax Planning Tips towards availing Tax-saving/Benefits

www.carajput.com; Save Income Tax

Tax Planning Tips towards availing Tax-saving/Benefits

Right now that most of us don’t start earning, we’re all wondering why someone needs to hear about the tax-savings mess. But when we get our first salaries and see the amount of tax reduced, we know how much efficient tax management is required.

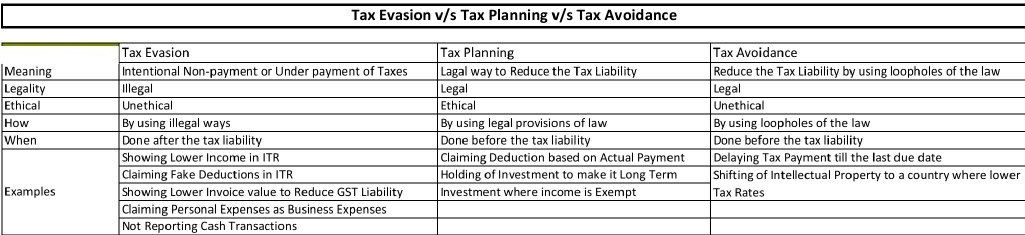

Tax Planning, Tax Avoidance, and Tax Evasion

Yet most of us are unable to take advantage of all the tax-saving opportunities that we have. Most of the time, we fail to claim a deduction under chapter VI i.e Section 80C, mostly because we don’t know about the investment that saves our tax and lack of understanding of other options.

Where would you save up to 78,000 annually?

| Investment | Tax applicable | Surcharge (4%) | Total amount | |

| In the U/s 80C (NPS, Term Life Insurance, ELSS, PPF, etc.) | ₹150,000 | ₹45,000 | ₹1,800 | ₹46,800 |

| NPS under Section 80CCD (1B) | ₹50,000 | ₹15,000 | ₹600 | ₹15,600 |

| Health insurance for self, family, and parents under Section 80D | ₹50,000 | ₹15,000 | ₹600 | ₹15,600 |

| Total tax savings | ₹78,000 | |||

Let’s address in depth the various sub-sections under Chapter VI deductions and other benefits :

In this blog, we’re going to tell you about some strategies that could save you tax above Rs. 1.5 lakh. Here are some possibilities that will help you invest money in tax benefits;

-

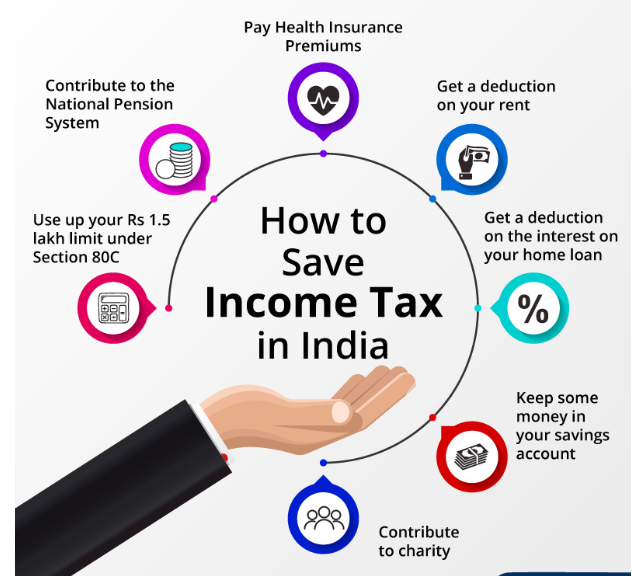

Investment in National Pension Scheme under Section 80CCD (1B)

Under Section 80C, you can claim a deduction of up to Rs 1.5 lakh by donating to the National pension scheme or NPS per year. Besides this, by adding another Rs 50,000 you will claim an extra deduction under Section 80CCD (1B).

This implies you can minimize your tax value by Rs 15,600 by investing in NPS if you fall below a 30 percent tax bracket. Also included in this is a 4 percent educational cess.

-

Health Insurance under Section 80D

Today health insurance is not an option but a requirement. If you do not have a health insurance policy then your financial stability will be negatively impacted by a medical crisis.

