GST Registration cancellation: Principle of Natural Justice

Page Contents

Principles of natural justice if no hearing provided to the taxpayer during the Cancellation of GST registration:

IN THE GUJARAT HIGH COURT VIKRAM NATH, CHIEF JUSTICE & J.B. PARDIWALA,

J. Mahadev Trading Company v. UOI

- In the above case of the taxpayer was that without fixing a date for hearing and without waiting for any reply to be filed by the taxpayer, the cancellation order was passed by authority whereby registration of the taxpayer with GST Dept was cancelled.

- Even cancellation order refers to a reply submitted by taxpayer & also about personal hearing, according to the assessee neither he had submitted any reply nor afforded any opportunity of hearing.

- It is held that the Show-cause notice (SCN) was as vague as possible & did not refer to any particular facts, much less point out so as to enable the notice to give his reply. So, cancellation of registration resulting from said show-cause notice also cannot be sustained.

(CGST Circular 148/04/2021- GST)

- Standard Operating Procedure (SOP) for implementing section 30 of the CGST Act, 2017 and rule 23 of the CGST Rules, 2017’s provision of extending the time limit to request for reversal of cancellation of registration.

- At Rajput Jain and Associates, we help our clients in dealing with various of GST matters (GST registration, GST tax return, refund claims & GST audits) by supplying them with sufficient guidance and support from our end.

- If you have any questions or would like to understand more about cancelling your GST registration, Our Below mention Services Include under GST registration cancellation.

Also Read : A requirement of liability under GST Registration

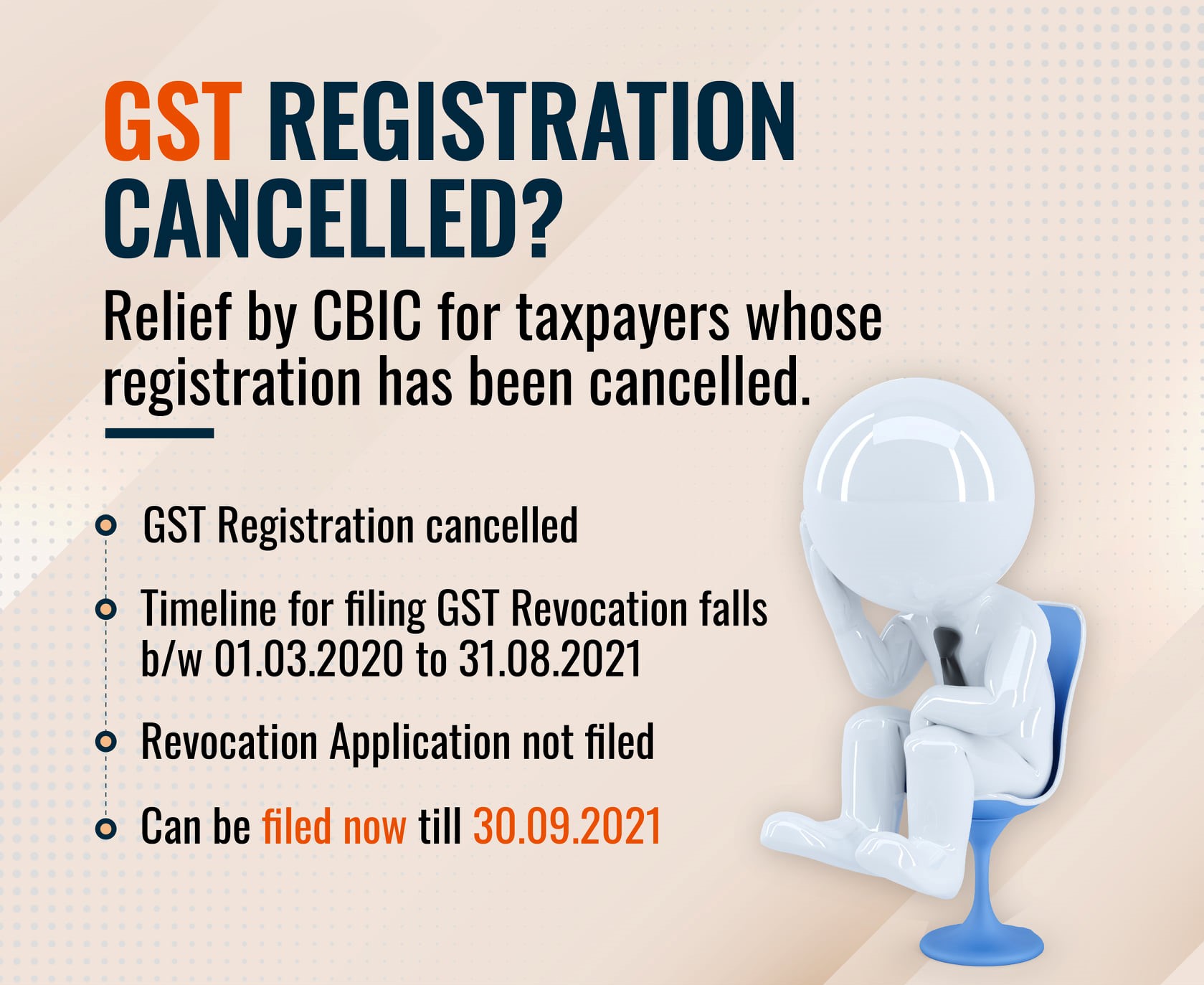

Date for GST filing application for revocation of cancellation of registration extended

- The time limit for filing an application for revocation of cancellation of registration has been extended to 30th September, 2021, as per notification 34/2021 -Central dated 29th August 2021,

- where the due date for filing an application for revocation of cancellation of registration falls between 1st March, 2020 and 31st August, 2021.

- Advantages of this notification is extended to all cases where registration has been cancelled under section 29(2) (B) or (C) of the CGST Act, 2017 and the due period for filing an application for revocation of cancellation of registration is between March 1, 2020 and August 31, 2021.

Reference:

- Any GST Registered person, other than a person specified in clause (b), has not Filling GSTR Returns for a continuous period of six months. : Section 29(2)(c)

- A person paying tax under section 10 has not filling GSTR Returns for three consecutive tax periods : Section 29(2)(b).

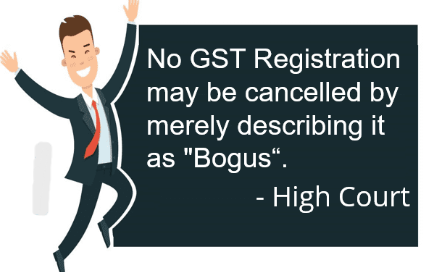

High Court : No GST Registration may not be cancelled by merely describing it as “Bogus”. The word “bogus” has not been used by the law

- GST Registration could be revoked only if one of the 5 statutory conditions of Section 29(2) is fulfilled.

- No registration may be cancelled simply by labelling the firm that received it as “bogus.”

- The term “bogus” is not used in the statute. The only situation to which such term may refer is one described in Clauses (c) and (d) of Section 29(2) of the Act, which is when a registered firm fails to begin operations within six months of its registration.

- Aside from that, the term “bogus” may also relate to a satisfaction envisioned by Section 29(2)(c) of the Act, which states that a registered firm’s registration may be cancelled if it has not furnished its return for a continuous period of 6 months.

It is further stated that the benefit of notice will apply in instances where the application for revocation or cancellation of registration is either pending or has already been rejected by the proper officer. please feel free to contact us on 9555 555 480 or singh@carajput.com

Popular Articles: