Mandatory annual compliances for a Private Limited Company

Page Contents

Annual Compliances for a Private Limited Company

This article is all about the annual compliances for a private limited company, before starting the topic there must be a brief understanding of a private limited company:-

What is a private limited company?

A private limited company is a company that is owned by a small group of individuals or by a group of members called shareholders.

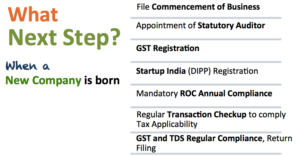

How to Incorporate a Private Limited Company?

There is a stepwise process to incorporate the Private limited company:-

Step 1: Submit an application for name approval through “RUN” in MCA Services.

Step 2: After approval of the name, the applicant has to prepare the necessary documents

(INC-9, DIR-2, NOC, office address proof, copy of utility bill, DSC of all directors)

Step 3: Fill the information in E-form “Spice” INC-32.

Step 4: Drafting Article of Association (AOA) and Memorandum of Association (MOA)

Step 5: Fill in the details of PAN and TAN

Step 6: If a company wants to apply for GST, IEC in AGILE, fill in the necessary details.

Step 7: After all the documents and information, submit the form on MCA.

Step 8: Certificate of Incorporation shall be generated with CIN, PAN, and TAN.

After a discussion on what is a private limited company and what is the process to incorporate it, to move forward with the main topic i.e., annual compliance for private limited companies.

First Board Meeting

The board of directors holds a board meeting within 30 days of incorporation of Company.

Subsequent Board Meeting

There should be minimum 4 board meetings in a calendar year and the gap is not more than 120 days in between the two meetings.

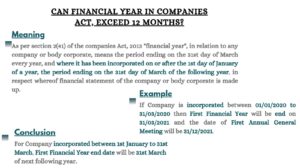

First Annual General Meeting

The first annual general meeting of the company will be held within a period of Nine months from the date of closing of the first financial year.

Subsequent Annual General Meeting

The subsequent annual general meeting of the company will be held within a period of six months from the date of closing of the financial year, and the gap between the first annual general meeting and next annual general meeting is not more than fifteen months.

Disclosures of Interest by Directors/Declaration

All the Director of the company shall disclose their interest in the Board meeting of the Board in every financial year in form MBP-1 and declaration in form DIR-8.

