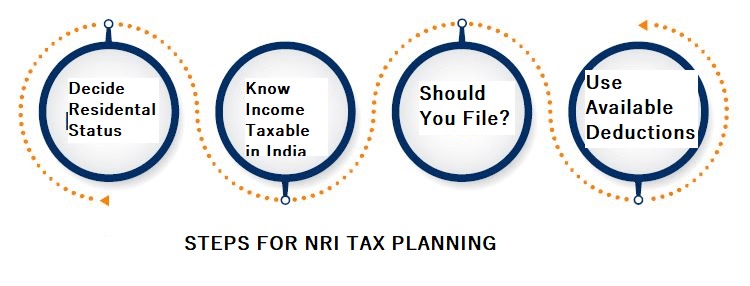

NON-RESIDENT INDIAN(NRI) INCOME TAXABLE IN INDIA

Page Contents

NON-RESIDENT INDIAN(NRI) INCOME TAXABLE IN INDIA

NON-RESIDENT INDIAN(NRI) INCOME TAXABLE IN INDIA

- Income from Salary: Your salary income is taxed in India under two situations.

-

- Situation A: If it’s received in India- If you’re an NRI and you have got received any salary in India directly into an Indian Account or somebody else has received it in your behalf in India, then such salary income would become taxable in India.

- Situation B: If it’s earned in India- Your income is claimed to be earned in India if it’s earned for services rendered in India. Therefore, if you’re a NRI and your salary earned is for the services rendered in India, it shall be taxed in India.

You will be taxed at the slab rate to which your income belongs to.

- Income from House Property: Income arising from property located in India, whether in the form of rented or lying vacant and the same be taxed for an NRI. The calculation of such income shall be within the same manner as for a resident.

An NRI, like resident is allowed

-

- A standard deduction of 30%,

• To deduct property taxes,

• To take advantage of interest deduction if there’s an equity credit line, and

• Claim the principal repayment of loan as deduction under section 80C. Also, tax and registration charges paid on purchase of a property can even be claimed under section 80C.

- A standard deduction of 30%,

It is to be noted that, where the income is received in NRO account, whether or not received directly, the same would be susceptible to tax in India since the source of income i.e., the property is situated in India.

- Income from Other Sources: Indian sourced income within the sort of interest on fixed deposits and saving accounts is taxable in India. However, the amount received in NRE and FCNR account shall be tax free, whereas that received in NRO account would be subject to taxation in India.

- Capital Gains: Any sought of capital gain arising in relation to transfer of capital asset, being situated in India, shall be taxed in India. Also, the capital gains on investments made in India in the form shares, securities shall be taxable in India.

Where an NRI sell a capital asset, being a house property, then

-

- TDS be deducted @ 20%, in case of Long-term capital gains, or

- TDS be deducted @30%, in case of Short-term capital gains.

The buyer whether or not he’s an individual is liable for deducting tax at source and paying it to the govt. Since the onus of deducting tax on payments made to NRI, lies on the customer, and hence the same shall obtain a Tax Deduction Account number (TAN) and issue a TDS certificate for the same.

SPECIFIC PROVISIONS WITH INVESTMENT INCOME OF NRI

As a NRI you’ll be able to avail of a special provision associated with investment income. A NRI income shall be taxed @ 20%, where he invests in certain assets in India.

INVESTMENTS ELIGIBLE FOR SPECIAL TREATMENT

The income derived from the subsequent assets in India acquired in foreign currency shall qualify for special treatment:

-

- Investment in the shares of Indian Companies (Public or Private company)

• Investment in the debentures, being issued by a publicly-listed Indian company.

• Deposits made with the banks and public companies.

• Any security of the Central Government

- Investment in the shares of Indian Companies (Public or Private company)

No deduction under Section 80 is going to be allowed while calculating investment income.

SPECIAL PROVISION IN RESPECT OF LONG-TERM CAPITAL GAINS

On long term capital gain arising from the transfer or sale of those assets, no advantage of indexation and deduction under Section 80 is allowed. But you’ll be able to still save your taxes, by availing exemption on the gains earned under Section 115F. Under this, you’re required to reinvest the web consideration received within the amount of six months from the date of sale of the first asset, into the subsequent assets:

-

- Shares in an Indian company

• Debentures of an Indian public company

• Deposits with banks and Indian public companies

• Central Government securities

• NSC VI and VII issues

- Shares in an Indian company

The entire capital gain would be exempt if the entire of the net consideration is re-invested. However, if the price of recent asset purchased, falls short than the consideration, then the capital gain would be exempt proportionately, i.e.,

Total Capital Gain X Cost of New Asset

—————————–

Total net consideration

Exemption=

NOTE: The exemption is withdrawn if the new asset purchased is transferred or converted into money within a period of three years from the date of purchase. The NRI is eligible to withdraw the amount from the special provision, at any point of time and in such an event, the investment income and LTCG shall be charged to tax as per the standard provisions of Income Tax Act, 1962.

