Overview on Disallowance of Expenditure u/s 43B(h)

Page Contents

Overview on Disallowance of Expenditure u/s 43B(h)

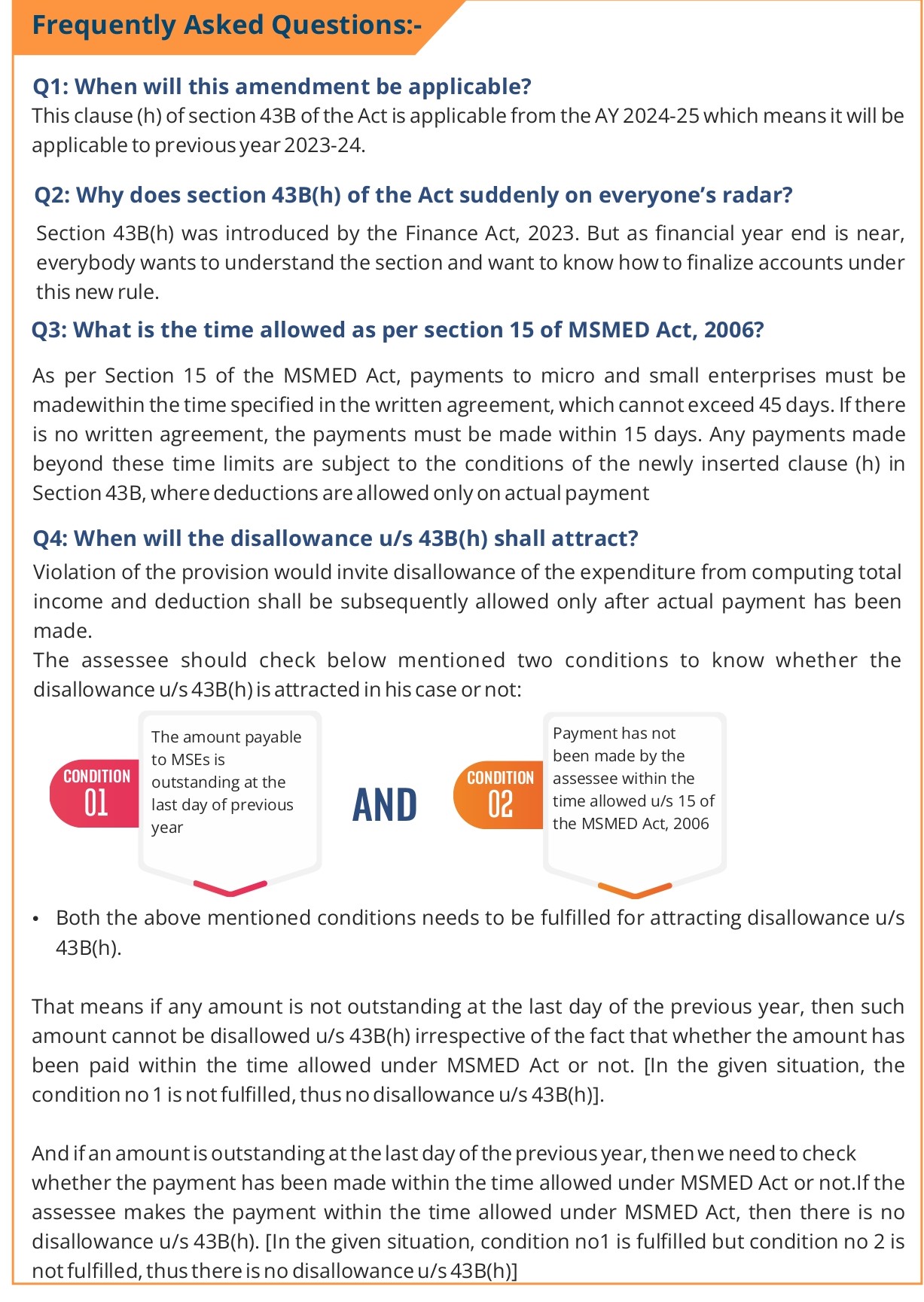

The Union Budget 2023 introduced measures to encourage timely payments to micro or small enterprises by including them in Section 43B of the Income Tax Act, 1961. The Finance Act, 2023, with effect from 1st April 2024, added new clause (h) to section 43B of the Income Tax Act, 1961 which states that the deduction shall be allowed in respect of any sum payable by the Taxpayer to a micro or small enterprises beyond time limit prescribed in section 15 of the MSMED Act, 2006” only in computing total income of previous year in which the sum has been actually paid. Proposed an amendment to Section 43B only to allow the assessee to deduct sums payable to a registered MSME based on actual payment.

