Interim Dividend as per Companies Act

Page Contents

Interim Dividend as per Companies Act

Brief Introduction

- In accordance with the Secretarial Standards, being issued by the Institute of Company Secretaries of India, Interim Dividend has been defined as the dividend which is declared by the Board of Directors.

- Such amount of dividend is declared and paid between two Annual General Meetings. Before declaration and payment of Interim Dividend, it’s advisable to require an opinion of Company’s Auditor as Interim Dividend is paid before Final Accounts of the corporate is ready and finalized.

- Unlike Final Dividend, Interim Dividend may be paid multiple times in an exceedingly year. Most of the companies tends to follow a practice of paying interim dividends on a quarterly or half-yearly basis.

- Rate of Interim Dividend is usually less than that of final Dividend.

- Board of directors have the authority to declare and pay Interim Dividend but on the opposite hand Shareholders of the corporate have the facility to revoke the choice of the Board and hence, refuse for the payment of Interim Dividend.

- Interim Dividend is typically declared by the Board of Directors when the corporate has sufficient earnings on top of expected.

Features of Interim Dividend

Interim Dividend Features are mention below :-

- Declaration by the Board- Under the Companies Act, 2013, the authority for declaration and payment of Interim Dividend has been vested only with the BOD’s (Board of Directors) and hence, there is no interference of shareholders in the same.

- Articles shall authorize- AOA(Articles of Association) of the corporate shall authorize Board for declaration of Interim Dividend. If Articles don’t authorize then, it must get altered before declaration of same.

- Pass Board Resolution- BOD shall pass Board Resolution within the committee meeting convened to declare Interim Dividend.

- Free Reserves- Interim Dividend can’t be paid out of Free Reserves.

- Provide Depreciation- Before declaring Interim Dividend, the corporate shall provide depreciation for full year not for partial/proportionate year.

- Time Period- Amount of such dividend shall be paid to respective shareholders, within 30 days from the date of declaration of dividend.

- Transfer to Unpaid Dividend Account- In case dividend remains unclaimed or unpaid within seven days of expiry of thirty days of declaration, then such amount shall be transferred to “Unpaid Dividend Account”.

- Transfer to IEPF- Any amount of dividend remains unclaimed for a continuous period of seven years, the same shall be transferred to Investor Education and Protection fund.

- Separate Bank Account- Within 5 days of declaration of Dividend, Amount to be distributed as a Dividend shall be transferred to a separate bank account.

Also Read : income tax treatment of a company’s dividend

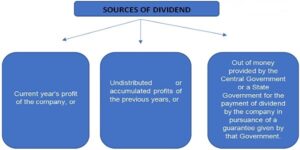

Sources of Payment of Interim Dividend

The amount of Interim Dividend be paid from:

- Surplus in profit and loss account.

- Out of Profit of current financial year that such Interim Dividend is paid.

- Profit generated within the year preceding the Quarter during which such Dividend is asserted.

It is commonly seen that the amount of Interim Dividend is paid out of retained earnings, which, to some extent, consists of undistributed profits of previous financial years.

Till the tip of the quarter immediately preceding the date of declaration of Interim Dividend if the corporate has incurred loss, then the rate of dividend on such shares shall not be on top of the average rate of dividend during the immediately preceding three years.

Situation under which dividend is not required to be paid

Key Considerations on Interim Dividend

Some of the basic key points, which the Board of Directors must consider are –

- Depreciation of whole year

- Tax including deferred tax of the corporate of whole year

- Losses which are anticipated for year

- Fixed rate of Dividend that’s required to be paid on preference shares

Difference between Interim and Final Dividend

| Interim Dividend | Final Dividend | |

| 1. | when Declared and paid by the Board of Directors of the company. | Recommended by Board of Directors but declared by the Shareholders. |

| 2. | Declared before the closure of Financial Year. | Declared in the Annual General Meeting at the end of the Year. |

| 3. | In this case Declared before the preparation of final accounts. | In this case Declared after preparation of final accounts. |

| 4. | Authorization of Articles of Association is required. | No such authorization is required in the Articles of Association. |

| 5. | Board Resolution be passed in the Board Meeting for the payment of Interim Dividend. | At the AGM of the company, Ordinary Resolution shall be passed for declaring Final Dividend. |

Procedure of Declaration & Payment on Interim Dividend

The procedure that’s required to be follow for the declaration & payment of dividend are as follows:

- At least 7 days’ notice of committee meeting shall be issued to every and each director of the corporate to call a committee meeting for a purpose of declaration of Interim Dividend.

- Board meeting shall be convened, and consideration of all matters associated with payment of Interim Dividend shall happen and it also includes:

o Ascertainment of financial position of the corporate

o Amount of dividend to be declared

o Fixation of record date

o Opening of bank account for the aim of transferring dividend

o Printing & granting authority for signing dividend warrants

o Pass Board Resolution for declaration and payment of Dividend.

- After passing Board resolution, separate bank account must be opened with the scheduled bank.

- Deposit the amount of Dividend payable therein account within five working days of declaration of such dividend.

- Dividend be paid to the respective shareholders, within 30 days from the date of declaration of said dividend.

- Where the amount of dividend remains unclaimed or unpaid, the same shall be transferred to a “Unpaid Dividend Account” and such transfer be made within 7 days from the expiration of thirty days from the date of declaration of such dividend.

- Within a period of ninety days of constructing any transfer in “Unpaid Dividend Account”, the corporate shall prepare an announcement containing names, address, etc and place it on a website, if any

- In case the a person desires to assert his amount of dividend from Unpaid Dividend account, then such person should apply in Form IEPF-5 to the corporate.

- Also, where any amount remains unclaimed in the “Unpaid Dividend Account” for a continuous period of 7 years, the said amount of unclaimed dividend be transferred to Investor Education and Protection Fund.

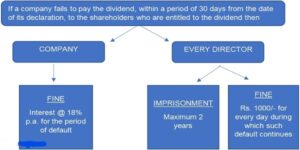

Section 127 : Punishment For Failure To Distribute Dividends

Wrapping up on Dividend

- It is important to note that no dividend shall be paid only in cash; nevertheless, dividends payable in cash may also be paid to the shareholder who is entitled to a dividend by cheque, warrant, or electronic communication.

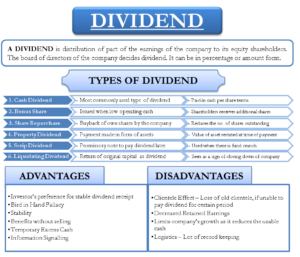

- Interim Dividend is the amount of dividend, being declared by the Board of Directors before the finalisation of Annual accounts.

- this is also considered as debt of the corporate, that after declared it cannot be revoked.

- Board of directors shall analyse the financial position of the corporate before declaring any variety of Interim Dividend and such dividend shall be paid out of surplus in profit and loss account of the corporate.

- Rate of Interim Dividend is mostly lower as compared to the rate of final Dividend.