Just like resident individuals, the NRIs have been provided with the exemptions under section 54, section 54EC and section 54F on long-term capital gains, arising on account of sale of house property. The long-term capital gain is often invested under:

| SECTION | ASSET SOLD/ TRANSFERRED | ASSET TO BE INVESTED IN | TIME PERIOD FOR INVESTMENT | QUANTUM OF EXEMPTION |

| 54 | · RESIDENTIAL HOUSE PROPERTY

· HOLDING PERIOD OF 3 OR MORE YEARS |

· RESIDENTIAL HOUSE PROPERTY IN INDIA |

· WITHIN ONE YEAR BEFORE THE DATE OF TRANSFER OF ASSET. · PURCHASED AFTER 2 YEARS FROM THE DATE OF TRANSFER OF ASSET. · CONSTRUCTION WITHIN 3 YEARS FROM THE DATE OF TRANSFER OF ASSET. · THE NEW ASSET CANNOT BE SOLD OR TRANSFERRED BEFORE THE END OF 3 YEARS. |

· WHERE THE ENTIRE CAPITAL GAIN HAS BEEN INVESTED FOR ACQUISITION OF NEW ASSET, THE FULL AMOUNT OF CAPITAL GAIN WOULD BE EXEMPTED.

· WHERE PARTIAL CAPITAL GAIN HAS BEEN INVESTED, THE CAPITAL GAIN NOT ADJUSTED IN NEW ASSET, SHALL BE CHARGED TO LONG-TERM CAPITAL GAIN TAX. |

| 54F | · CAPITAL ASSET OTHER THAN HOUSE PROPERTY

(NOTE: YOU SHOULD NOT OWN MORE THAN ONE RESIDENTIAL HOUSE PROPERTY AT THE TIME OF TRANSFER OF THE CAPITAL ASSET) |

· TO CLAIM FULL EXEMPTION, ENTIRE SALE PROCEEDS SHOULD BE INVESTED IN NEW ASSET.

· WHERE THE PARTIAL INVESTMENT HAS BEEN MADE, THE EXEMPTION WOULD BE: COST OF THE NEW HOUSE X CAPITAL GAINS SALE RECEIPTS |

||

| 54EC | · CAPITAL ASSET BEING RESIDENTIAL HOUSE PROPERTY | · BONDS OF NATIONAL HIGHWAY AUTHORITY OF INDIA (NHAI) OR RURAL ELECTRIFICATION CORPORATION (REC) | · THE SAID INVESTMENT BE MADE WITHIN 6 MONTHS FROM THE DATE OF TRANSFER.

· THE MAXIMUM AMOUNT OF INVESTMENT THAT CAN BE MADE IS RS. 50 LAKHS. · THE NEW ASSET CANNOT BE SOLD OR TRANSFERRED BEFORE THE END OF 3 YEARS. |

· AMOUNT INVESTED OUT OF CAPITAL GAIN; OR

· RS.50 LAKHS; WHICHEVER IS LOWER |

- Relevant proofs should be shown to the customer so no TDS is deducted by him.

• In case, the customer deducts TDS, advantage of these exemptions may be availed at the time of return filing by NRI and refund of such TDS may be claimed.

DEDUCTIONS AVAILABLE TO NRI

- Deduction under Section 80C:

The maximum amount of deduction available under the section is of Rs.1,50,000. Section 80C comprises of –

- Life premium Payments-

Deduction would be available, where the policy has been purchased in NRI’s name or in the name of his/her spouse or any child’s name. The premium must be but 10% of sum assured. - Tuition Fee Payment-

- NRI can claim deduction of tuition fees paid to any school, colleges or any universities situated in India for the aim of full-time education of their children.

- Principal repayment of home loans-

Like Residents, NRIs may claim deduction for principal repayment of house property loan borrowed for the needs of constructing or purchasing a residential house property. Other expenses like tax charges, registration fees, being incurred in respect of acquiring of such property, shall also be eligible. - Unit Linked Insurance Plan (ULIP)-

Investment in ULIP’s offers twin advantage of insurance and investment under one integrated plan. The lock-in period is of 5 years. Premium paid in respect of own, spouse and children shall be eligible for deduction. - Equity Linked Tax Saving Scheme (ELSS)-

- Deduction under Section 80D:

NRIs can claim deduction for premium got insurance of themselves and family or parents in India.

The three possible situations and tax benefits for every is shown below:

| POLICY TAKEN FOR | DEDUCTION ALLOWED | TOTAL TAX BENEFIT |

PARENTS BELOW 60 YEARS |

RS. 25,000

RS. 25,000 |

RS. 50,000 |

| 2. SELF, SPOUSE & CHILDREN BELOW 60;

PARENTS ABOVE 60 |

RS. 25,000

RS. 30,000 |

RS. 55,000 |

| 3. SELF, SPOUSE ABOVE 60 & CHILDREN;

PARENTS ABOVE 60 |

RS. 30,000

RS. 30,000 |

RS. 60,000 |

3. Deduction under Section 80E:

- Section 80E allows NRIs to assert a deduction of interest paid on an education loan. Such a loan shall be taken for pursuing higher education of the NRI, or his spouse or children or for a student, in respect of whom, the NRI is a trustee.

- There’s no limit on the number which might be claimed as a deduction under this section. The deduction shall be available, for the earlier of, period of 8 years or the interest is paid. No deduction would be available in respect of principal repayment of loan.

4. Deduction under Section 80G:

- Where the NRI makes eligible donations, as prescribed under section 80G of the IT Act, 1962, the same shall be eligible for deduction to NRIs.

Tax Rates on Capital Gains on Transfer of Securities (For Individuals and HUFs)