Guide to Tax Implications on NRIs

Page Contents

A Guide to Tax Implications on NRIs

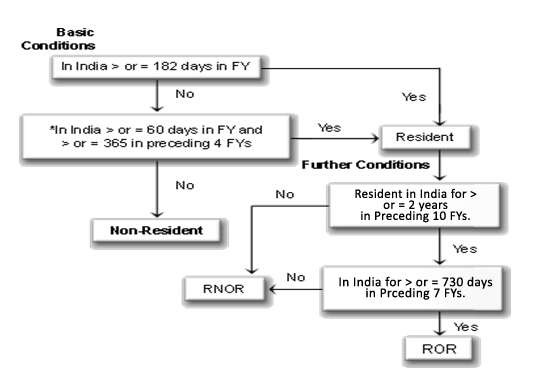

Who is considered as NRI?

If you do not satisfy any of the following conditions, A person shall be considered a non-resident of India (NRI).you will be an NRI if.

- In case you are in India during the financial year for at least 6 months (182 days to be exact)

- IF you are an Indian citizen who works abroad or is a member of a crew on an Indian ship in India and you have been in India for 2 months (60 days) in the last year and have lived for an entire year (365 days) in the last four years.

A person who is not a resident of India shall be considered a non-resident of India (NRI). You are a resident if you stay in India for a given financial year: 182 days or more or 60 days or more and 365 days or more in the four preceding years. In the event that you do not meet either of the above conditions, you will be regarded as an NRI.

FOR FY 2019-20 (I.E DURING COVID PANDEMIC)

If an individual has come to India on a visit before 22 March 2020 and

- has not been able to leave due to lockdown on or before 31 March 2020, the period of stay from 22 to 31 March is not considered for FY 2019-20.

- Quarantined due to Covid 19 on or following 1 March 2020 and departure on or before 31 March 2020 on an evacuation flight or failure to leave India on or after 1 March 2020 shall not be treated for the period from quarantine to quarantine.

- The period of stay from 22 March 2020 until departure shall not have been considered on the evacuation flight on or before 31 March 2020.

1.1 Key Points you have to know!

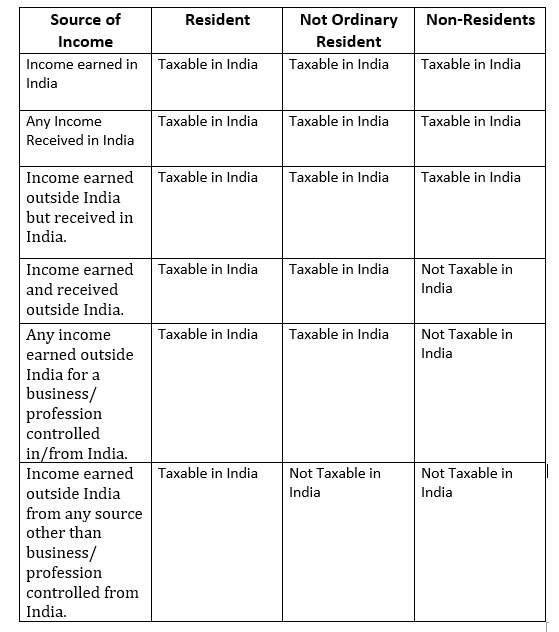

- The income taxes of an NRI in India would depend on his residential status for the year. Your global income is taxable in India if your status is ‘resident’. Your income that is received or accrued in India is taxable in India if your status is ‘NRI.’ Examples of income obtained or accrued in India are wages paid in India or salaries for services rendered in India, income from household assets located in India, capital gains on transfer of assets located in India, income from fixed deposits or interest on savings bank accounts. For an NRI, these profits are taxable. In India, income that is received outside India is not taxable. Interest gained on an account with NRE and FCNR is tax-free. NRO account interest is taxable on an NRI.

