An Overview Tax Audit

Page Contents

AN OVERVIEW on TAX AUDIT

- Tax Audit unde section 44AB was introduced by Finance Act 1984, w.e.f. 1st April 1985 (A. Y. 1985-86).

- The main objective of the tax audit was to ensure that Books of accounts and other relevant records are properly maintained by the assessee and to compute the taxable income according to the law and to maintain the transparency in the financial statements filed by the assessees with the Income-tax department.

Applicability of Section 44AB

- If the total sales/turnover/gross receipts in the business for the previous year or years exceeds or exceed Rs100,00,000, it is obligatory for a person carrying on such business to get his accounts audited, before the specified date.

- A person carrying on profession should get his accounts audited before the specified date if his gross receipts in profession for the previous year or years exceeds or exceed Rs 25,00,000.

- Where the accounts of a person are required to be audited under any other law, it is sufficient if such persons get his accounts audited under such other law before the specified date and obtain a report of such audit by the chartered accountant in the prescribed form by the said date.

- The specified date is 30th day of September of the assessment year.

- Provisions of compulsory audit do not apply to the person who derives income from the shipping business carried on by non-resident.

- Where an assessee is covered under section 44AE, 44BB or 44BBB but claims his income to be lower than presumptive income as specified by these sections then he is required to get his accounts audited even if his turnover/ gross receipts may not exceed the limits prescribed above.

- Further where an assessee is covered under section 44AD but claims his income to be lower than 8% of the turnover then he is required to get his accounts audited (irrespective of his turnover) provided his income exceeds the maximum amount which is not chargeable to Income tax in the previous year.

Liability to tax audit – special cases

- In case of an assessee carrying on business and at the same time engaged in a profession the provisions of section 44AB will be applicable if either his professional receipts or total sales turnover or gross receipts from business(anyone taken separately) exceeds the specified Limit.

- Where the assessee carries on more than one business activity, the results of all business activities should be clubbed together i.e the aggregate sales, turnover and/or gross receipts of all businesses carried on by an assessee would be taken into consideration in determining whether the limit of Rs 1 crores has been exceeded or not.

- However, where the business is covered by section 44B or 44BB or 44BBA or 44BBB,turnover of such business shall be excluded.

- Similarly when the business is covered by sections 44AD and 44AE and the assessee opts to be assessed under the respective sections on presumptive basis, the turnover thereof shall be excluded.

- So far as a partnership firm is concerned, each firm is an independent assessee for purposes of Income-tax Act. Therefore, the figures of sales of each firm will have to be considered separately for purposes of determining whether or not the accounts of such firm are required to be audited for purposes of section 44AB.

- It must also be understood that the issue whether the turnover exceeds Rs 1 crores in the case of business or the gross receipts exceed Rs.25 lakhs in the case of profession is to be determined in each year independent of the results obtained in the preceding year or years.

- Further, this section applies only if the turnover exceeds the prescribed limit according to the accounts maintained by the assessee.

- If the Assessing Officer wants the assessee to get his accounts audited in cases where the figures of turnover as appearing in the books of account of the assessee do not exceed the prescribed limits, he has no option but to pass an order under section 142(2A) directing the assessee to get his accounts audited from a particular chartered accountant as may be nominated by the Commissioner of Income-tax or the Chief Commissioner of Income-tax.

- In case of an assessee whose income is not chargeable to income-tax by reason of a specific exemption contained in the law or otherwise, as to whether he is required to get his accounts audited and to furnish such report under section 44AB.

- Such cases may cover those assessees who are wholly outside the purview of income-tax law as well as those whose income is otherwise exempt under the Act.

- Neither section 44AB nor any other provisions of the Act stipulate exemption from the compulsory tax audit to any person whose income is exempt from tax.

- This section makes it mandatory for every person carrying on any business or profession to get his accounts audited where conditions laid down in the section are satisfied.

- A charitable trust carrying on business may enjoy exemption under sections 10(21), 10(23), 10(23B) or section 10(23BB) or section 10(23C) and a research association carrying on business may enjoy exemptions under section 10(21) and section 11.