But health insurance policies come with some tax incentives so more and more consumers are adopting it.

Under Section 80D, you can obtain tax incentives for the additional payment charged for your insurance cover. And the incentives can be applied for – a regular life insurance policy, health insurance providers, and child-care plan as well.

You can also receive a tax deduction for routine health check-ups, as long as it is under the insurance coverage limits.

| Type of policy | Deduction limit from Tax |

| Individual, spouse & children, and if anyone is a senior citizen | Rs. 50,000 |

| Parents which are not senior citizens | Rs. 25,000 |

| The parent which is a senior citizen | Rs. 50,000 |

If your immediate family and not your parents are insured by the insurance scheme, then you can demand up to Rs 25,000 on the premium charged.

If an individual above the age of 60 is covered by the scheme then the maximum you can demand is Rs 50,000. Besides, if you have taken any scheme for your parents, then the premium is Rs 25,000 for non-senior citizens.

And it’s Rs 50000, for senior citizens. This is beyond the limitations of family protection.

Let us take a look at one case. Suppose Anil, a 35-year-old working professional, has acquired a health insurance policy covering him, his wife, and his child.

Under Section 80D, he may in a financial year claim up to Rs 25,0000 for this policy. This policy also includes preventive health check-ups.

For this policy, he pays Rs 18,000 each year and another Rs 4,000 for a preventive health check-up. Under Section 80D, he may claim a Rs 22,000 deduction.

Now for his parents, who are senior citizens, have taken another health policy. He will demand deductions up to Rs. 50,000 under this scheme. In total, he could claim a deduction for two policies up to Rs 75,000.

-

Disabled Dependent under Section 80DD

If a taxpayer caring for a disabled dependent, then he can claim tax deductions under Section 80DD. This deduction is provided as support to disabled family members.

A disability dependent may come under this section are spouse, children, parents, and sibling It may be any family member of the Hindu Undivided Family (HUF).

It is important to ensure that the disabled dependent has not claimed a deduction under section 80U for receiving compensation under this act. Under the section, Disabilities which are covered –

- Blindness

- Low vision

- Loco-motor disability

- Hearing impairment

- Mental retardation

- Mental illness

- Autism

- Cerebral palsy

May you demand deductions on Expenses for the care, caring, development, and rehabilitation of disabled persons.

- For the premium paid for these particular conditions on policies

- But the deduction amount depends on the severity of the disease. The taxpayer will demand deductions up to Rs 75,000 if the injury is up to 40 percent. If the individual with a disability is at least 80% disabled, then the taxpayer will demand a deduction up to Rs 1,25,000.

-

Interest on Education loan under Section 80E

Section 80E states that tax incentives can be obtained on the interest portion of an educational loan. And, that does not have a fixed limit.

This deduction can be received by either the student or the guardians, whoever makes the repayment. However, this advantage will be accessed from the first year of the loan to the eighth year or until the loan period is complete, whichever is earlier.

Let’s suppose, for example, you finish the repayment period within six years, so you will take advantage of the gain for six years.

On the other hand, even after the eight-year term, you will continue to repay the college debt, but in any situation, this tax incentive can not be taken advantage of.