Provision of section 43B has a major impact on financial statements and consequent Income tax liability of the Taxpayer. This change will improve working capital management for micro or small enterprises, which are crucial to the Indian economy.

Provision of section 43B is applicability

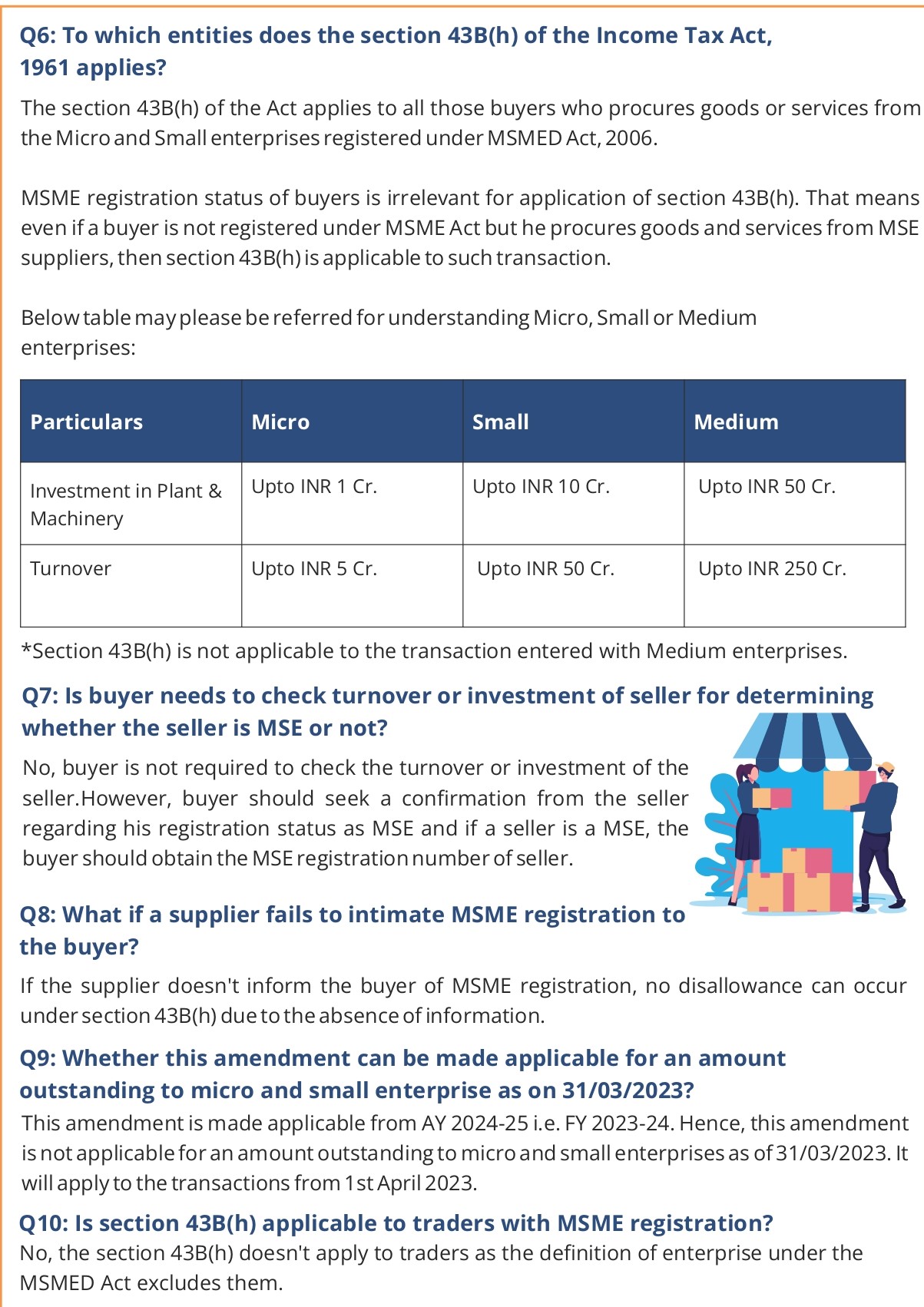

This Provision of section 43B is applicable when an organisation is purchasing goods or taking services from an organisation registered under the MSMED Act, 2006. Notably, the registration of the buyer under the MSMED Act, 2006, is not compulsory. Definition “enterprise” means an industrial undertaking or a business concern or any other establishment, by whatever name called. So an individual carrying out a business without an office may not classify as a MSME. (As per section 2(e) of MSMED Act, 2006). The objective of Section 43B amendment is to encourage timely payments to MSME enterprises & to overcome problem of shortage of working capital in this sector.