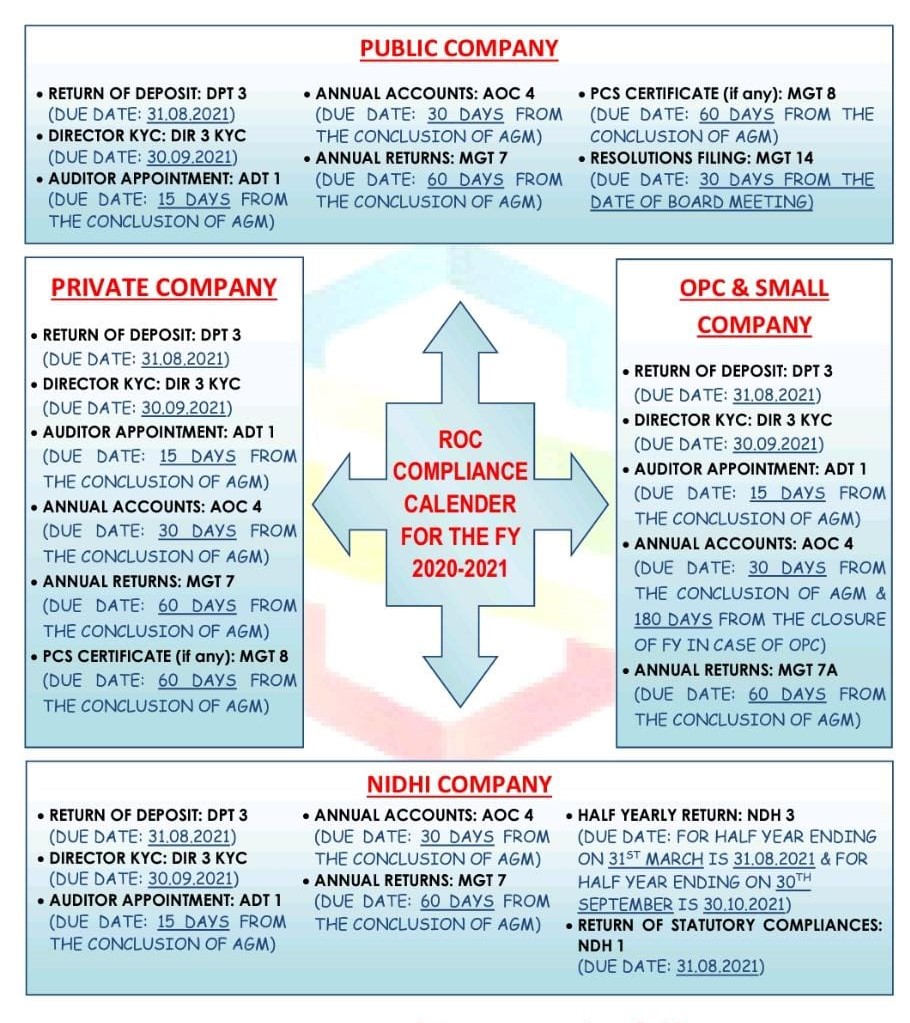

Appointment of First Auditor

The first auditor is appointed in the Board meeting within 30 days of incorporation. In case of failure, the members should appoint in EGM within 90 days.

Form: ADT-1 is to be filed

Consequences: There is not any financial risk for filing of form ADT-1, in case of appointment of the first auditor, i.e., it is the choice of the company to file it or not.

Appointment of Subsequent Auditor

The subsequent auditor is appointed in the annual general meeting for the next 5 years and the company should inform the ROC within 15 days from the date of AGM.

Filing of form ADT-1

The company should inform the ROC within 15 days from the date of appointment of the Auditor with the filing of Form ADT-1.

Form: ADT-1 is to be filed

Consequences: If the company does not file the ADT-1 on time, it will impact the financial position of the company.

| Fee for filing Form ADT-1 | |

| Share Capital of Company | Fees (Rs.) |

| Less than 1,00,000 | 200 |

| 1,00,000 to 4,99,999 | 300 |

| 5,00,000 to 24,99,999 | 400 |

| 25,00,000 to 99,99,999 | 500 |

| 1,00,00,000 or more | 600 |

| Not having capital | 200 |

| Penalty for non-filing of Form ADT-1 | |

| Delay in Filing (No. of days) | Penalty (Rs.) |

| Up to 30 days | 2 times of Normal fees |

| More than 30 to 60 days | 4 times Normal fees |

| More than 60 to 90 days | 6 times Normal fees |

| More than 90 to 180 days | 10 times of Normal fees |

| More than 180 days | 12 times of Normal fees |

Filing of Financial Statements i.e. form AOC-4

The company must file the form AOC-4 (Financial Statements) within thirty days from the date of Annual General Meeting (AGM).

Form: AOC-4 is to be filed

| Late Fees for Form AOC-4 | |

| Period of Delay | Additional Fees (Rs.) |

| Delay beyond the due dates to file AOC 4 | 100 per day |

| Note: In case of delay in filing the annual returns/balance sheet/financial statement the following fees is applicable: | |

Consequences: If the company not filed the AOC-4 on time, it will impact the financial position of the company.

| Fee for filing Form AOC-4 | |

| Share Capital of Company | Fees (Rs.) |

| Less than 1,00,000 | 200 |

| 1,00,000 to 4,99,999 | 300 |

| 5,00,000 to 24,99,999 | 400 |

| 25,00,000 to 99,99,999 | 500 |

| 1,00,00,000 or more | 600 |

| Late Fees for non-filing of Form AOC-4 | |

| Delay in Filing (No. of days) | Additional fees (Rs.) |

| Up to 30 days | 2 times of Normal fees |

| More than 30 to 60 days | 4 times of Normal fees |

| More than 60 to 90 days | 6 times of Normal fees |

| More than 90 to 180 days | 10 times of Normal fees |

| More than 180 days | 12 times of Normal fees |

| Note: In case of delay in filing the belated annual returns/balance sheet/financial statement the following fees is applicable: | |

| Penalty for non-filing Form AOC-4 | |

| Defaulting Party | Penalty Imposed |

| Company | Rs.1000 for every day subject to a maximum of Rs.10 Lakhs |

|

1. Managing Director/Chief Financial Officer 2. In the absence of the Managing Director/Chief Financial Officer-Any any other Director who the Board assigns the responsibility. 3. In case of the absence of any such Director-All directors of the company |

Rs.1 Lakh + Rs.100 per day of subject to a maximum of Rs.5 Lakhs |

Filing of Annual Return i.e. form MGT-7

The company must file the form MGT-7 (Annual Return) within sixty days from the date of Annual General Meeting (AGM).