- A co-operative society carrying on business may enjoy exemption under section 80P.

- Such institutions/ associations of persons will have to get their accounts audited and to furnish such audit report for purposes of section 44AB if their turnover in business exceeds Rs 1 crores.

- But an agriculturist, who does not have any income under the head “Profits and gains of business or profession” chargeable to tax under the Act and who is not required to file any return under the said Act, need not get his accounts audited for purposes of section 44AB even though his total sales of agricultural products may exceed Rs 1 crores.

- It may be appreciated that the object of audit under section 44AB is only to assist the Assessing Officer in computing the total income of an assessee in accordance with different provisions of the Act.

- Therefore, even if the income of a person is below the taxable limit laid down in the relevant Finance Act of a particular year, he will have to get his accounts audited and to furnish such report under section 44AB, if his turnover in business exceed Rs 1 crores.

- A non-resident assessee is also required to get his accounts audited and to furnish such report under section 44AB if his turnover exceeds the prescribed limits.

- This audit, however, would be confined only to the Indian operations carried out by the non-resident assessee since he is not chargeable to income-tax in India in respect of income accruing or arising or received outside India.

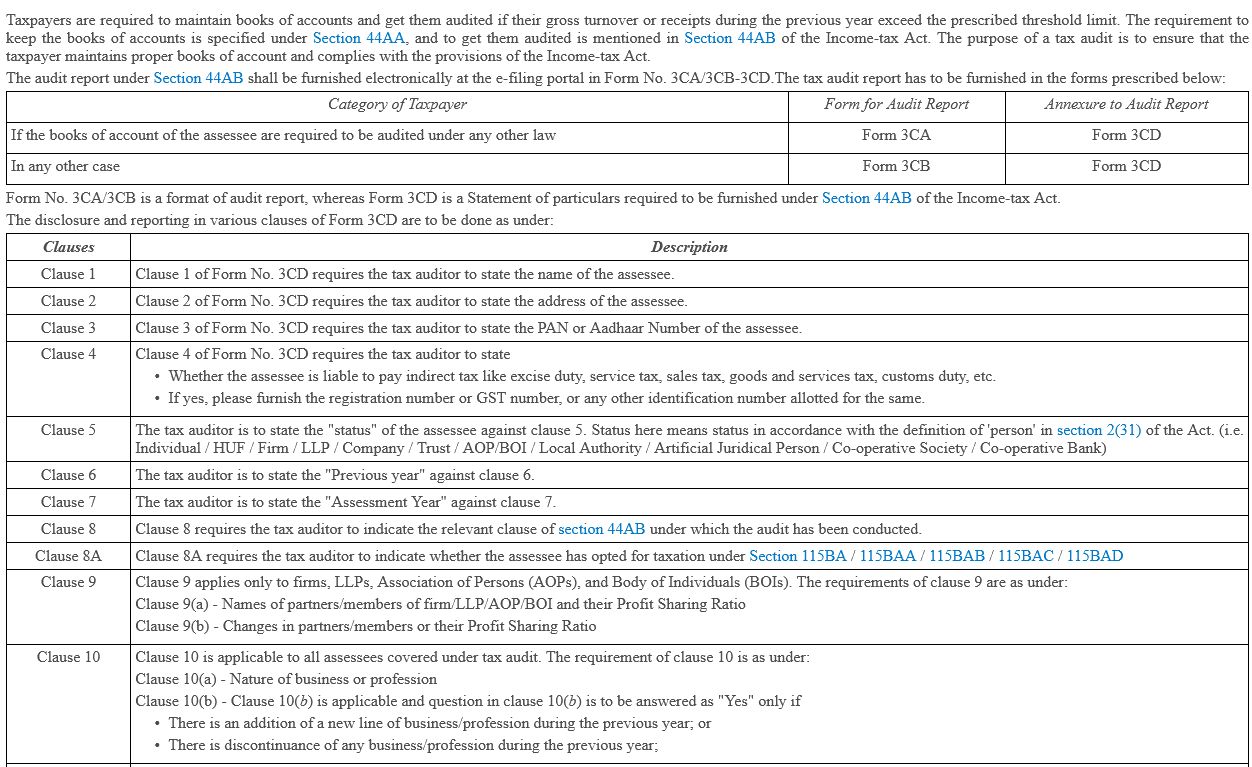

Forms to be used

The tax audit report should be submitted in the following forms:

