NRI Taxation : Filing of TDS & tax returns

Page Contents

NRI : Filing of Tax deduction at source & tax returns

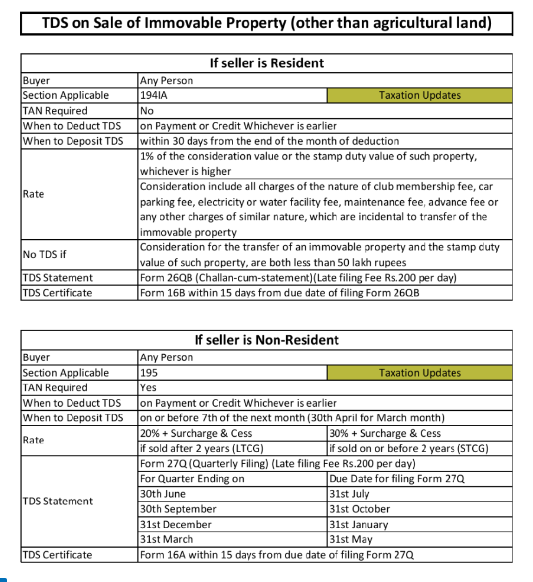

Whether tds u/s 194IA required to be deducted as property is owned by co-owners but stamp duty value is 51lac ?

- TDS (Tax Deducted at Source) under Section 194IA is required to be deducted if the value of the property transferred (as per stamp duty value) is more than Rs. 50 Lakhs.

- In case of co-owners, if the stamp duty value of the property is more than Rs. 50 Lakhs then TDS needs to be deducted. If multiple parties are there in the sale agreement, TDS is calculated on the pro-rata basis of the amount paid/credited to each co-owner.

- So If the stamp duty value of the property is more than 51Lac then TDS is required to be deducted under Section 194IA from the amount paid or credited to the co-owners as per their share.

It’s important to check the details of the transaction for the calculation of TDS, it is also important to issue TDS certificate and file the TDS return in a timely manner to avoid any late fee and interest.

Filing of TDS and Income tax returns:

- Specific income is taxed in one of the two nations and exempted in the other, according to the exemption mechanism.

- The income is taxed jointly with the countries listed in the income tax treaty when using the tax credit method.

- If you are an NRI living in Australia or the United States, you can take advantage of a special offer when you use RJA – NRI Taxation’s tax services. We assist you in filing your income tax returns in both India and Australia/USA.

- By signing a double taxation avoidance agreement, you can avoid paying tax twice. This can be accomplished in two ways: one through exemption and the other through tax credit.

- · Exemption Technique: The exemption method taxes specific income in one of the two nations while exempting it in the other.

- · Tax Credit Method: The income is taxed jointly with the countries listed in the income tax treaty under the tax credit method.

- If you are an NRI living in Australia or the United States, you can take advantage of a special offer when you use RJA – NRI Taxation’s tax services. We assist you in filing your income tax returns in both India and Australia/USA.

Repatriation of Fund from India

- The conversion of foreign currency to one’s domestic currency is referred to as repatriation. Once the property is sold and the money is transferred to your NRO account, you can use repatriation and remittance of funds as defined by the RBI to transfer the funds to your local bank account abroad.

- Under the “Liberalized Remittance Scheme,” the RBI has set certain limits on the amount of currency that can be transferred from India to abroad.

- The liberalized remittance scheme of 2004 allows for a transfer of USD 2,50,000 per financial year.

Repatriation of proceeds from the sale of property in India:

- NRIs, OCIs, and PIOs may repatriate funds from residential property sales outside of India.

- Seller purchased the immovable property in accordance with the provisions of the foreign exchange law in effect at the time of acquisition.

- Purchase price of the immovable property was paid in foreign currency obtained through banking channels or from funds held in an FCNR(B) or NRE account.

- [If an immobile property in India is bought from housing loans and repayments are made out of transfers from the outside via banking channels or by debit to that individual’s NRE/FCNR(B) account, such repayments may be treated as foreign exchange equivalent.].

- The remittance is limited to the sale proceeds of up to two immovable properties held by NRIs/PIOs in any given year, and is capped at $1 million.

Popular blogs :