-

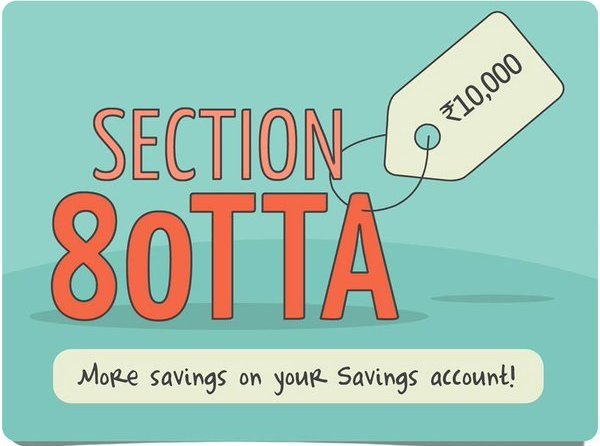

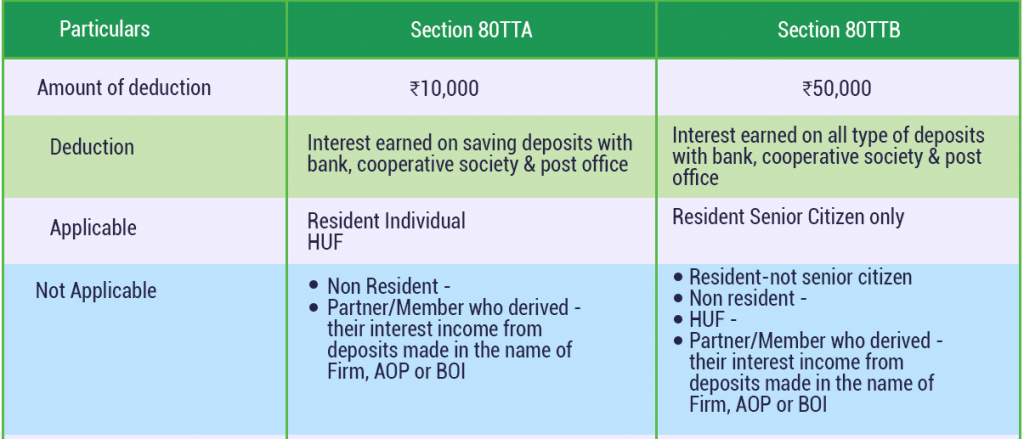

Interest on Saving Bank account under Section80TTA & 80TTB

We already have money in the banks and we get an interest in it. Any individual and HUF can claim a tax deduction on the interest paid.

Taxpayers who are not senior citizens which claim exemptions under Section 80TTA and senior citizens which demand tax under Section 80TTB.

Tax deductions can not be claimed on interest earned on Fixed deposits, Recurring deposits, or term deposits.

Section 80TTA:

Under this clause, the maximum amount to be deducted is Rs 10,000. You can demand a deduction of interest earned up to Rs 10,0000.

And if you have several savings accounts, the interest earned from all the deposits will be combined. Surplus income will be defined as income from other sources and taxable profits. This deduction is given on interest received –

- From a bank deposit account

- On savings account with a cooperative organization engaged in the banking industry

- From a savings account with a postal office

This deduction is NOT permitted for interest received on time deposits. Term deposits mean deposits that are repayable at the end of fixed periods. It is not permitted for –

- Interest in fixed deposits

- Earn Interest in recurrent deposits

- Any other deposits of time

Section 80TTTB:

This section was initiated as a reward for senior citizens to use as their source of revenue, interest earned by saving savings accounts and deposits on 1 April 2018. Senior citizens can assert tax deductions as high as Rs 50,000 under such a provision.

Amount of deductions allowed:

A deduction of less than Rs 50,000 or a sum from a defined income is permitted from the total income. Mentioned income is the sum of all of the following income:

- In case of Interest in deposit accounts (savings or fixed deposits);

- Interest in deposits held in a cooperative company engaged in banking operations, like a cooperative land mortgage bank or a cooperative land development bank; or