- Taxable Income for NRI

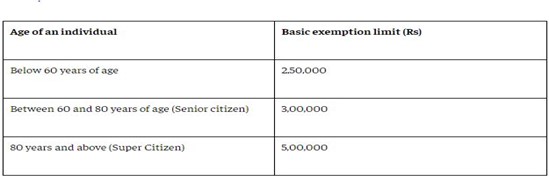

NRI or not, any person whose income exceeds Rs.2,50,000 is required in India to file an income tax return.

- July 31st is the last date in India for NRIs to file income tax returns.

- You are obligated to pay advance tax if the tax obligation reaches INR 10,000 in a FY. When you do not pay the advance tax, interest under Section 234B and Section 234C is applicable.

- Interest for defaults in furnishing return of income : Under Section 234A

- Moreover, Interest for defaults in payment of advance tax : Under Section 234B

- Payment of Advance tax not in time or Interest for deferment of advance tax : Under Section 234C

| Applicable Period for Amount on which Interest is Paid | Interest application for Period | Amount on which interest is calculated | Interest Rate |

| In case Advance Tax paid on or before June 15 is less than 15 percentage of Amount* | Three months | 15% of Amount* less tax already deposited before June 15 | interest @1% per month |

| In case Advance Tax paid on or before September 15 is less than 45 percentage of Amount* | Three months | 45% of Amount* less tax already deposited before September 15 | interest @1% per month |

| In case Advance Tax paid on or before December 15 is less than 75 percentage of Amount* | Three months | 75% of Amount* less tax already deposited before December 15 | interest @1% per month |

| In case Advance Tax paid on or before March 15 is less than 100 percentage of Amount* | Three months | 100% of Amount* less tax already deposited before March 15 | interest @1% per month |

When you earn your salary in India or anyone does it on your behalf, your salary income is taxable. Therefore, if you are an NRI and you earn your salary directly into an Indian account, Indian tax laws should apply to you. This benefit is charged at the slab rate to which you belong.

2.1 Income from salary

If your services are rendered in India, income from salary will be considered to arise in India. Even if you may be an NRI, but if your salaries are paid for services you provide to India, it is taxable in India irrelevant to where you receive your money.

- If your employer is the government of India and you are a resident of India, salary income is also taxed in India.

- if your service is made outside India. Remember that the salary of diplomats and ambassadors are exempt from tax.

2.2 House Property Income

For an NRI, income from a property located in India is taxable. The measurement of such income shall be carried out in the same way as that of the citizen.

- This property may be leased out or empty. An NRI is entitled to claim a standard deduction 30 %, deduct property taxes and take advantage of an interest deduction if a home loan exists.

- A deduction for principal repayment under Section 80C is also allowed by the NRI.

- Under Section 80C, stamp duty and registration charges payable on the purchase of a property may also be claimed.

- House property income is taxed as applicable at slab rates. Nandini owns a house in Goa and, while staying in Bangkok, she rented it out. She set up the rent payments to be paid directly from her Bangkok bank account.

- In India, Nandini’s income from this home, which is in India, shall be taxable.

2.3 Rental Payments to an NRI

A tenant who pays an NRI owner’s rent must agree to deduct 30 percent of the TDS. The income can be collected from an account in India or from the account of the NRI in the country in which it currently resides.

Maria is paying her NRI landlord of Rs 30,000 pm. Before transferring the amount to the landlord’s account, she must deduct 30 % of the total TDS (30,000 *30% = Rs 9,000). Maria also has to get a Form 15CA prepared and send it to the Department of Income Tax online.

Form 15CA must be submitted by a person making a remittance (a payment) to a Non-Resident Indian. This form must be submitted online. In some situations, before uploading Form 15CA online, a certificate from a chartered accountant on Form 15CB is required.

In Form 15CB, the CA certifies details of the payment, TDS rate, and TDS deduction as per Section 195 of the Income Tax Act, If any Double Tax Avoidance Agreement( DTAA ), and other details of the nature and intention of the transactions. There is no need for Form 15CB when:

- Remittance is not more than Rs 5,00,000 (in total in a financial year). In this case, only Form 15CA has to be addressed.