Govt of India is considering request to see if there is any scope of amendment to clause Provision of section 43B So that credit cycle of micro or small enterprises is not disturbed & those not aware of amendment get ample time to avoid any probability of liabilities,

Since Provision of section 43B October 2017 introduction, the government micro or small enterprises Samadhaan delayed payment monitoring platform has received 1.76 lakh submissions from micro or small enterprises accusing their purchasers of withholding payments. This included Rs 41,105 crore that was held up for these micro or small enterprises; of them, only 34,551 cases totaling Rs 6,052 crore have been resolved by the nation’s MSE Facilitation Councils as of date.

This blog provides extensive study & understanding of subject matter Provision of section 43B, FAQ & Various interpretations around Provision of section 43B.

Some examples for applicability of Section 43B(h) in different cases

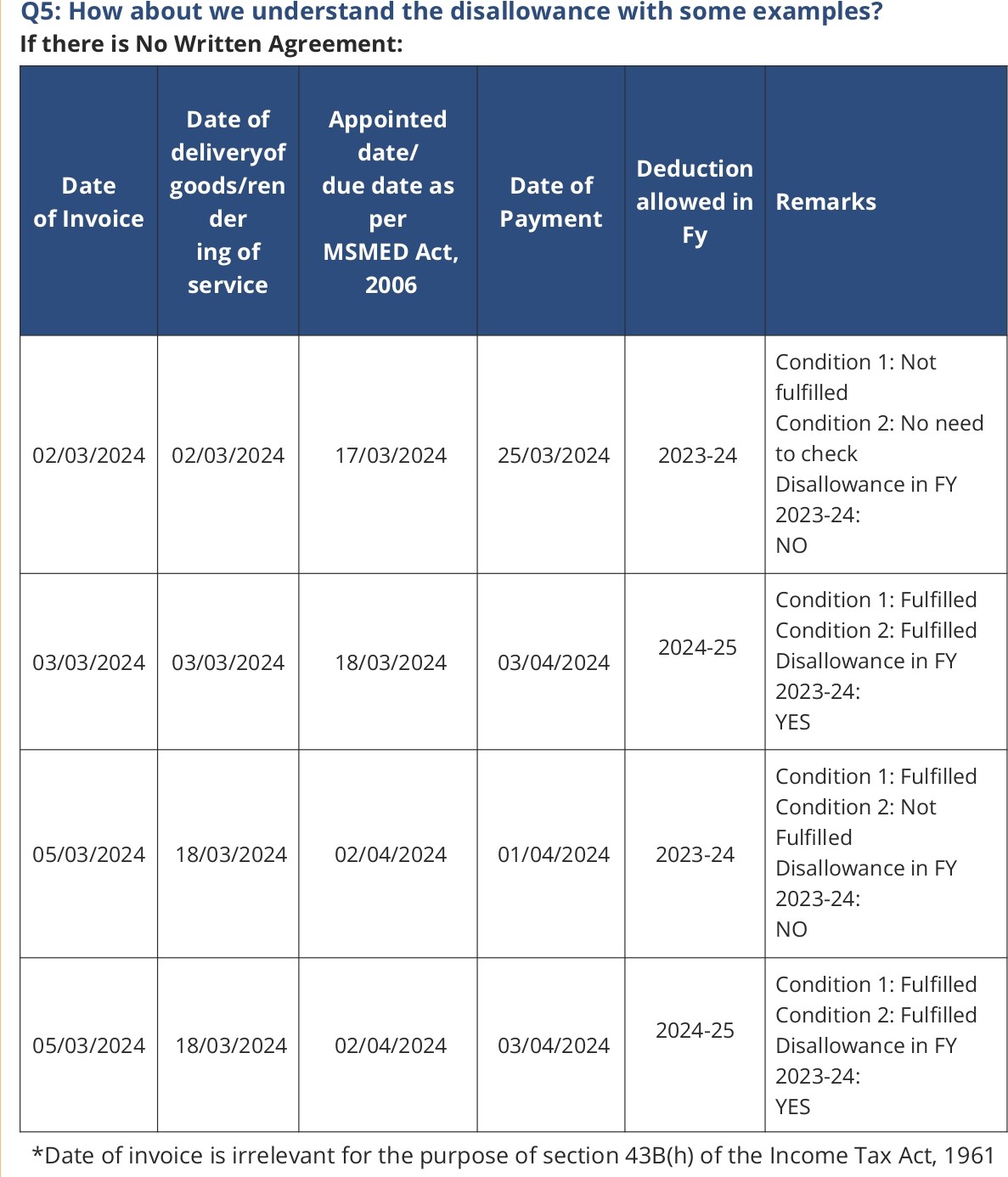

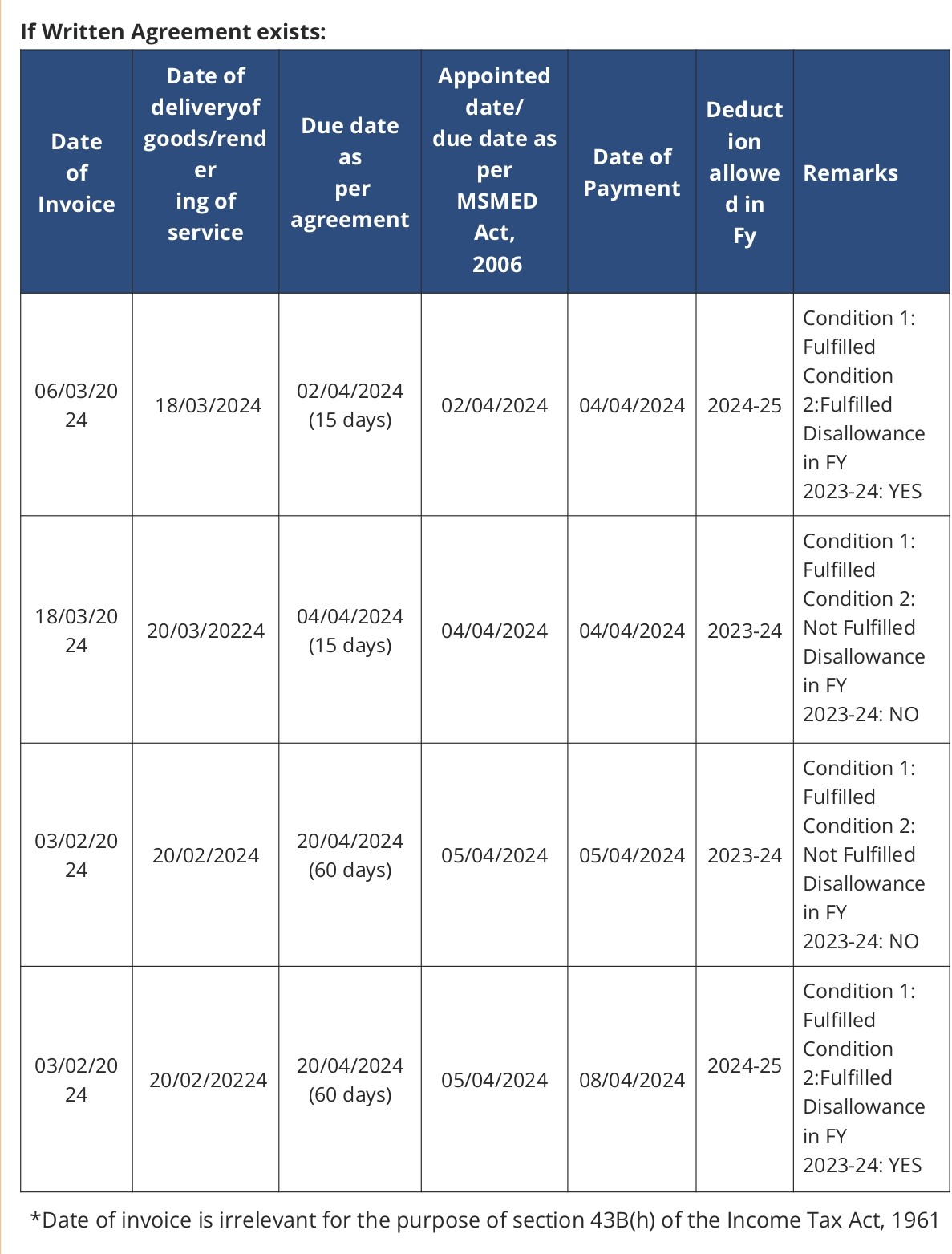

Where there is no agreement in writing