Submit ITR for AY 2023-24 on time/face a penalty Fee

Page Contents

Submit ITR for AY 2023-24 on time/face a penalty Fee of Rs 10,000

CBDT made 2-time Penalty for Missing ITR Due Date this Year

Moreover, in the Budget Exemptions to rule due to the amendments made in the Income-tax Act, 1961, which stipulates the below person will not be exempted from the penalty

- Individuals who have deposited an amount or aggregates of the amount exceeding INR 1 cr in one or more banking accounts

- Individuals who have incurred expenditures exceeding INR 2 lakh due to foreign travel.

- who incur made an expenditure of INR 1 lakh & more due to electricity consumption.

Submit the ITR dues also ensure that interest payable on the income tax refund is calculated from April 1 of the relevant AY. In the case of belated filings, the individual loses out on some amount of interest.

“In view of the continued challenges faced by taxpayers in meeting statutory compliances due to outbreak of COVID-19, the government further extends the dates for various compliances,” said the CBDT in a statement.

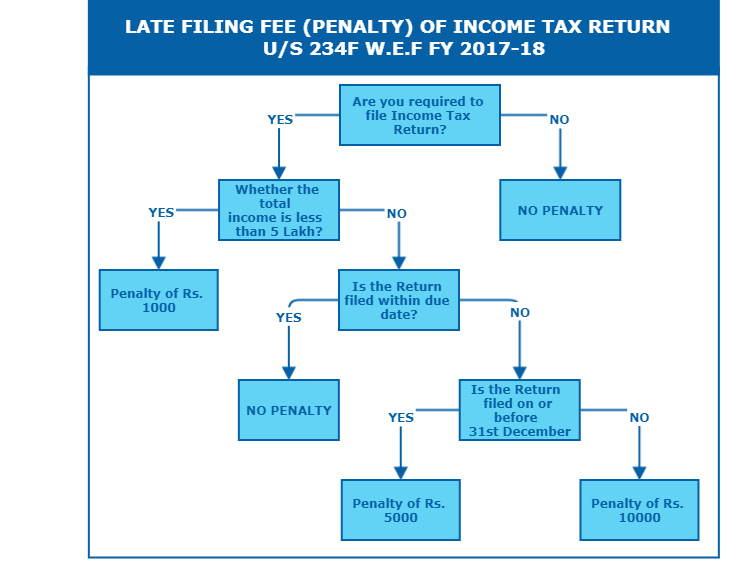

In conclusion, section 234F explain the below summary of penalty Fee appliable :

| Applicable Late Filing Fee Details as per section 234F | ||

| E- Income tac Filing Date | Total income Below INR 5 lakhs | Total income Above INR 5 lakhs |

| Up to 31st August 2020 | Rs 0 | Rs 0 |

| Between 1st September 2020 to 31st December 20 | Rs 1,000 | Rs 5,000 |

| Between 1st January 21 to 31st March 21 | Rs 1,000 | Rs 10,000 |

Applicable kind of income tax form

| ITR 1 (SAHAJ) | Individuals with Salary & interest Income only |

| ITR 2 | Individuals and HUF not having income from business/profession |

| ITR 3 | Individuals/ Hindu Undivided Families being partners in firms & not carrying out business or profession under any proprietorship |

| ITR 4 | Individuals & Hindu Undivided Families having a proprietary business or profession income |

| ITR 4S (SUGAM) | Individuals or Hindu Undivided Families having presumptive business Income |

| ITR-5 | In order for AOP & BOI, LLP, & Partnership firms to report their income and tax computation. |

| ITR-6 | Co that are registered in India use this form. |

| ITR-7 | In case entities are claiming an exemption as colleges, scientific research institutions, political parties or universities, and religious or charitable trusts, this form must be used. |