- If a lower TDS is to be deducted and a certificate is issued in compliance with Section 197, the order of the AO shall deduct the lower or lower TDS.

- If the transaction comes under Rule 37BB of the Income Tax Act, where it lists 28 items, neither is required. Here: check out the entire list. And New Rules related to 15CA and 15CB are attached

In all other situations, if a remittance is made outside India, the person making the remittance will receive a CA certificate on Form 15CB and will send Form 15CA to the government online after receiving the certificate.

2.4 Income from Other sources

- Interest income is taxable in India from fixed deposits and savings accounts kept in Indian bank accounts. Interest is tax-free on NRE and FCNR accounts. NRO account interest is completely taxable.

2.5 Income from Business and Profession

- Any revenue from a company operated or set up in India received by an NRI is taxable to the NRI.

2.6 Income from Gains in Capital

- Any capital gain arising from the transfer of capital assets situated in India is taxable in India. Capital gains on investments in shares in India and securities are also taxable in India. The buyer must deduct TDS at 20% if you sell a home property and have a long-term capital gain.

- However, by investing in a house property pursuant to Section 54 or investing in capital gain bonds pursuant to Section 54EC, you are entitled to invoke the capital gain exemption.

2.7 Special Investment Income Related Clause

- Individual (NRI) is taxed at 20 % when an NRI invests in certain Indian properties. If the only income the NRI has during the financial year is Special investment income then TDS has been deducted from that income, then such an NRI is not expected to file a tax return on income.

-

The Special Care Eligible Investments

Revenue from the following foreign currency-acquired Indian assets:

- Shares in an Indian public or private company

- Debentures of a public Indian company

- Deposits with banks and public Indian companies

- Securities from the Central Government

- NSC VI and VII issues

In this case, if the cost of the new asset is less than the net consideration, capital gains are proportionately exempt. Keep in mind that if the purchased new asset is transferred or sold back within 3 years, the exempted profit will be added to the income in the sale/transfer year.

Even when he/she becomes a resident, the above benefit may be available to the NRI before such an asset is transformed into money, and upon submission of a declaration by the NRI for the application of the special provisions to the assessing officer.

Income (investment income and LTCG) will be Charged to Tax Under the usual provision of the Income Tax Act if, the NRI may decide not to apply these special provisions.

-

Exemptions and Deductions for NRIs

- NRIs are also entitled, like residents, to obtain various deductions and exemptions from their overall income.

- NRIs still have most of the deductions U/s 80. A maximum deduction of up to Rs 1.5 lakhs is permitted under Section 80C from gross total income for an individual for FY 2020-21.

4.1 Deductions under Section 80C permitted to NRIs:

- Payment of the life insurance premium:

- The policy must be on behalf of the NRI or on behalf of their spouse or on behalf of any child (child may be dependent/independent, minor/major, or married/unmarried).

- The fee must be less than 10% of the total amount assured.

- Children’s tuition fees:

- Tuition fees charged for the full-time education of two children at any school, college, university, or other educational facility located within India (including payments for play school, pre-nursery and nursery).

- Principal reimbursement of loans for purchases of a building:

- Reimbursement of loans taken to buy or build a house is permitted.

- Stamp duty and other expenses for transferring the property to the NRI are also permitted to be paid.

- Unit Linked Insurance Plan (ULIPS):

- ULIPS is sold under Section 80C for life insurance coverage and includes the unit-linked LIC mutual fund coverage, e.g. Dhanraksha 1989 and the UTI insurance scheme for the other units.

- Investments in ELSS:

- In recent years, ELSS has been the most favored option as it allows you to claim a deduction under Section 80C up to Rs 1.5 lakhs, it provides taxpayers with the EEE (Exempt-Exempt-Exempt) benefit, and at the same time offers an excellent opportunity to earn as these funds invest mainly in a diversified way in the stock market.