- Assessee is required to get accounts audited under any other law and the financial year adopted for the purpose is the previous year,

Form No 3CA

- If the assessee is not required to get accounts audited under any other law,

Or

Where the assessee is required to get accounts audited under any other law but the financial year and the previous year is different.

Form No 3CB

- The particulars which are required to be furnished under section 44AB shall be in Form No. 3CD.

Profession’ and `business’

- As per Guidance note of the institute The term “business” includes any trade, commerce, or manufacture or any adventure or concern in the nature of trade, commerce or manufacture.

- The word `business’ is one of wide import and it means activity carried on continuously and systematically by a person by the application of his labour or skill with a view to earning an income.

- The expression “business” does not necessarily mean trade or manufacture only.Whether a particular activity can be classified as `business’ or `profession’ will depend on the facts and circumstances of each case.

- The expression “profession” involves the idea of an occupation requiring purely intellectual skill or manual skill controlled by the intellectual skill of the operator, as distinguished from an operation which is substantially the production or sale or arrangement for the production or sale, of commodities.

- The following have been listed out as professions in section 44AA and notified thereunder (Notifications No. SO-17(E) dated 12.1.77 and No.SO 2675 dated 25.9.1992):

- (i) Accountancy,(ii) Architectural (iii) Authorised Representative (iv) Company Secretary (v) Engineering (vi) Film Artists/Actors, Cameraman, Director, Singer, Story-writer,etc. (vii) Interior Decoration (viii) Legal (ix) Medical (x) Technical Consultancy

- The following activities have been held to be business:-

(i) Advertising agent (ii) Clearing, forwarding and shipping agents (iii) Couriers (iv) Insurance agent (v) Nursing home (vi) Stock and share broking and dealing in shares and securities (vii) Travel agent.

Sales, turnover, gross receipts

- The applicability of section 44AB depends upon the total sales, turnover or gross receipts in business or profession and therefore the meaning of the aforesaid terms has to be considered for the applicability of the section.

- The expression “Sales Turnover” means “The aggregate amount for which sales are effected or services rendered by an enterprise.

Items to be included in Turnover

- Adjustment not related to sales-bad debts written off, royalty, Sale of scrap, Sale of by product, Sales proceeds of any property, shares, securities, Debentures etc. held as stock-in-trade.

Items to be excluded from Turnover

- Goods returned, price adjustments, trade discount (but not the commission allowed to third parties)Cancellation of bills for the period under auditSales proceeds of any property, shares, securities, debentures, etc. held as investment.

- Where the invoices may involve various extra and ancillary charges such as packing, freight, forwarding, interest, commission, etc

- Then ordinarily the value of turnover should be disclosed exclusive of such ancillary and extra charges, except in those cases separate demarcation of such charges is not possible from the accounts or where the company’s billing procedure involves a composite charge inclusive of various services rather than a separate charge for each service.

- Cash discount if allowed in a cash memo/sales invoice is in the nature of a financing charge and is not related to turnover. The same should not be deducted from the figure of turnover.

- Turnover discount is normally allowed to a customer if the sales made to him exceed a particular quantity.

- This being dependent on the turnover, as per trade practice, it is in the nature of trade discount and should be deducted from the figure of turnover even if the same is allowed at periodical intervals by separate credit notes.

- Only brokerage which is being accounted for in the books of account of share brokers should be taken into account for considering the limits for the purpose of section 44AB.

- However, in case of transactions entered into by share broker on his personal account, the sale value should also be taken into account for considering the limit for the purpose of section 44AB.

- The same provisions will be applicable for sub-broker also.

“Gross receipts

- It will include all receipts whether in cash or in kind arising from carrying on of the business which will normally be assessable as business income under the Act.

- Broadly speaking, the following items of income and/or receipts would be covered by the term “gross receipts in business”:

i) Export Incentives such as Profits on sale of import licence, Cash assistance (by whatever name called) received or receivable by any person against exports and Duty Draw Back

ii) Interest received by the money lender;

iii) Commission, brokerage, service and other incidental charges received in the business of chit funds;

iv) Reimbursement of expenses incurred (e.g. packing, forwarding, freight, insurance, travelling etc.) and if the same is credited to a separate account in the books, only the net surplus on this account should be added to the turnover for the purposes of Section 44AB;

v) Hire charges of cold storage;

vi) Liquidated damages;

vii) Insurance claims – except for fixed assets;

viii) Sale proceeds of scrap, wastage etc. unless treated as part of sale or turnover, whether or not credited to miscellaneous income account;

ix) Gross receipts including lease rent in the business of operating lease;

x) Lease rent or interest on financing in the business of finance lease ; and

xi) Hire charges and instalments received in the course of hire purchase.

Items would not form part of “gross receipts in business” for purposes of section 44AB.

i) Sale proceeds of fixed assets;

ii) Sale proceeds of assets held as investments;

iii) Rental income unless the same is assessable as business income;

iv) Dividends on shares except in the case of an assessee dealing in shares

v) Income by way of interest unless assessable as business income;

vii) In the case of a recruiting agent, the advertisement charges received by him by way of reimbursement of expenses incurred by him;

viii) In the case of a travelling agent, the amount received from the clients for payment to the airlines, railways etc. where such amounts are received by way of reimbursement of expenses incurred on behalf of the client.

If, however, the travel agent is conducting a package tour and charges a consolidated sum for transportation, boarding and lodging and other facilities, then the amount received from the members of group tour should form part of gross receipts,

ix) In the case of an advertising agent, the amount of advertising charges recovered by him from his clients provided these are by way of reimbursement. But if the advertising agent books the advertisement space in bulk and recovers the charges from different clients, the amount received by him from the clients will not be the same as the charges paid by him and in such a case the amount recovered by him will form part of his gross receipts.

Gross receipts in business related Clarification:

- The basic principle to be applied is that if the assessee is merely reimbursed for certain expenses incurred, the same will not form part of his gross receipts.

- But in the case of charges recovered, which are not by way of reimbursement of the actual expenses incurred, they will form part of his gross receipts.

- In the case of a professional, the expression “gross receipts” in profession would include all receipts arising from carrying on of the profession.

- A question may, however, arise as to whether the out of pocket expenses received by him should form part of his gross receipts for purposes of this section.

- Normally, in the case of solicitors, advocates or chartered accountants, such out of pocket expenses received in advance are credited in a separate client’s account and utilised for making payments for stamp duties, registration fees, counsel’s fees, travelling expenses etc. on behalf of the clients.

- These amounts, if collected separately either in advance or otherwise, should not form part of the “gross receipts”.

- If, however, such out of pocket expenses are not specifically collected but are included/collected by way of a consolidated fee, the whole of the amount so collected shall form part of gross receipts and no adjustment should be made in respect of actual expenses paid by the professional person for and/or on behalf of his clients out of the gross fees so collected.

- However, the amount received by way of advance for which services are yet to be rendered will not form part of the receipts, as such advances are the liabilities of the assessee and cannot be treated as his receipts till the services are rendered.

Change of tax auditor

- Any practising chartered accountant cannot accept any appointment as auditor previously held by another chartered accountant without first communicating with him in writing.

- It will be in violation of clause(8) of Part I of First Schedule to the chartered accountants Act 1949. The communication must be effective one, hence it should be by registered AD or by hand delivery with written acknowledgement.

- Even though there is proper communication the incoming auditor should before acceptance must ensure all the undisputed fees must have been paid as per notification no 1CA(70/46/99dated28/10/99of ICAI.

ACCOUNTING STANDARDS

- Mandatory accounting standards are also applicable in respect of financial statements audited under Section 44 AB of the Income-tax Act, 1961.

