New requirements including in CARO 2020 reporting

Page Contents

NEW ADDITIONAL REQUIREMENTS INCLUDING IN THE CARO 2020 REPORTING AFTER ON CONSULTING ON WITH THE NFRA

Statutory Auditor’s Report (CARO 2020) shall include a statement a New Reporting Requirements

The existing COVID-19 pandemic affects not only public health but also the financial system as a whole. Public safety measures in place, although necessary are a huge hit to the economy’s liquidity flow leading to serious problems such as unemployment, a failure of the supply chain, a sudden drop in demand, unavailable inventories, etc.

The government provides various relief and relaxation measures to boost businesses and the economy. In the same sense, the MCA has postponed from FY 2019-20 to FY 2020-21 the applicability of the Companies (Auditor’s Report) Order, 2020 [CARO 2020].

The statement includes a Statutory auditor’s report (CARO 2020)

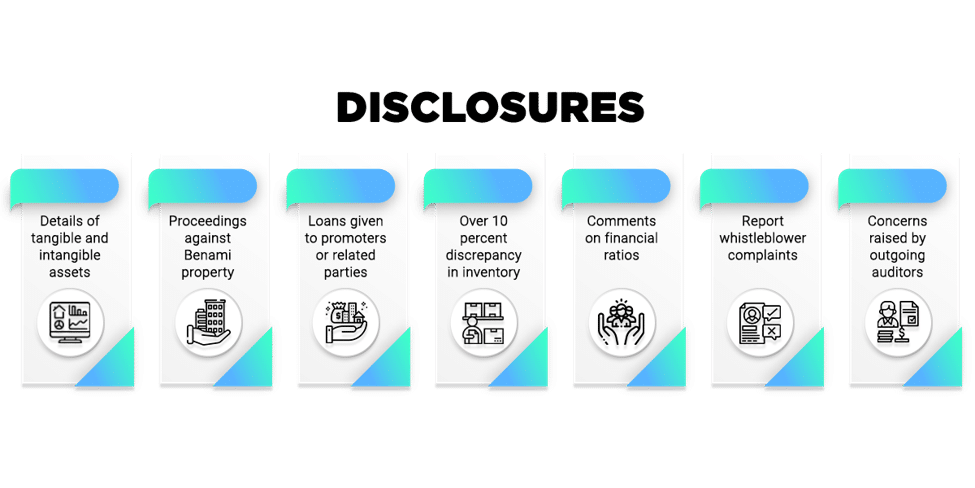

The Statutory auditor’s report (CARO 2020) shall include the following statement on the below matters, which are mentioned below:

