Overview on TDS on Sale of Immovable Property

Page Contents

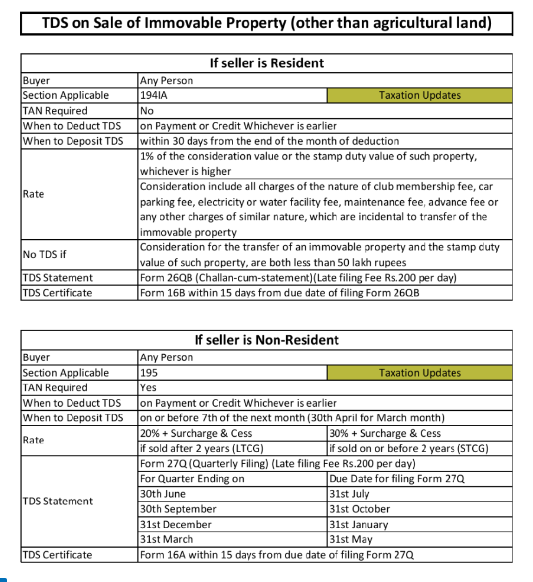

Tax deduction at source on Sale of Immovable Property

Income ax Ac provides that TDS will be applicable on transfers of immovable property when the property’s consideration exceeds or is equal to Rs 50 Lakhs. For all transactions starting on June 1, 2013, the buyer of the property has deducted Tax @ 1% while paying the sale consideration.

We offer the following services:

RJA are able to offer a whole range of solutions for the sale of properties by NRIs in India.

- We guide our clients from the first planning stages prior to the sale of their property to the restoration of the proceeds & also ensure that your tax returns are submitted effortlessly in both countries which including any DTAA benefits that may be available.

- Examining if financial repatriation or remittance is permissible.

- Providing guidance on any applicable limits or requirements.

- Providing a CA certificate (Form 15CB) and aiding with the self-declaration (Form 15CA) required for repatriation of monies out of India.

- We at RJA recognise the value of your time and are highly responsible when it comes to tax matters, ensuring that you receive the best advice possible in a timely manner.

- As Consultants, we make sure that your all the information is exchanged & preserved safely in the cloud. RJA uses specialized and sophisticated customer data management software to accomplish this goal.

-

TDS on Sale of Property by NRI

| Capital Gains Nature | Particulars | Applicable TDS Rate on Sale of Property by NRI |

| LTCG | Immovable Property held for greater than 2 years | 20 Percentage |

| SGST | Immovable Property held for less than Two Yrs | Seller Applicable Tax Slab Rates |

- Surcharge & Cess would also be levied on the all the above. So, Effective rate of TDS on property sale by Non Resident Indian in case of LTCG would be as below:

| Particulars | In case Property Sale Price (Rs.) | |||

| Less than 50 Lakhs | 50 Lakhs to 1 Cr | More than 1 Cr | ||

| LTCG Tax | Tax rate 20% | 20% | Tax rate 20% | |

| (Add) | Surcharge | Nil | 10% of above | 15% of above |

| Tax (incl Surcharge) | Tax rate 20% | 22% | 23% | |

| (Add) | Health and Ed. Cess | It will be levy @ 4% of above | 4% of above | It will be levy @4% of above |

| TDS Rate Applicable (including Cess & Surcharge) |

20.8% | 22.88% | 23.92% | |

| Particulars | Property Sale Price (Rs.) | ||

| 1 Cr to 2 Cr | 2 Cr to 5 Cr | ||

| LTCG Tax | Tax rate 20% | 20% | |

| (Add) | Surcharge | 25% of above | 37% of above |

| Tax (including Surcharge) | 25% | 27.4% | |

| (Add) | Health & Ed. Cess | 4% of above | 4% of above |

| Applicable TDS Rate (including Surcharge and Cess) |

26% | 28.496% | |

Non-Filing Of Form 26QB- Penalties Applicable

| Penal Interest | How to Calculation |

| Tax deduction at source Non-remittance | 1.5 Percentage per month for a period from the date on which Tax deduction at source is deducted to the actual date of payment. |

| Tax deduction at source Non-deduction | 1 Percentage per month for a period from date on which Tax deduction at source is deductible and collectable to the date on which Tax deduction at source and Tax collection at source is actually deducted. |

Pre-Sale Assistance

- Tax planning prior to a sale – Recognize your alternatives, such as reinvestment, repatriation, and the resulting cash flows, as well as potential global tax mitigation techniques.

- We’ll put you in touch with evaluated real estate consultants.

- Obtaining a certificate of lowers tax deduction from the Income Tax Department (subject to PAN jurisdiction) – This allows you to limit the amount of tax deducted at source to the amount of tax due on capital gains resulting from property.

Assistance during sale

- Capital gain computation.

- Assisting with the reinvestment of profits.

- Chartered Accountants certification is required for repatriation & remittance of funds.

Post-sale assistance

- We support on Filing revenue tax returns in India .

- Filing tax returns in your country (USA/Singapore/Australia).

- In your returns, you benefit from the Dual Tax Treaty available.

- Support for the income tax evaluation procedures, if any

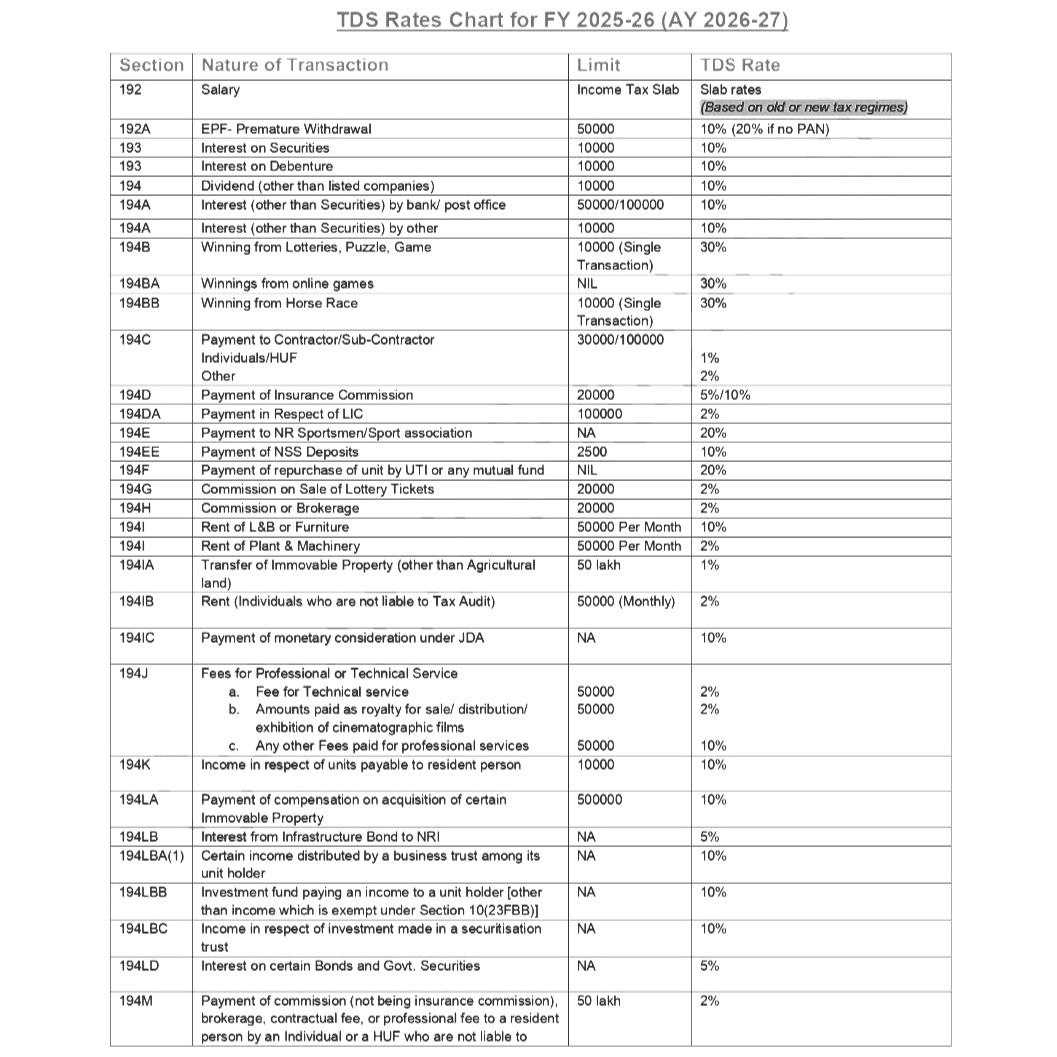

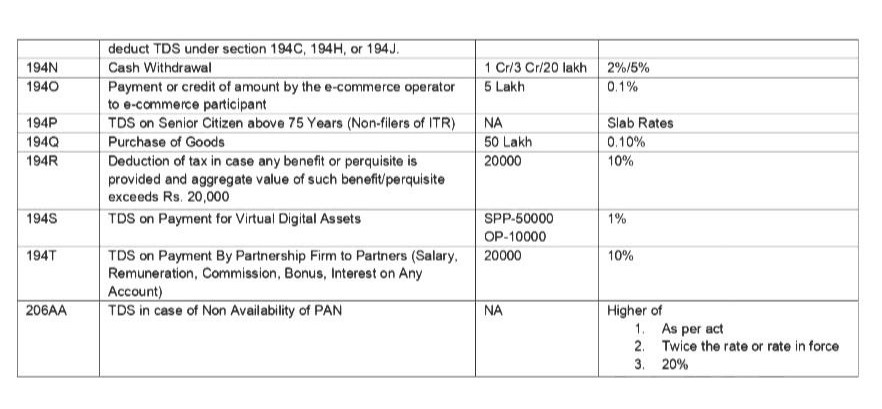

TDS Rates Chart for FY 2025-26 (AY 2026-27)

Popular blogs :