Amendments in ITR Form 6 applicable to companies

Page Contents

Amendments in Income Tax Return Form 6 applicable to companies:

New ITR forms For the AY 2024–2025, I-T return forms 2, 3, and 5 are now available for filing tax returns for the AY 2024–25, according to a recent announcement from the Income Tax Department. Prior notifications were sent out in December 2023 for the ITR-1, which is filed by individuals with a total income of up to Rs 50 lakh, and January 2024 for businesses with an ITR-6. ITR forms for AY 2024-25: Which ITR form needed to choose?

- Income Tax Return forms ITR-6: Companies other than those exempt u/s 11 can submit Income tax return Form-6.

- Tax Return forms ITR-5: Partnership firms and Limited Liability Partnership can submit Income tax return Form-5.

- Income Tax Return forms ITR-4: Sugam is for resident individuals, HUFs, & firms (other than Limited Liability Partnership’s) with a total income of up to INR 50,00,000/- & income from business or profession.

- Tax Return forms ITR-3: Those who do have income from business or profession can submit Income tax return Form 3.

- Income Tax Return forms ITR-2: Individuals & HUFs who do not have income from business or profession [and are not eligible to submit Income tax return Form-1 (Sahaj)] can submit ITR-2

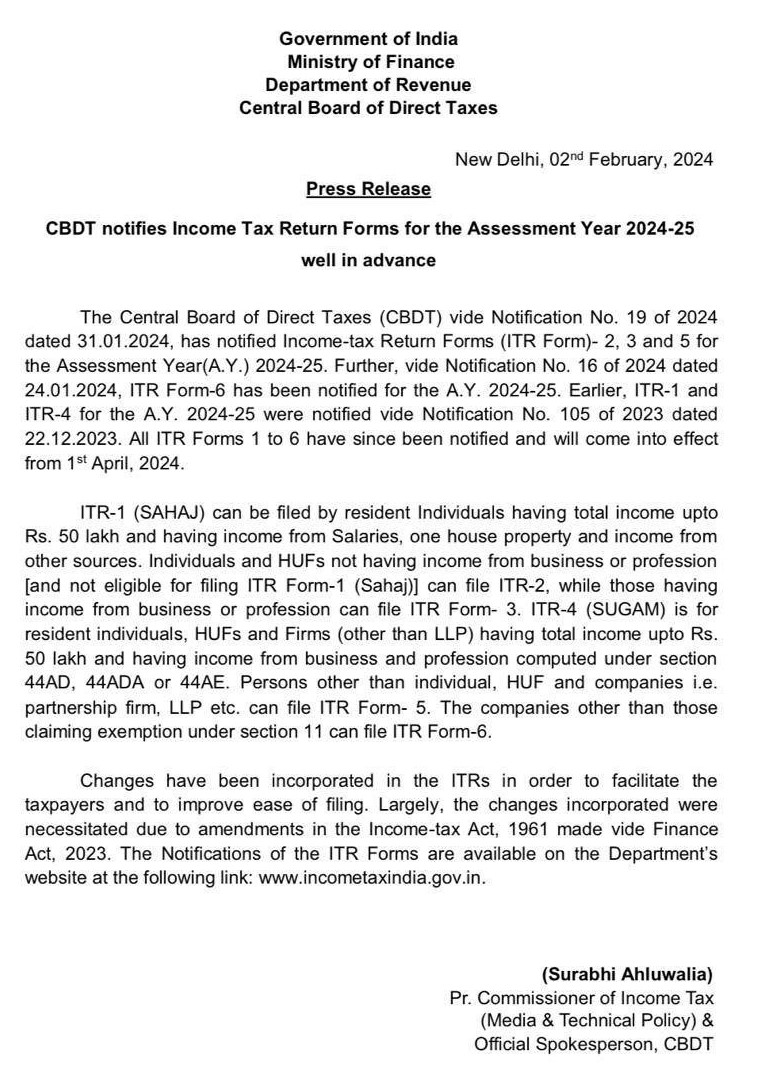

CBDT notifies ITR Forms 1-6 for AY 2024-25,

The CBDT notifies ITR Forms 1-6 for AY 2024-25, well in advance, to facilitate taxpayers & improve ease of filing. Complete Notification are attached here under :

Change in Income Tax Return Form 6

Central Board of Direct Taxes via Notification No. 16/2024, dated 24-01-2024 has notified ITR Form 6 for the AY 2024-25, Amendments in Income Tax Return Form 6 are briefly explained below:

- LEI (Legal Entity Identifier) information & details: Legal Entity Identifier (LEI) disclosure is now compulsory for refunds exceeding INR 50 crores or more in Form ITR 2, 3, 5 and 6 to furnish the Legal Entity Identifier details.

- Business Trust Sums Reporting: According to a new field under Schedule OS that Business Trust Sums Reporting of unitholders receive and that business trust distributes in order to prevent non-taxation can now be reported on Form ITR 2, 3, and 5.