4.2 Deductions not Authorized under Section 80C, below are not permitted to NRI

- PPF investment is not permitted (NRIs are not allowed to open new PPF accounts, however, PPF accounts which are opened while they are a resident are allowed to be maintained)

- NSCs investments

- 5-year deposit scheme by post office

- Savings Scheme for Senior Citizen

-

Other Allowable Deductions

In addition to the deduction that an NRI can claim under Section 80C, he is also eligible to claim other deduction under the income tax laws :

- House Property Income Deduction for NRIs

- NRIs can seek all the deductions applicable to a resident for a house purchased in India from house property income.

- The deduction is also allowed on property tax paid and interest on home loan deduction. Here you can read in dept about home property profits.

- Section 80D deduction

- NRIs are permitted to claim a health insurance premium deduction. This deduction is eligible for senior citizens up to Rs 30,000 (increased to Rs 50,000 effective 1 April 2018) and up to Rs 25,000 for self-, spouse-, and dependent children insurance in other cases.

- In addition,an NRI can also claim a deduction for parents insurance (father or mother or both) up to Rs30,000 (raised to Rs 50,000 effective April 1, 2018) for senior citizens, and for the parents who are not senior citizens is Rs 25000.

- A deduction of up to Rs 5,000 for preventive health check-ups is also available under the existing limit starting from FY 2012-13.

- Under Section 80E deduction

- NRIs can claim a deduction from interest paid on an education loan under this section. This loan may have been taken for the NRI, or the spouse or children of the NRI, or for a student for whom the NRI is a legal guardian for higher education.

- This deduction is valid for a maximum duration of 8 years or until interest is paid, whichever is earlier.

- The deduction for the principal repayment of the loan is not available.

- Under Section 80G deduction

- Under Section 80G, NRIs are permitted to demand a deduction for donations for social causes.

- Here are all the donations that are eligible under Section 80G.

- Section 80TTA Deduction

- Like Resident Indians, Non-resident Indians can also claim a deduction on income from interest on savings bank accounts up to a limit of Rs 10,000.

- This is permitted for savings account deposits (not time deposits) with a bank, cooperative Society or post office and is available since FY 2012-13.

- Investment as per “Rajiv Gandhi Equity Saving Scheme” RGESS (Section 80CCG)

- In the successful AY 2013-14, deductions under Section 80CCG or the Rajiv Gandhi Equity Savings Scheme were introduced.

- Primary aim behind this deduction was to increase the involvement among institutional investors in stock markets.

- The permissible deduction allowed under RGESS is 50% of the total amount invested s.t. Maximum investment of Rs 50,000. if certain requirements are met.

- NRIs do not have this deduction at their disposal. In respect of any assessment year starting on or after the 1st day of April 2018, no deduction under this section shall be permitted.

- Deduction under section 80CCG has been discontinued starting from 1st April 2017. Due to this phasing out, a new investor in Financial Year 2017-18 will not be eligible to claim the deduction under section 80CCG.

- Under Section 80DD Deduction for the Differently-Abled

- NRIs are eligible for deduction under this Section for maintenance including medical treatment of a handicapped dependent (person with a disability as specified in this Section).

- The Selling of Property Exemption for the NRI

- Long-term capital gains are taxed at 20% (when the property is owned for more than 3 years) . Remember that a TDS of 20% is subject to long-term capital gains gained by NRIs.

- Under Section 54, Section 54 EC & Section 54F on long-term capital gains, NRIs are entitled to claim exemptions. Therefore, at the time of filing a return, an NRI can take advantage of capital gains exemptions & demand a refund of TDS deducted from Capital Gains. There is an exception under Section 54 for long-term capital gains on the selling of a property.

- There is an exception under Section 54F for the selling of any asset other than the property of a building.

Popular Article :