Difference between ITR1 and ITR2

Normal Due date of Advance Tax under the income tax act

| Installments | Rate of Advance Tax | Total Liability/due under advance Tax |

|---|---|---|

| First Installments | 15 % | 4,80,000*15%= 72,000 |

| Second Installments | 45% | 4,80,000*45%= 2,16,000 |

| Third Installments | 75% | 4,80,000*75%= 3,60,000 |

| Fourth Installments | 100% | 4,80,000*100%= 4,80,000 |

kind of Interest U/s 234 of the income tax act 1961

three kinds of Interest payable u/s 234 as below mention hereunder :

- Interest under section 234A- Delay in Filing of Income Tax Return

- Interest under section 234B- Delay in payment of Advance Tax

The last date for filing income-tax returns

Tax returns for AY2023-24 (The FY 2022-23 ) were original to be filed by July 31.

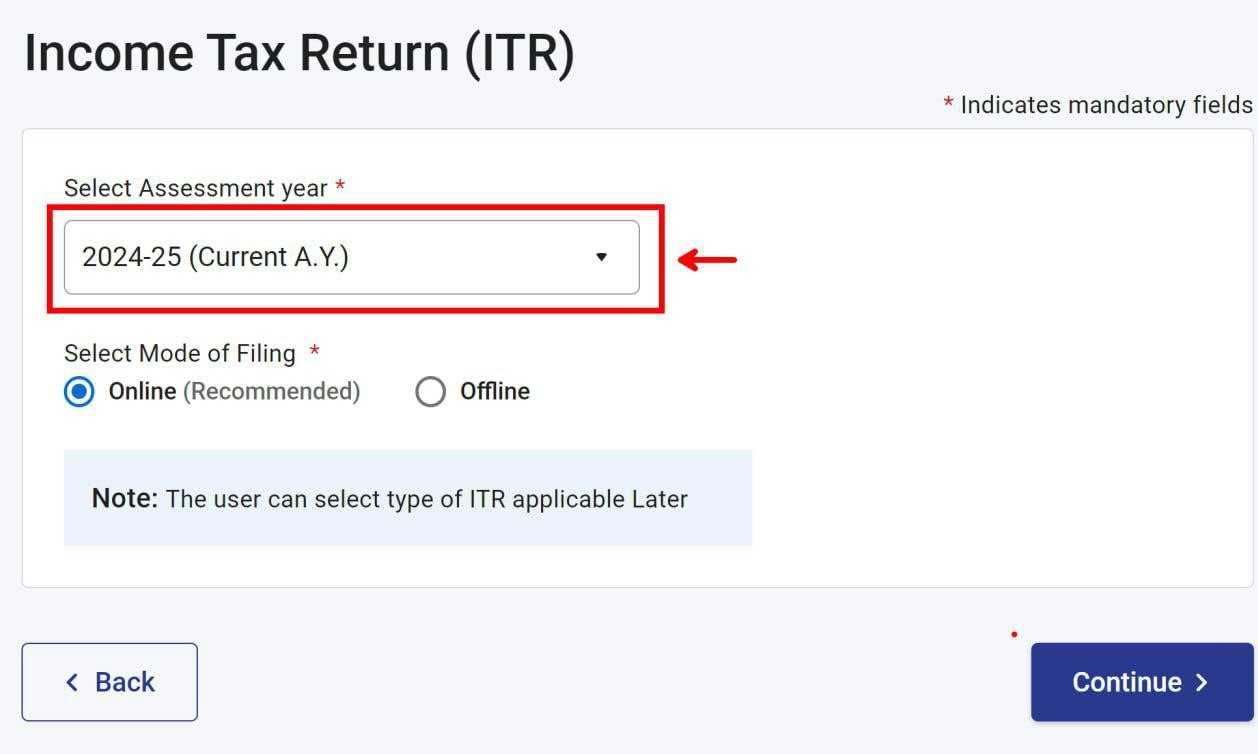

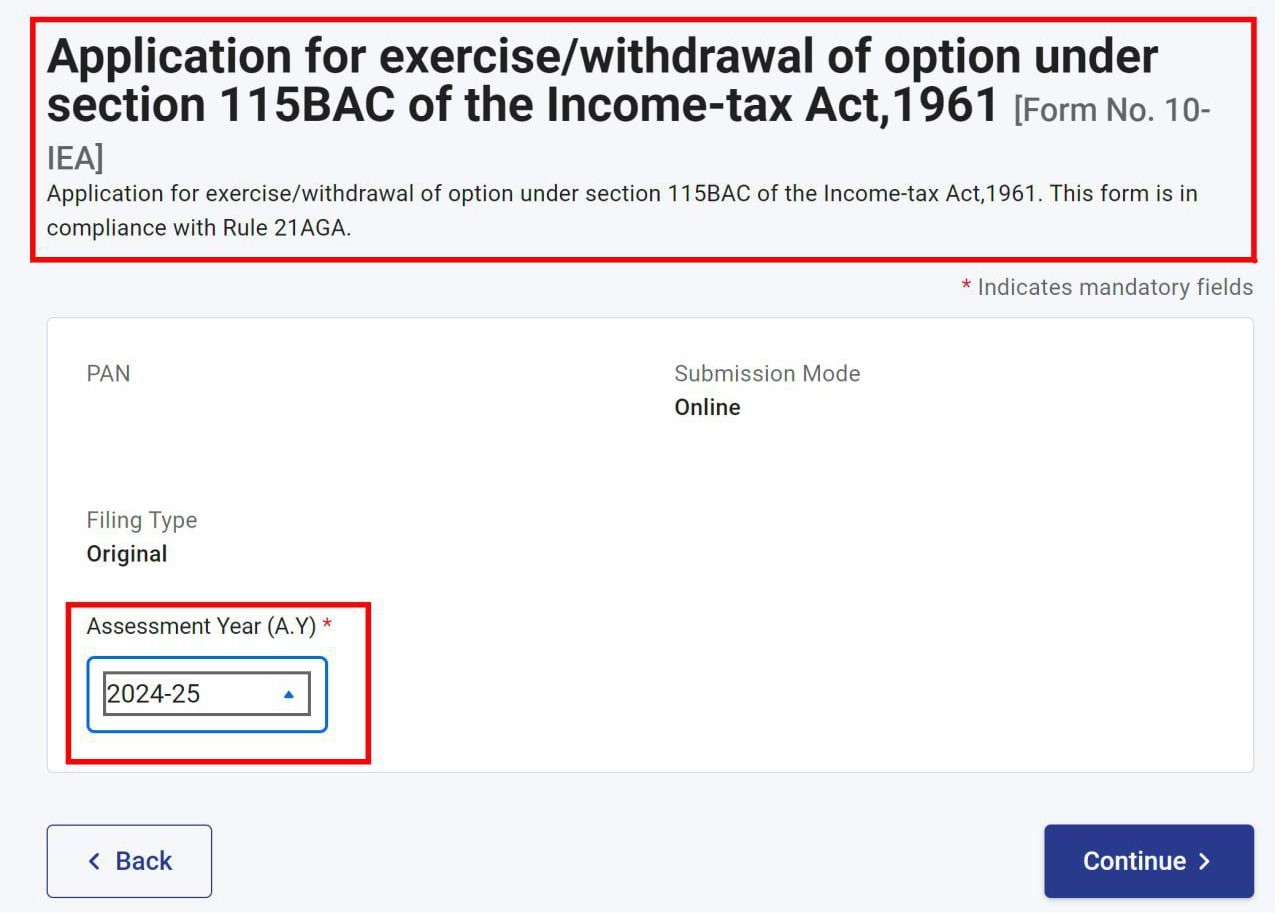

Form 10IEA for AY 2024-25 is now available for filing on income tax portal.

Please Note – All taxpayers opting for old tax regime in AY 2024-25 need to file Form 10IEA before due date of ITR Filing

ITR 1,2 & 4 for AY 2024-25 are now available on income tax portal for filing.