- The institute has issued a number of accounting standards applicable to corporate/ non corporate entities.

- While discharging their attest function it will be the duty of the members of the Institute to ensure that the Accounting Standards are implemented in the presentation of financial statements covered by the Audit Reports.

- In the event of any non compliance of the accounting standards, it will be their duty to make adequate disclosures in their reports, so that the users of such statements may be aware of such deviation .

PENALTY FOR NON COMPLIANCE

- where any person is required to get his accounts audited under section 44AB but he fails to do so then he shall be liable for penalty under section 271B.

- The amount of penalty shall be .5% of turnover / gross receipts or Rs. 150000/- whichever is lower.

- However penalty u/s.271B would not be levied if reasonable causes existed, that prevented the assessee from filing return of income and obtaining audit report u/s.44AB.Penalty u/s.271B is discretionary and not mandatory.

Limitation on Number of Tax Audits

- The Institute of Chartered Accountants of India has prescribed ceiling on number of Tax audit assignments that can be accepted by any member in practice or by a firm of chartered accountants.

- This limit prescribed is 60 audits per member. But in case of partnership firms the limit will be applicable for all the partners taken together and a single partner can sign all the reports on behalf of the firm.

ICAI issue Tax Audit Guidance Note issued for Assessment Year 2022-23 (including Clause 44 which is applicable from AY 2022-23).