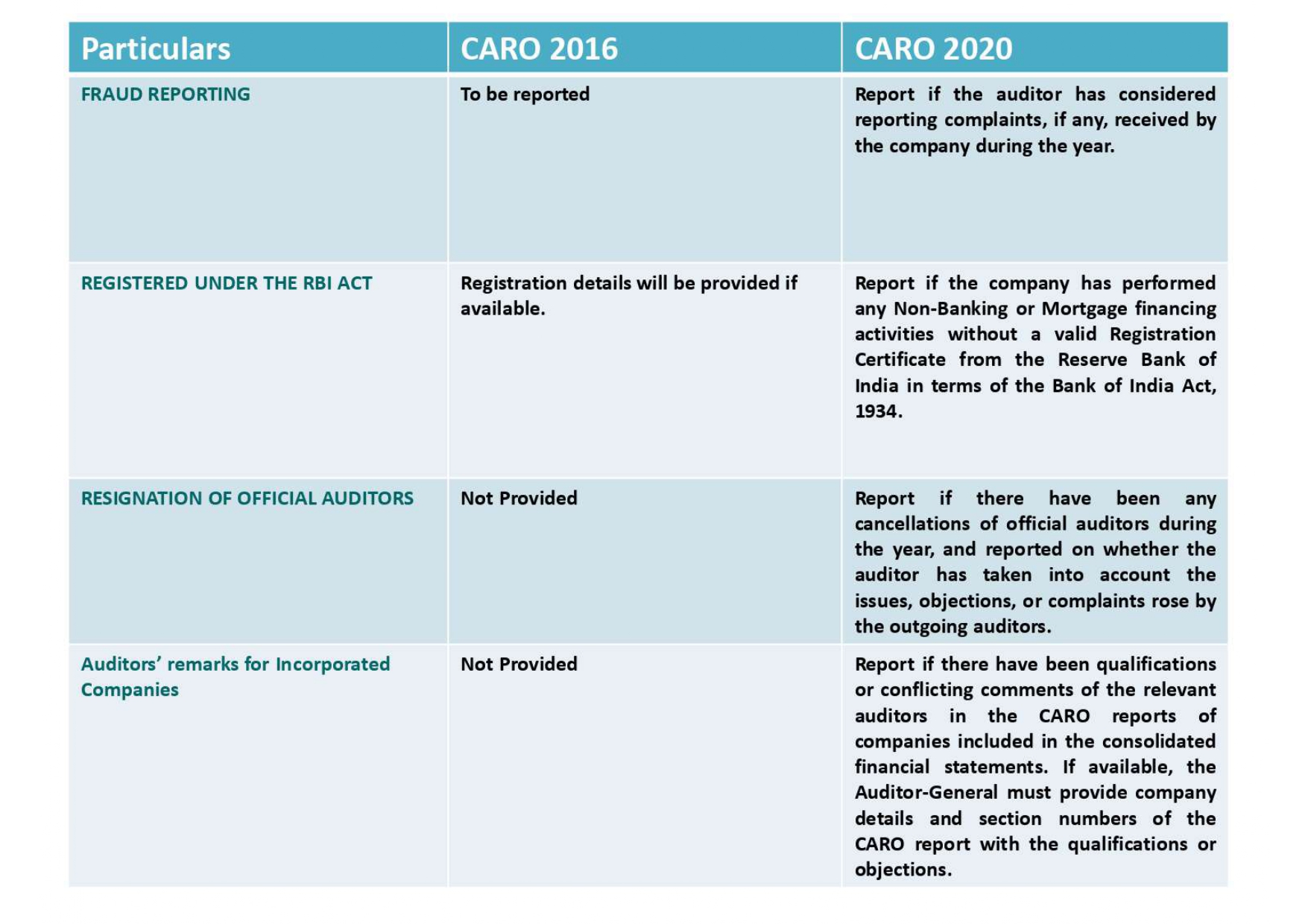

- Registration U/s 45-IA of RBI Act

- Total Cash losses information

- Information about the tangible and intangible assets

- Cost records Maintenance

- Total of statutory liabilities Deposit

- Completed unrecorded income which is required to be disclosed,

- Information of Default in repayment of borrowings

- Details of transfer to fund specified under Sch- VII of Co. Act

- Qualifications or adverse auditor remarks in other group companies

- Details of Compliance in respect of deposits accepted

- information of resignation of statutory auditors during the year

- any material uncertainty on meeting liabilities of the company.

- information of inventory and working capital

- complete details of investments, any guarantee or security or advances or loans given

- Compliance in respect of a loan to directors

- Funds raised and utilization

- Any pending Compliance by a Nidhi Company.

- Complete details Compliance on transactions with related parties

- Any Fraud & whistle-blower complaints

- Implementation of Internal audit system

- Non-cash dealings with company directors

In cases where the answer given by the Statutory auditor to any of the above requirements is unfavorable or negative, The auditor’s report shall then also set out the basis for such unfavorable or qualified response.

In addition, in cases in which the auditor is unable to give an opinion on any defined issue, the report shall state such fact together with the purposes why the auditor can not give an opinion on the same.

CARO 2020 Applicability on which of the Companies.

To improve the scope of the audit, the CARO 2020 was published by the MCA in consultation with the NFRA. It contains a list of topics that the relevant companies are obliged to report on.