- and Interest in deposits at the post office

www.carajput.com; summary

-

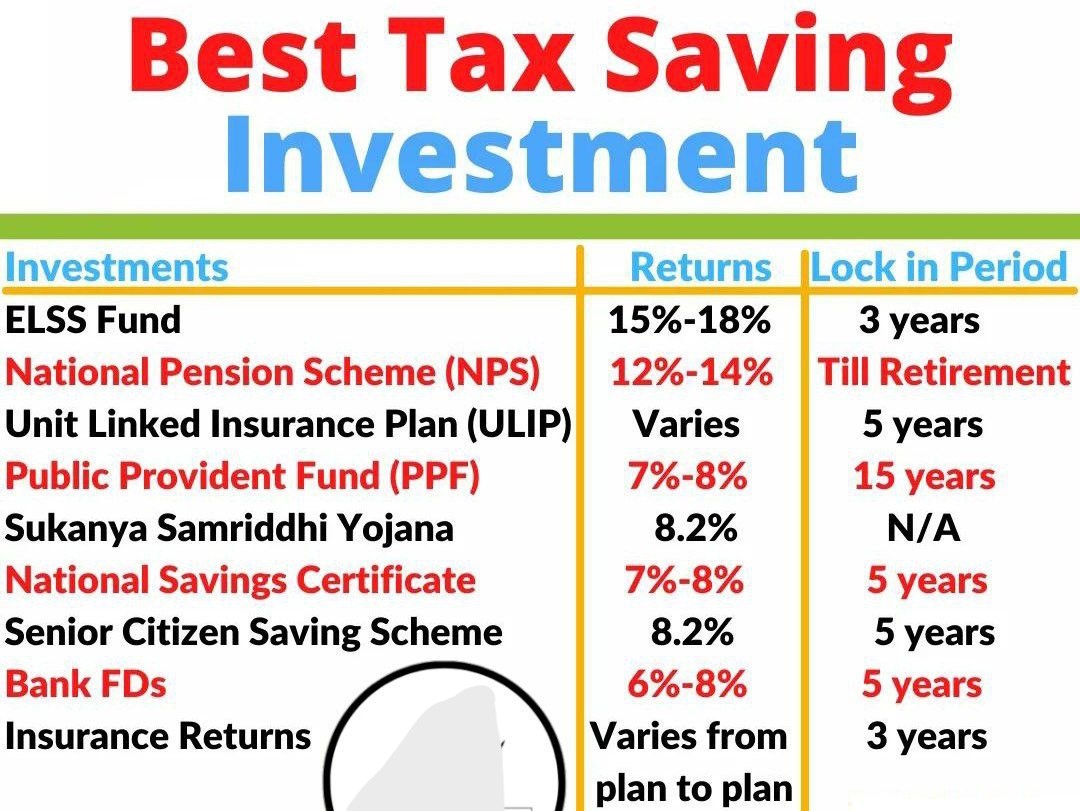

PPF (Public Provident Fund)

Established by the National Savings Organization and sponsored by the Government of India, PPF is a long-term fund (read 15 years) that you can use for purposes such as raising your child or retiring.

This ensures the investment you make, the profits you receive, and the gains from the growth are absolutely tax-free. You will also demand tax benefits for the amount you spend according to Section 80C of the Income Tax Act.

For PPF the minimum contribution is just Rs. 500. For a financial year, you can spend up to 1,50,000 Rs. The central government sets the interest rate for PPF along with many other savings schemes and revises the rates each quarter.

-

EPF (Employee Provident Fund)

T hat is only if, of course, you deduct the money after retirement! Premature withdrawal, if you have kept the EPF account for 5 consecutive years, is tax-free.

The amount of interest would be tax-free too. In accordance with Section 80C, you can demand tax deductions for the amount invested.

You should pay 12 percent of your basic salary to EPF compulsorily while your employer contributes equally. EPF includes a company employing 20 or more employees with a rate of 12 percent applied to these organizations. However, the EPF rules specify that under some requirements and conditions those organizations that have less than 20 employees will contribute to 10 percent.

You may also make voluntary contributions in excess of that limit. How much can you help? In your EPF, you could spend up to 100 percent of your minimum salary plus dearness allowance.

Both of the investments you make will receive the same rate of interest. The tax and withdrawal regulations would also be similar for such voluntary contributions.

Remember that the employer’s contribution to the Employee pension scheme (EPS) would be 8.33 percent. Rs 1250 will be spent in EPS for any employee whose basic salary is Rs. 15,000 or more.

If the basic salary is less than Rs. 15,000, so EPS will earn 8.33 percent of the wage. The average interest rate for EPF is 8.55 percent, measured on the basis of the monthly operating balance.

Assume you receive a basic salary of Rs. 50,000, the EPF balance will be Rs. 1.29 lakhs at the end of one year considering the existing interest rate. If you include the balance of your EPS it will be Rs. 1.34 lakhs.

Today, after one month of resigning from service, EPF customers will deduct 75 percent of their overall account balance.