- New Schedule 115TD: Schedule 115TD makes it mandatory for any entity of fund authorized u/s 10(23C) or registered u/s 12AB of income Tax Act to pay additional income tax on the additional income, arising on conversion into a non-charitable form.

- Offshore banking unit or IFSC: Additional disclosures have to be made with regards to Income Tax Return Form 6.

- Contributions towards Political Party: Income tax Schedule 80GGC will need information & detailed disclosure of contributions on political party in Form ITR 2, 3, 5 & 6.

- Electronic Verification Code for Tax Audits: Individuals & Hindu Undivided Family’s under tax audits (ITR 3) can now verify returns using EVC. This simplifies the Electronic Verification Code verification process and enhances ease of compliance.

- ITR Filing Deadlines: Income tax Taxpayers now have a new column in Tax Forms ITR 3, 5 and 6 where they give deadline for ITR filing. Also new provisions allow for the adjustment of unabsorbed depreciation needed to be disclose in Form ITR 3 and 5.

Change in Income Tax Return Form 6- Related to Discloser

- Disclosure of deposits in Capital Gains Accounts scheme (CGAS) Reporting: Schedule-Schedule Capital Gain G has been enhanced to gather more information relating to money deposited in the CGAS (Capital Gains Accounts scheme) is now required in Form ITR 2, 3, 5 and 6.

- Income Tax Disclosure of donation made to political parties (Schedule 80GGC): Additional information beyond the amount eligible for deduction under section 80GGC, such as IFSC Code, transaction number& contribution amount has to be disclosed.

- Disclosure for eligible start-ups deduction details: New Schedules for claiming deductions under Sections 80-IAC & 80LA have been added in Income tax Form ITR 5 & 6. Eligible Start-ups need to furnish details such as Incorporation date, Nature of business, certificate number from Inter Ministerial board of certification, First year of deduction, amount of deduction in financial Year/ Current year, if the said start-up is claiming deductions undersection 80-IAC.

- The Discloser in Dividend Income Reporting: Income tax Taxpayer dividend income received from a unit in an International Financial Service Centre shall be taxed at a decreed tax rate of 10 percent instead of 20 percent. Schedule OS has been changed in new Income tax return forms to incorporate such change in Income tax return Form ITR 2, 3, 5 and 6

- Reason for Tax Audit U/s 44AB: Business Entities are required to provide reasons for tax audit u/s44AB in Income Tax Return Form 6

- Disclosure Online games winnings Taxation: Changes has been made to Schedule OS for disclosure of income by way of winning from online games in form ITR 2, 3, 5 and 6 which is charged u/s 115BBJ.

- Reasons for Tax Audit: Additional details are required from audited companies in Form ITR 3, 5 and 6 regarding the circumstances necessitating tax audits. This change enhances transparency and accountability in tax reporting.

Other Change in ITR Form 6

- Ministry of Micro, Small and Medium Enterprises disallowance: A new column has been added Income Tax Return Form 6 with Part A-OI (Other Information) to disclose the amount due to Micro or small enterprises above the prescribe time limit per the Micro, Small and Medium Enterprises Development Act, 2006.

- Timeline date of filing Income tax return: The taxpayer has to choose the applicable Timeline date for filing the Income tax return from the dropdown options provided.

- Discloser of Cash Receipts Reporting: A new column for additional discloser of cash receipts reporting has been added to claim an enhanced turnover limit in income tax Form ITR 3, 4 and 5.

- Unique Document Identification Number: Companies are now mandated to file the acknowledgement number of the Chartered Accountants audit report & the Unique Document Identification Number (UDIN).

- Ministry of Micro, Small and Medium Enterprises registration number: The registration number allotted Micro, Small and Medium Enterprises Development Act, 2006 has to be disclosed by the entity.

- Taxpayer Bank A/c Disclosure: Taxpayers must now disclose all bank a/c held, except dormant Bank A/c in Income Tax Form ITR 2, 3 and 5.

- New Schedule 80U: Schedule 80U is additional for claiming deductions for persons with disabilities under section 80U, seeking detailed in Income tax Form ITR 3.

- Deduction under Section 80CCH: A new column is added to claim deductions u/s 80CCH for Agniveer Corpus Fund in Income Tax Form ITR 1, 2, 3 and 4.

- Schedule 80DD: Like Schedule 80U, additionally information needed in New Income Tax Schedule 80DD is added to claim deductions for maintenance & medical treatment of taxpayer dependents with disabilities in income tax Form ITR 2 and 3.

Taxation of Companies

All the Required Documents for Filing ITR

Popular Article :

- All about the Income taxation on capital gain

- Provision-of-capital-gains-charts

- All about the Income taxation on capital gain

- Deduction u/s 80CCD of Income Tax Act, 1961

- All about the Income taxation on capital gain

- Aware of the penalty of Section-234f for late filing of ITR

- Which is Better- Old vs New Tax Regime Comparison 2024 ?

Our Services:

- Tax Returns: Individual Tax Returns, Company Tax Returns

- Consultancy: Comprehensive Compliance Consultancy

Contact Us: For query or help, contact: singh@carajput.com or call at 9555555480