CARO 2020 applies to all St. Audits beginning on or after 1 April 2020 which relates to the financial year 2019-20. The order applies to all companies covered under CARO 2016. Accordingly, the order requires all companies except the following companies which have been expressly prohibited from their jurisdiction:

- Companies registered for charitable purposes

- Small companies (Companies with paid-up capital less than/equal to Rs 50 lakh and with a last reported turnover which is less than/equal to Rs 2 Cr)

- Insurance companies

- One person company

- Banking companies

The Below Private Limited Companies are also exempt from CARO’s, 2020 requirements:

- Whose gross receipts or revenue (including revenue from discontinuing operations) is less than or equal to Rs 10 Cr in the financial year

- Whose paid-up share capital plus reserves is less than or equal to Rs 1 CR as on the Balance sheet date (i.e. usually at the end of the financial year )

- Not a holding or subsidiary of a Public company

- Whose borrowings is less than or equal to Rs 1 Cr at any time during the financial year

CARO, 2020 (Applicable from FY 2019-20)-Changes made

-

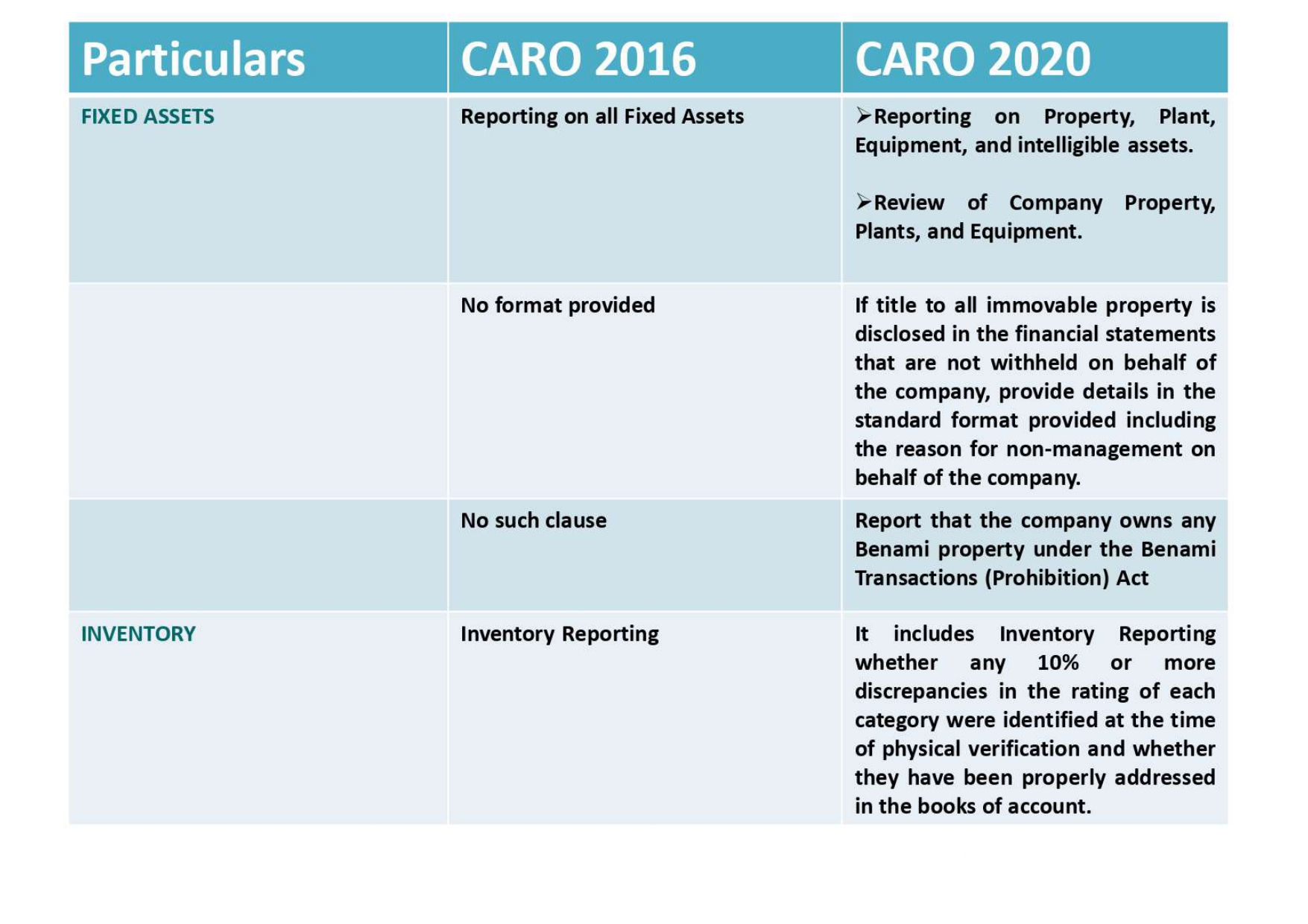

Fixed Assets/ Property, Plant, and Equipment

Reporting over maintenance of records of Intangible assets has been specifically added.