-

ULIP (Unit-Linked Insurance Plan)

A portion of the ULIP premium, being a hybrid option, will go into insurance coverage and another portion will be deposited in the stock market.

The premium you pay counts under Section 80C for tax exemptions and the returns you will obtain on maturity will also be excluded from tax under Section 10(10D) of the Income Tax Act.

According to the Insurance Regulatory and Development Authority (IRDAI) of India, the overall annual fund management fees can be 1.35 percent.

The minimum insurance plan must therefore be 10 times the average premium, it has reported. These rules guarantee that the premiums do not reduce the returns, and insurance coverage is not negligible.

You can select from the fund options that insurer offers that come with various asset allocations. Based on your risk profile, investing in both equity and debt may allow you to invest more in equity, debt, or have a balanced approach. Post-tax returns from ULIPs may be between 7 percent -9 percent.

-

SSY (Sukanya Samridhi Yojana)

Are you going to have a baby girl? SSY is also one of the best long-term initiatives to produce tax-free returns. The average interest rate of the program is 8.1%. Pursuant to Section 80C, the money deposited will be registered as a tax deduction.

- The minimum deposit balance is Rs. 250 and you can invest Rs. 1.5 lakhs in a financial year.You can create an SSY account before your child turns 10. You’ll handle your account until you get married, or 21 years from the opening date of your account, whichever is earlier. Once she turns 18, you will make a partial withdrawal for your daughter’s education.

-

Contribution Given to political party

Section80GGC

- If, in the previous year, any individual except the local authority and any artificial legal entity, wholly or partially supported by the government, contributes to any political party or political trust.

- The tax incentive is required to pay 100% of the amount only if the donation is not paid in cash.

Section GGB

- If, in the preceding year, any Indian Corporation contributes to any political party or political trust and to the expenses incurred, directly or indirectly, by an advertising company in any publication by or on behalf of a political party.

- The deduction shall be given to 100% of the value of the donation only if the donation is not paid in cash.

-

Investment in notified equity saving scheme Section 80CCG

If a resident person (may be ordinarily resident or not ordinarily resident) invests in registered equity or listed unit or equity-oriented fund.

Tax benefit shall be given to a resident person for 3 financial years of assessment, beginning with the assessment year applicable to the preceding year in which the listed share or the listed share of the equity-oriented fund was first acquired.

The incentive is given at 50 percent of the amount invested, but the tax incentive is not allowed at more than Rs. 25.000.

-

Contribution to certain pension fund Section 80CCC

Where an individual has made a contribution of taxable income to LIC or to some other eligible insurer under an eligible pension scheme.

The tax benefit is the sum of the deposit of Rs. 1,50,000, whichever is less. However, the pension earned or the amount withdrawn by the applicant or his / her candidate is taxable in the year of receipt. There were also two subsections in this section:

Section 80CCD (1): NPS investments are eligible for tax deductions under this provision. Any Indian citizen between the ages of 18 and 60 can invest in NPS and make use of this tax benefit.

This profit may also be asserted by NRIs. The maximum deduction that can be made under this clause is 10% of your income (including basic salary + DA). For self-employed people, the cap is 20% of their gross net income. Also, the maximum profit you will enjoy per year under this section is 1.5 lakh.

Section 80CCD (1b): This clause allows for an extra deduction of 50,000 for investment in NPS. This is over and beyond the 1.5 lakh available in Section 80CCD(1).

So, in brief, you can make use of a total income tax deduction of 2 lakh a year when you invest in pension fund Section 80CCC i.e NPS.

