GSTN has enabled Form DRC-01C on Portal.

Page Contents

Goods and Services Tax Network has enabled Form DRC-01C on Portal.

GSTN has enabled Form DRC-01C to deal with ITC mismatches between GSTR 3B & GSTR 2B, in accordance with rule 88D of the CGST Rules 2017 Through GSTN Notification No. 38/2023-dated on August 4, 2023.

CGST Relevant Rule: Central Goods and Services Tax (CGST) Rules, 2017 – Rule 88D

“Central Goods and Services Tax (CGST) Rules, 2017. Rules 88D. explain the manner of dealing with difference in ITC available in auto-generated statement containing the details of ITC & that availed in GST Return.”

This GSTN system can differentiate Input Tax Credit available as per GSTR-2B/2BQ with Input Tax Credit claimed as per GSTR-3B/3BQ for each Goods and Services Tax return period. If claimed Input Tax Credit exceeds the Input Tax Credit available as per GSTR-2B by specified limits, as extensive guidebook issued by competent GST Authority, GST taxpayer shall receive an intimation in form of GST Form DRC-01C.

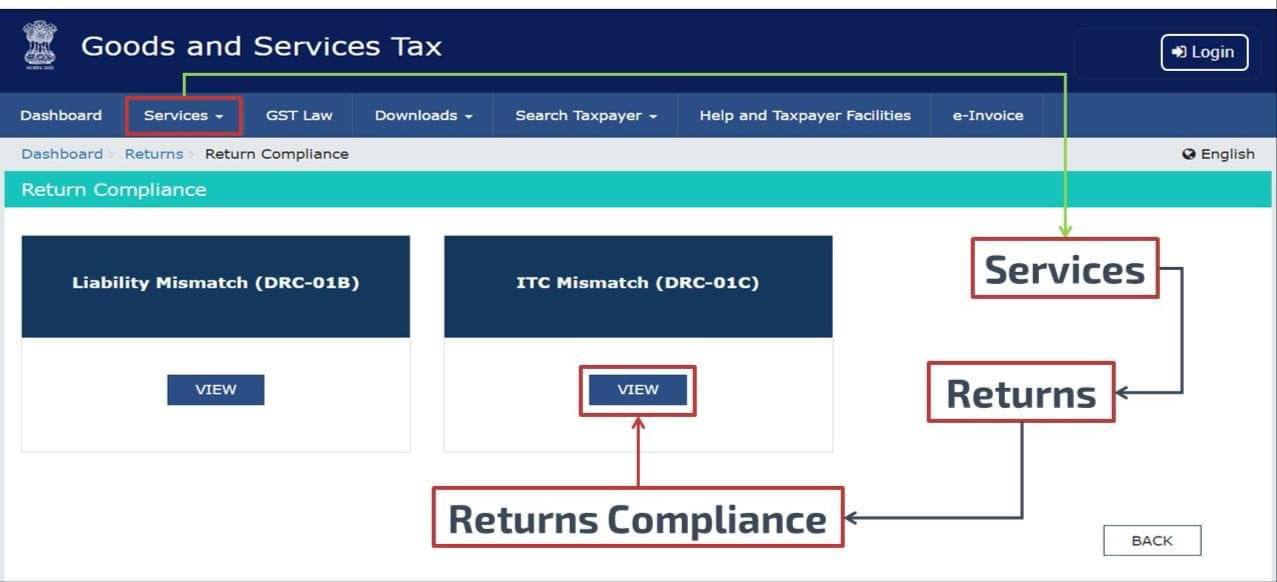

GST taxpayer is needed to submit a response using Form DRC-01C Part B after receiving the notification. The taxpayer has the choice to either use Form DRC-03 to specified payment made to make up the difference, to use one of the alternatives on form to explain difference, or to combine both of these options.

The impacted GST taxpayers will not be allowed to submit their future period GSTR-1/IFF if they fail to respond in Part B of GST Form DRC-01C.

An extensive guidebook with navigational instructions is accessible on the GST portal to aid GST Taxpayers even further in process. It discusses many scenarios relating to the feature and provides step-by-step directions. The below link is mention below: https://tutorial.gst.gov.in/downloads/news/return_compliance_itc_mismatch_intimation_in_form_gst_drc_01c.pdf

Goods and Services Tax Network issued Advisory can be find at: https://www.gst.gov.in/newsandupdates/read/606