Leased Immovable property is specifically excluded from the reporting over the holding of title deeds in the Company’s name. If owned Immovable property is not held in the Company’s name, Dispute status and details of the registered owner need to be reported.

In the case of EPP revaluation, the auditor must determine that the same has been achieved on the basis of the Reported Interest survey. Changes ought to be recorded if 10% or more of the adjustments are made in the WDV.

-

Inventory

Inconsistencies recognized by management with an effect of 10% or more of the inventory value need to be reported.

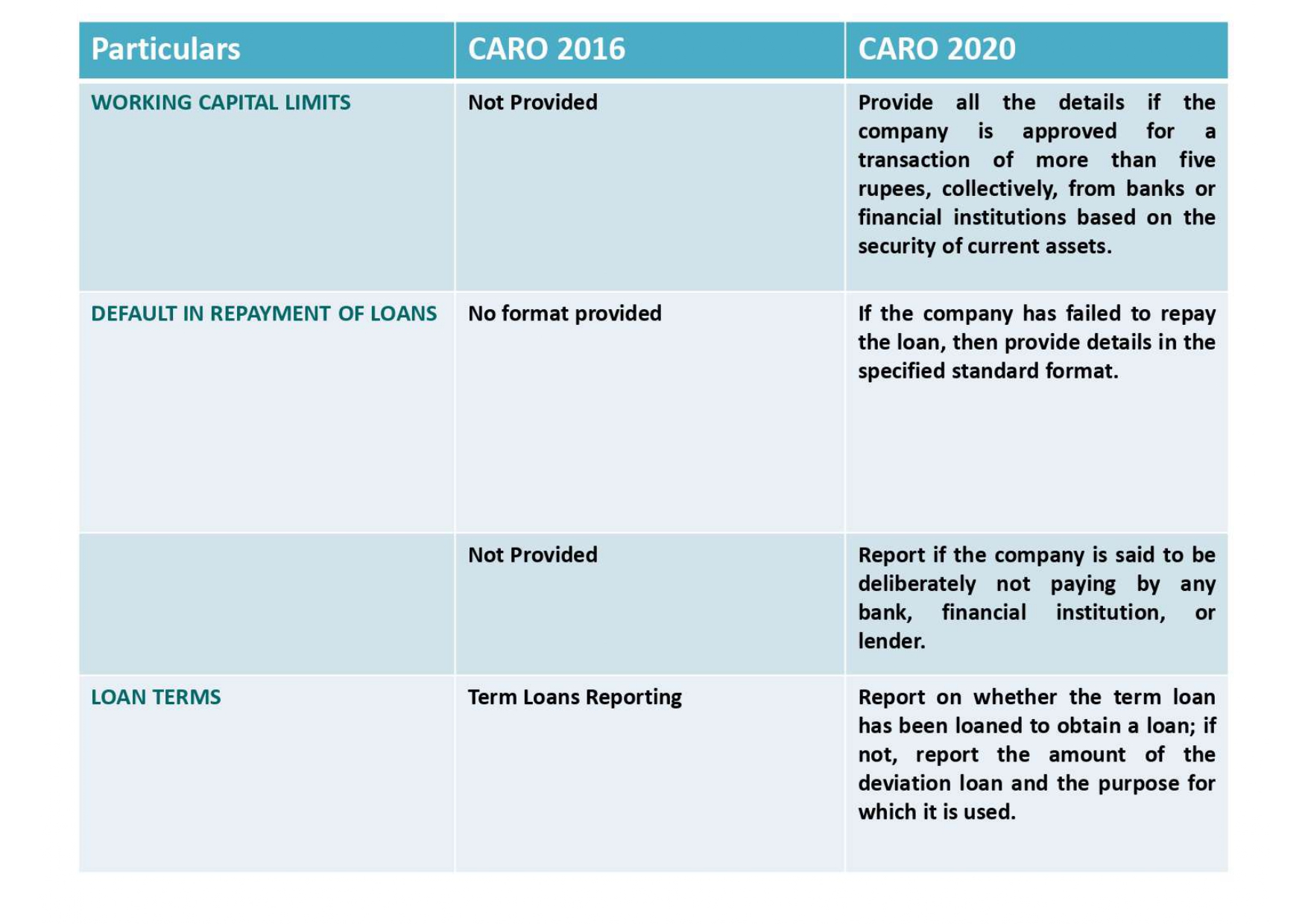

In the case that the Corporation has a working capital limit of more than INR 5 Crores depending on the security of the current assets (e.g. Stock, Debtors), the auditor must report that the regular filings (e.g. Financial Accounts, Debtors Listing) made with the lender are in compliance with the books.

-

Undisclosed Income:

The auditor must disclose whether or not any income has been returned under the Income Tax Act, 1961 and the same has been duly accounted for in the books of accounts.

-

Default in repayment of loans

The auditor must determine that the company is considered to be a “Willful defaulter.”

Information on the removal of term loans from allowable use needs to be published.

Data has been given on how short-term loans have been used for long-term purposes.

The auditor must comment on all money taken to meet the commitments of the community business.

Reporting on loans received by the Firm was made on the basis of the commitment of shares issued by the Firm to shareholders, Joint ventures, and associates.

- Fraud reporting

Fraud reporting has been extended to fraud against the Company by any person rather than by officers or employees in the past.

The fraud report issued by the auditors in the form of ADT-4 to CG should be reported.

The auditor has to record his evaluation of “Whistle Blower” allegations.

The auditor must report whether the internal audit system exists within the company and whether or not the internal audit reports have been considered.

The particulars of the proceedings (pending/initiated) under the Benami Law need to be published.

-

Consolidated Financial Statements

Details of consolidated companies with qualifications or adverse reactions in the CARO report must be reported along with the Paragraph Number of the auditor with the audit report on Consolidated Financial Activities.

-

Non-Banking Financial Activities

The auditor must report on the conduct of financial activities of an NBFC nature by the company without valid Certificates and reporting.

-

Cash Losses