-

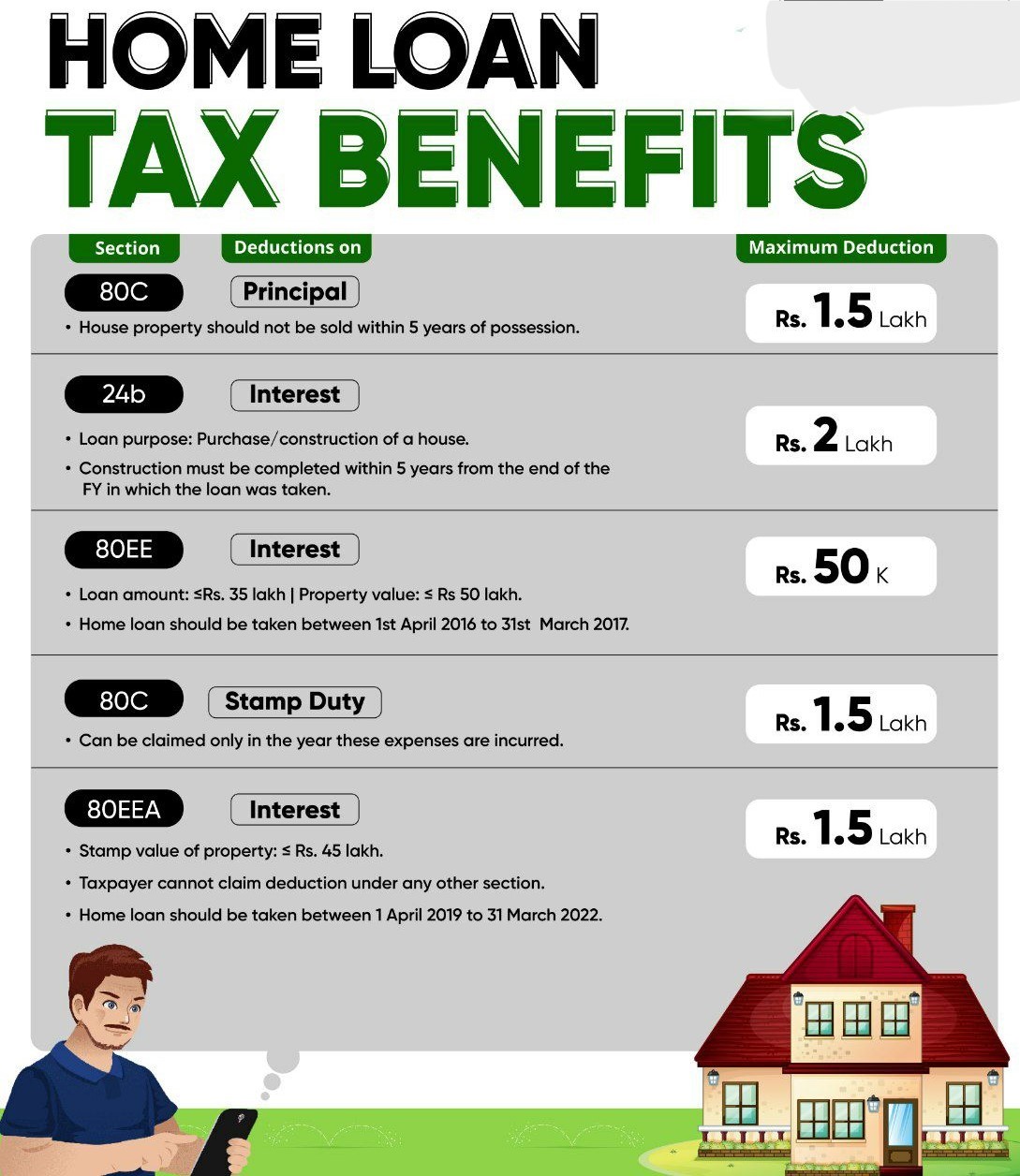

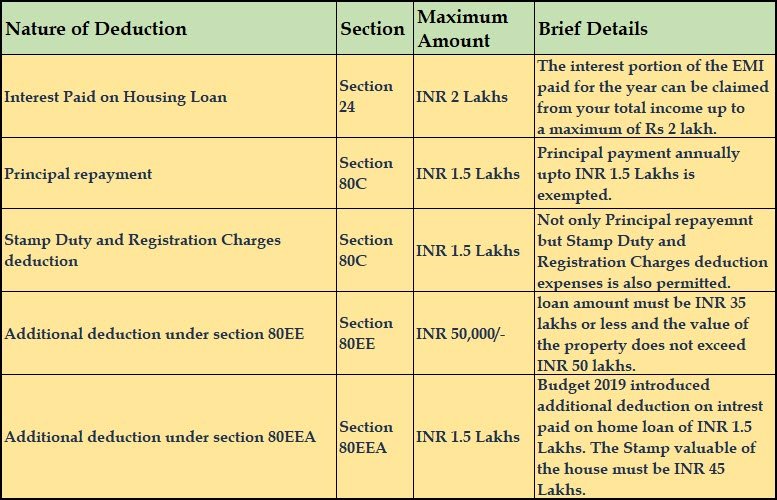

Housing Loan

Section 80C

- Housing loan principal payments: whether you have borrowed a home loan, the portion of EMI that is used to repay the principal sum is qualified for tax deductions under Section 80C. The amount you pay as interest is not eligible to claim deduction under this provision.

- If a person or HUF has taken a loan for his first house which is self-occupied or leased or vacant (deemed to be disposed of) then he may obtain a maximum tax reward of Rs. 1,50,000 only for payment of the principal amount repaid.

Section 80EE with Section 24 and Section 80EEA

- The deductions under this clause are only applicable to individuals. This means that whether you are a HUF, AOP, a corporation, or any other form of taxpayer, you can not assert any advantage under this clause.

- Limit of amount: this deduction (up to Rs. 50,000) exceeds the cap of Rs 2 lakh in compliance with section 24 of the Act on income tax. Learn more about the deduction of Rs 2 lakh on home loan interest here.

- In order to claim this deduction, you need not own any other property on the date of the approval of the loan from a financial institution.

- Conditions to be met for the claim deduction

House value should be Rs 50 lakhs or less

Loan to the house must be Rs 35 lakhs or less

When you’re in a position to comply with both Section 24 and Section 80EE of the Income Tax Act, be swift to assert the benefits. Next, reach the deductible maximum under section 24, which is Rs. 200,000.

Then proceed to claim additional benefits under section 80EE. In addition to the Rs 2 lakh limit authorized under section 24, these deductions are also permitted.

The additional deduction is allowed to the individual in respect of interest paid on loan taken for residential house property to provide benefits for first home buyers. The tax incentive shall not allow Rs. 50,000.