Form: MGT-7 is to be filed

Consequences: If the company not filed the MGT-7 on time, it will impact the financial position of the company.

| Fee for filing Form MGT-7 | |

| Share Capital of Company | Fees (Rs.) |

| Less than 1,00,000 | 200 |

| 1,00,000 to 4,99,999 | 300 |

| 5,00,000 to 24,99,999 | 400 |

| 25,00,000 to 99,99,999 | 500 |

| 1,00,00,000 or more | 600 |

Late Fees for Form MGT-7 |

|

| Period of Delay | Additional Fees (Rs.) |

| Delay beyond the due dates to file MGT-7 | 100 per day |

| Note: In case of delay in filing the annual returns the company is required to pay the penalty. | |

Statutory Audit of Accounts

The company is required to prepare the financial statement (Balance Sheet, Profit & Loss) and must be audited by a Chartered Accountant every year.

Maintenance of Statutory Registers, Minutes books, and records

All the Companies are advised to prepare a few statutory registers in the prescribed format such as the register of members, register of charges, register of directors and KMP, register of loan and guarantee etc. Minutes of Board meeting and general meeting, Attendance Register, Books of Accounts, etc. are to be maintained.

Statutory register for private limited company

Filing of Income Tax Return of Company

| Particulars | Existing due date | Extended due date |

| Where tax audit / statutory audit / another audit under income tax act is applicable. | 30.10.2021 | 30.11.2021 |

| Where Transfer Pricing provisions are applicable | 30.11.2021 | 31.12.2021 |

Directors KYC

Every director of the company must do their KYC every year. The director KYC must do before 30th September from the end of every financial year.

Form: DIR-3 KYC

Consequences: De-activation of DIN and Penalty of Rs.5,000/- per director.

E-Form MSME-I

If the company has outstanding payments dues to micro and small enterprises and in case the payment of the same is pending beyond 45 days, then the Company has to furnish details as per the following timeline:

For April to September by 31st October

For October to March by 30th April

Form: MSME-I to be filed

Consequences: Non-compliance will lead to punishment and penalty under the provision of the Companies Act.

E-Form DPT-3

Every company if having any outstanding loan as on 31st March of every financial year has to give details and breakup of such outstanding amount irrespective of the fact whether such amount is falling under the definition of deposit or not by 30th June

Form: DPT-3 to be filed

Consequences: Non-compliance will lead to punishment and penalty under the provision of the Companies Act.

| Penalty for non-filing of Form DPT-3 | |

| Delay in Filing (No. of days) | Penalty (Rs.) |

| Up to 30 days | 2 times of Normal fees |

| More than 30 to 60 days | 4 times of Normal fees |

| More than 60 to 90 days | 6 times of Normal fees |

| More than 90 to 180 days | 10 times of Normal fees |

| More than 180 days | 12 times of Normal fees |

| Fee for filing Form DPT-3 | |

| Share Capital of Company | Fees (Rs.) |

| Less than 1,00,000 | 200 |

| 1,00,000 to 4,99,999 | 300 |

| 5,00,000 to 24,99,999 | 400 |

| 25,00,000 to 99,99,999 | 500 |

| 1,00,00,000 or more | 600 |

Popular Blog:-

Key Highlights of RACP Bill, 2020 and Companies (Amendment) Bill,2020

Summary of New MCA official updates under the Company Act 20

New Online filing eForm DIR-3 eKYC Directors

Compliance for Foreign Subsidiary Companies in India

Key Highlights of RACP Bill, 2020 and Companies (Amendment) Bill,2020

Summary of New MCA official updates under the Company Act 20