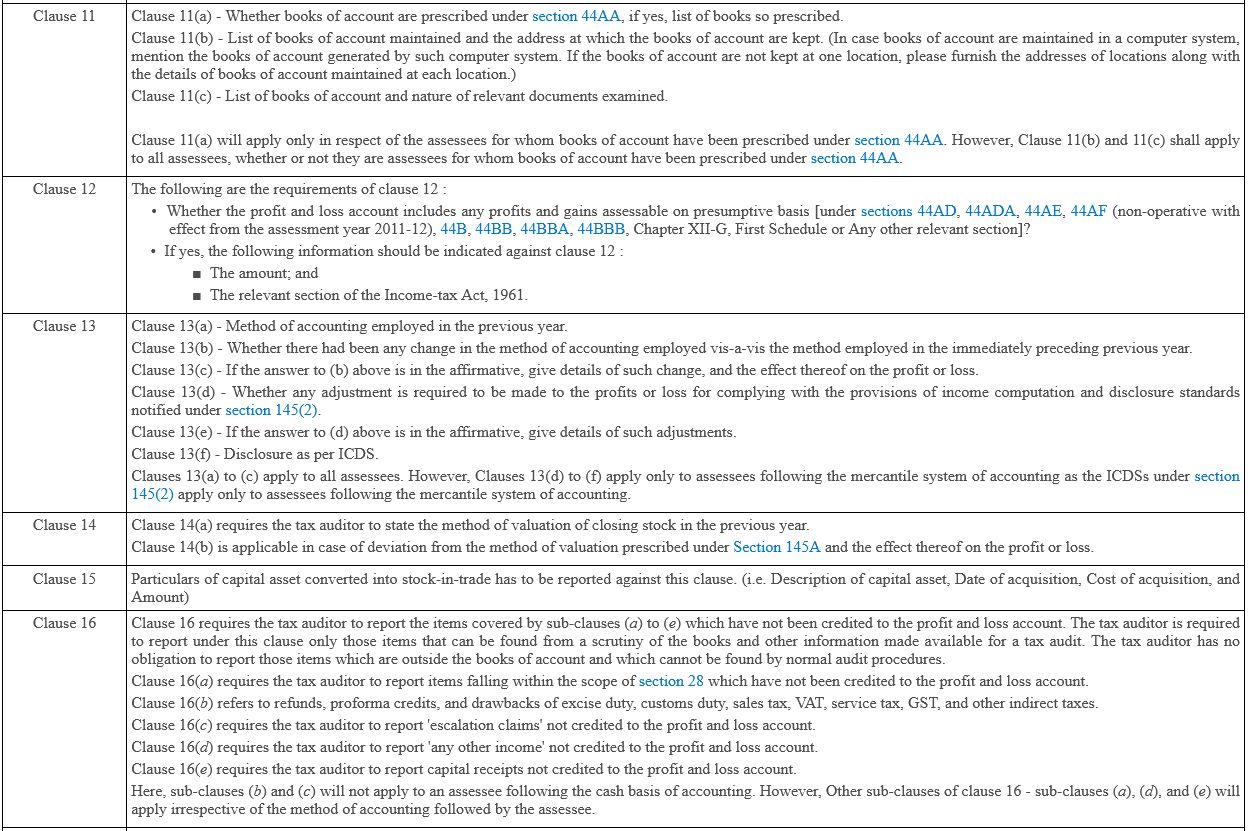

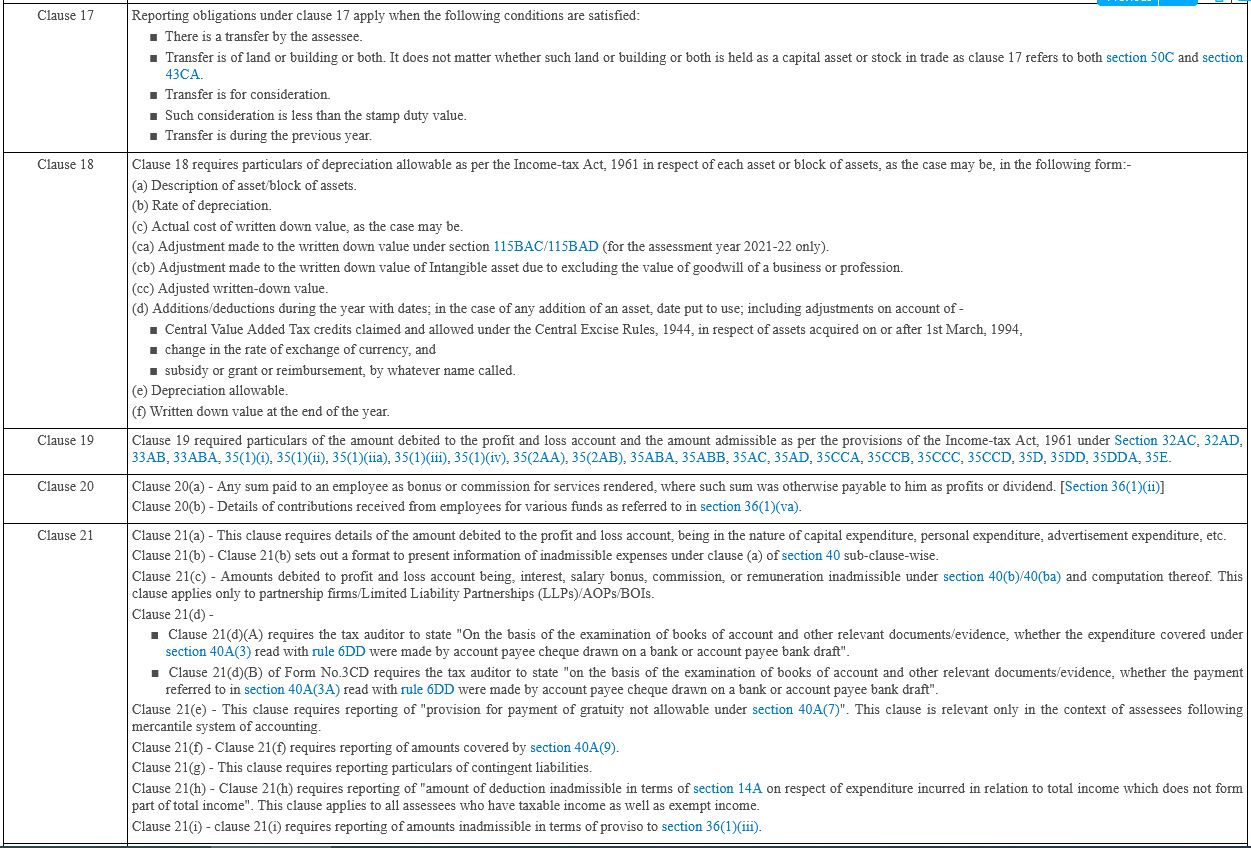

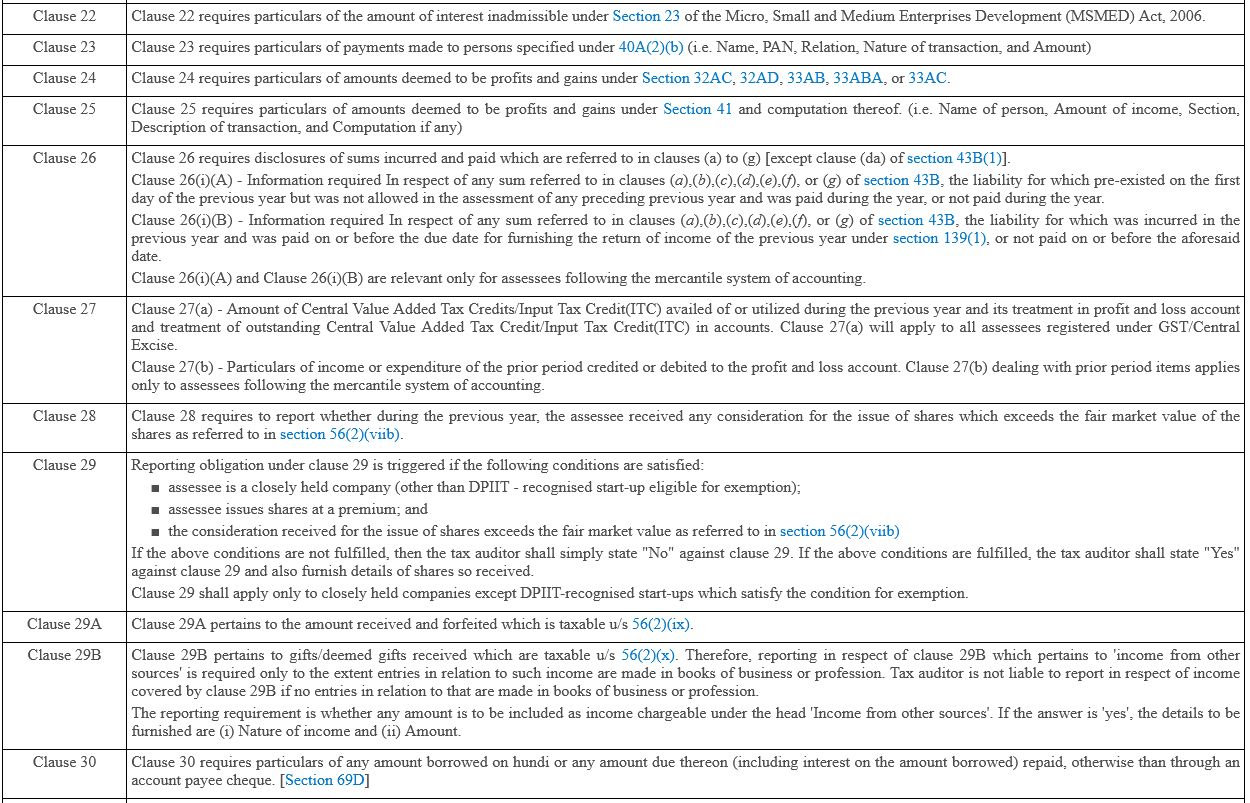

Tax Audit Clause by Clause Analysis

Popular Articles related to Tax Audit:

- Amendment in Tax Audit u/s 44AB

- Limit Applicable for tax Audit U/S 44 AB under Income Tax

- Tax Audit Check List

- Tax Audit Updated 01.08.2022 Under the Income Tax Act

- Overview of Tax Audit

- Amendment in section-44AB for Tax Audit

For query or help, contact: singh@carajput.com or call at 9555555480