Union budget 2019 announced a new section 80EEA to increase the tax advantages of interest deductions to Rs 1,50,000 for housing loans for affordable homes over the term 1 April 2019 to 31 March 2020.

The taxpayer should be a first-time homeowner and should not be eligible for a tax deduction of 80EE. The tax incentive is only available until the repayment of the loan continues.

14. Section 80TTA

under Section 80TTA allows you to demand a deduction of Rs. 10,000 on your interest earnings. This deduction is really only applicable to individuals and to HUFs. The deduction shall be entitled on:

- Money earned in a savings bank account.

- income earned on a savings bank account with a cooperative organization engaged in banking activities

- Profit in a savings bank account with a post office

Your whole interest income would count as a deduction if it is less than 10,000. If your interest income is more than Rs. 10,000, your deduction shall be limited to Rs. 10,000.

CONCLUSION: What you need to know about saving income taxes

Prior to actually selecting a tax-saving instrument, it is necessary to take into account the degree of risk, lock-in time, liquidity, and returns.

There is no point in opting for a tax-saving plan unless it fits the particular needs as well. It also helps to keep up-to-date on the latest trends in tax-saving legislation.

Barring Section 80C, most taxpayers are not acquainted with some other parts of the Income Tax Act that allow them to substantially keep their tax burden. It is Strongly advised ways to save taxation under Sec 80C & 80D

- Investment Rs 1.5 lakh under Section 80C to limit your net income

- Buy Medical Insurance & seek a deduction of up to Rs. 25.000 (Rs. 50.000 for senior citizens) for a medical insurance premium under Section 80D.

- Claim deductions up to Rs 50,000 for housing loan Interest under Section 80EE

Best Tax Saving Investment & Schemes for FY 2023-24

Popular blog:-

Govt. scheme Launched for Public and National Benefits

National committee on deduction benefits u/s 35AC

Rajput Jain & Associates