The auditor will document whether the Company has suffered CASH LOSS during the current AND preceding financial year and the volume of such cash loss.

The resignation of the statutory auditor and the causes, problems with him duly considered by the incoming auditor or not; must be published.

-

Financial Ratios

The goals of the Organization to meet its Existing Obligations on the basis of percentages, maturity and plans for execution must be stated.

-

Corporate Social Responsibility:

The Auditor will disclose that the unexpended amount has been allocated to the designated fund within 6 months of the end of the fiscal year and whether or not the pending project balance has been moved to a special account. (Amendment itself under the Corporations Act, not yet told in 2013).

APPLICABILITY OF ANNEXES TO THE AUDITOR’S REPORT:

- Annexure of the CARO Report is not needed in the case of Small Business, Banking Firm, Insurance Company, Section 8 Company, One Person Company, and any private company having paid-up capital and free assets to INR 1 crores as at the balance sheet date and borrowing up to INR 1 crores at any time during the year and revenue up to INR 10 crores as per the financial reporting of the year mentioned.

- Annexure of the Internal Financial Control Report is not required in the case of Small Company, One Person Company, AND any Private Company with Turnover up to INR 50 Crores as per the financial statements of the year concerned and borrowing up to INR 25 Crores at any time during the year.

CONCLUSION:

- According to CARO 2020, disclosure is required as to whether any qualifications or adverse remarks have been made by the respective auditors in the CARO reports of the companies included in the consolidated financial statements, if yes, the company details and the CARO report sentence numbers usually contain the qualifications or adverse remarks should be noted.

- The CARO 2020 is supposed to substantially increase the overall standard of the audit reports on the company’s financial statements and thereby contribute to greater accountability and confidence in the company’s financial affairs. It is inevitably expected to increase the inflow of investment by and in Indian companies.

- In summary, we would like to say that the auditor’s reporting expectations are expanding substantially. Hoping this would lead to more public accountability between the company and its shareholders and hence the auditor needs to make sure he’s more perspective and especially while performing his duties.

Popular blog:-

- Rules and regulations of Audit and Assurance and corporate law compliance

- tally manual for tax audit report

- Draft Audit Report as per SA- 700(revised) incorporating CARO-2020