GST Applicability on under Construction Flat Transactions

Page Contents

GST Applicability on under Construction Flat Transactions

Situation in Case of Services Tax

No Service Tax on Sale of Flats after issue of Occupancy Certificate

Recently, Press Information Bureau of Ministry of Finance has issued a press release dt. 26th October, 2015 to resolve a long standing issue relating to levy of Service Tax on sale of flats/dwellings etc. after issue of occupancy certificate but before issue of completion certificate in areas under the jurisdiction of Municipal Corporation of Greater Mumbai i.e. Brihanmumbai Municipal Corporation (BMC).

In the said release, it has been conveyed to the Service Tax Authorities in Mumbai, that sale of flats/dwellings etc., where the entire consideration is received after issue of occupancy certificate by BMC, leading to a mere transfer of title in immovable property, would fall outside the definition of “Service” as per Section 65B (44) of the Finance Act, 1994, and is therefore, not taxable.

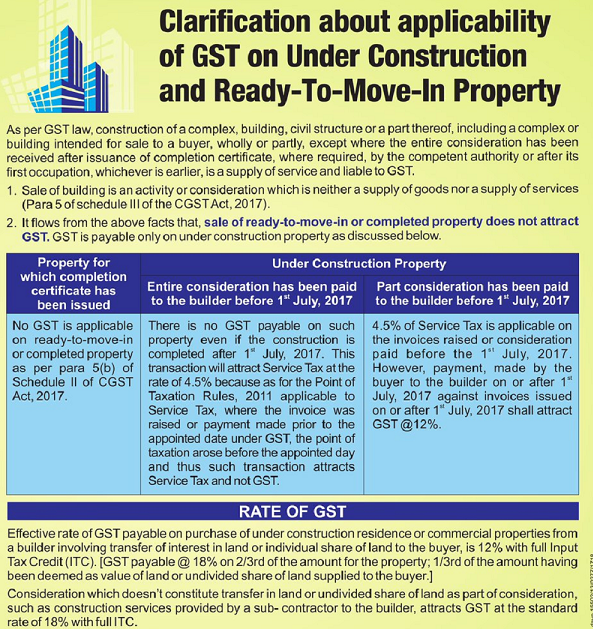

Situation in Case of GST

Honorable Karnataka’s Advance Ruling Authority (AAR) has upheld & Confirm that Consideration amounts received for sale of shares in flat will not attract GST in case Complete Sale Consideration is paid after issuance of completion certificate.

So we can say that no GST on Sale of Flats after issue of Occupancy Certificate

What are the reason of No GST applicable on ready to move flats?

- Goods and Services Tax on real estate is not applicable for sale of ready to move in flats, property going resale and purchase or sale of land. As per the Goods and Services Tax Act, purchase and sale activity does not include supply of services/goods. So there is no Goods and Services Tax is applicable to these kind of real estate transactions.

- It should be noted that Flat was booked under construction and thereafter construction has been completed after Goods and Services Tax Act come in to forces/implementation, and Occupancy Certificate or completion certificate has been received post implementation of GST then User/ owner is liable to pay GST.

- Finally, Its means to say that under construction transactions we needed to pay Goods and Services Tax.

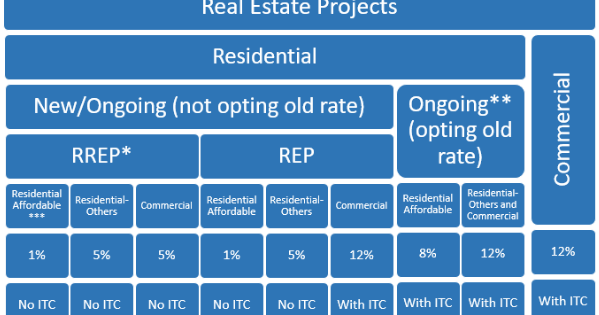

GST Rate & ITC Applicable on Real-Estate transaction

What is date of payment liability of GST on FSI/ TDR//LP on portion of unsold unit of project

- Date of liability of payment of GST shall arise on the date of completion or 1st occupation of the hosing project, as the case may be, whichever is earlier

GST Rate on unbooked residential apartment for FSI/ TDR//LP claimed as exempt

- Other Than Affordable housing unit- 5% (without input tax credit )

- For Affordable Housing unit – 1% (without input tax credit )

- In case commercial apartments such as shops, offices etc In a residential real estate project (RREP) (carpet area of Commercial apartment is not more then 15% of total carpet area of all apartment : 5% (without input tax credit )

- Above commercial apartments can also opt for ITC credit availability : 12% (with input tax credit related to commercial apartment)

Popular Articles :

- E-Invoice Mechanism under the GST

- Blocking/Unblocking the E-Way Bill creation system if fails to file GSTR-3B: GSTN

- Reasons for the Movement of Goods under the GST

- The due date for filing the Annual return

For query or help, contact: singh@carajput.com or call at 9555555480