Company Taxation in India

Page Contents

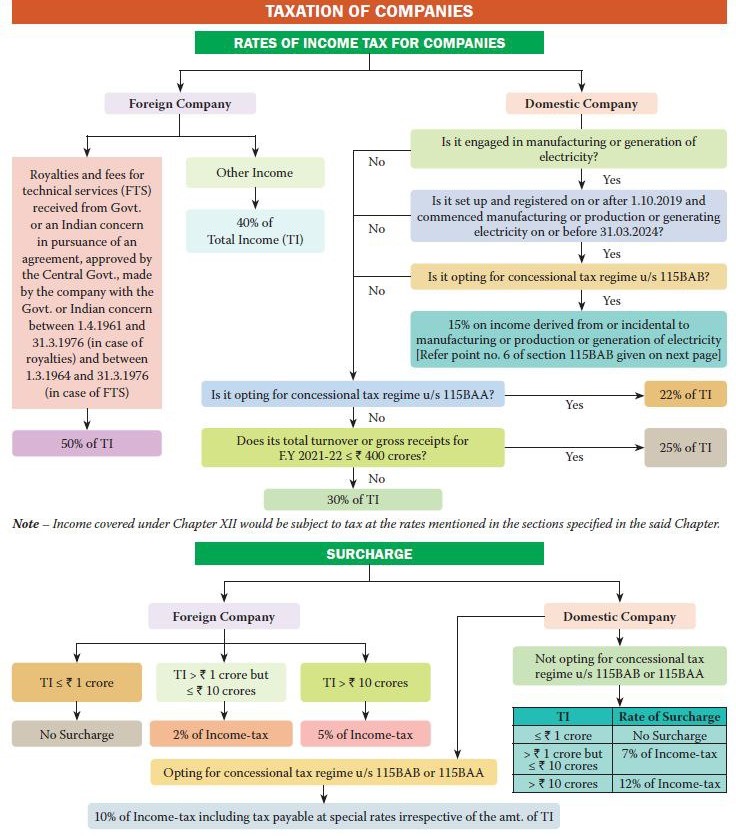

INCOME TAX ACT – Company Taxation in India

ALTERNATE MINIMUM TAX (AMT) [CHAPTER XII-BA–SECTIONS 115JC TO 115JF]

![ALTERNATE MINIMUM TAX (AMT) [CHAPTER XII-BA–SECTIONS 115JC TO 115JF]](https://carajput.com/blog/wp-content/uploads/2015/12/ALTERNATE-MINIMUM-TAX.jpg)

SET OFF OF CREDIT OF MAT PAID UNDER SECTION 115JB [SECTION 115JAA]

![SET OFF OF CREDIT OF MAT PAID UNDER SECTION 115JB [SECTION 115JAA]](https://carajput.com/blog/wp-content/uploads/2015/12/SET-OFF-OF-CREDIT-OF-MAT-PAID-UNDER-SECTION-115JB.jpg)

MINIMUM ALTERNATE TAX ON COMPANIES [SECTION 115JB]

![MINIMUM ALTERNATE TAX ON COMPANIES [SECTION 115JB]](https://carajput.com/blog/wp-content/uploads/2015/12/MINIMUM-ALTERNATE-TAX-ON-COMPANIES-SECTION-115JB.jpg)

![MINIMUM ALTERNATE TAX ON COMPANIES [SECTION 115JB] -](https://carajput.com/blog/wp-content/uploads/2015/12/MINIMUM-ALTERNATE-TAX-ON-COMPANIES-SECTION-115JB-.jpg)

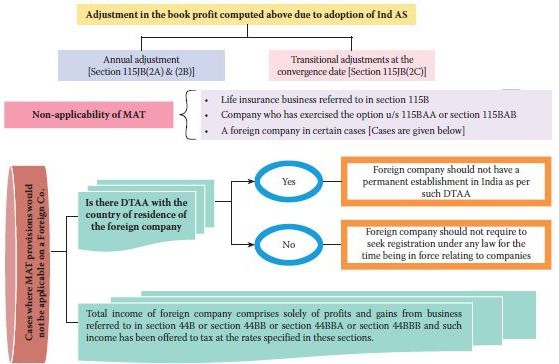

COMPUTATION OF BOOK PROFIT FOR IND-AS COMPLIANT COMPANIES

DIRECT TAX LAWS

Section 119 of the Income-tax Act, 1961 – Income-tax Authorities – Instructions to Subordinate Authorities – Facilitating Taxpayers’ Electronic Interface with the Department

Under Section 115JB of the Income-tax Act, 1961 – Minimum Alternate Tax (MAT) – Applicability of MAT on Foreign Companies for period prior To 1-4-2015 5

SECTION 9

INCOME – DEEMED TO ACCRUE OR ARISE IN INDIA

Business income : In absence of any material on record as to whether non-resident agents appointed by assessee rendered services abroad and they had no business connection in India, question regarding assessee’s obligation of deduction of tax at source on payment of sales commission to them was to be disposed afresh –[2015] 64 253 (Chennai – Trib.)

SECTION 10(23C)

EDUCATIONAL INSTITUTIONS

Sub-clause (iiiab) : Where assessee-society running educational institutions filed its return claiming exemption under section 10(23C)(iiiab) in view of fact that Government was substantially financing and interested in management of assessee, its claim for exemption was to be allowed – [2015] 64 312 (Punjab & Haryana)

SECTION 68

CASH CREDITS

In terms of section 68, assessee is liable to disclose only source(s) from where he has himself received credit and it is not burden of assessee to show source(s) of his creditor nor is it burden of assessee to prove creditworthiness of source(s) of said sub-creditors – [2015] 64 329 (Delhi)

Donations : Where assessee claiming himself to be a Sewadar of Historic Dera, deposited donations received in name of Dera in his own bank account and, moreover, he failed to prove that any charitable activity in terms of section 2(15) was ever carried out by him, authorities below were justified in making addition to his income under section 68 in respect of donations in question – [2015] 64 311 (Punjab & Haryana)

SECTION 92C

TRANSFER PRICING – COMPUTATION OF ARM’S LENGTH PRICE

Bright line test (BLT) is not a valid method for either determining the existence of international transaction or for the determination of ALP of such transaction – [2015] 64 328 (Delhi)

Comparables and adjustments/Adjustments-Interest : ALP of an international loan transaction, which was designated in hard currency, is to be ascertained, interest rate on rupee transactions in India is not relevant –[2015] 64 251 (Bangalore – Trib.)

Comparables-and adjustments/Adjustments-Interest : In case of interest on outstanding interest from loan transactions, that was designated in hard currency, rate of interest and terms applicable in materially similar situation of delay in payment of interest to Exim Bank would apply mutatis mutandis for determining ALP –[2015] 64 251 (Bangalore – Trib.)

SECTION 92CA

TRANSFER PRICING – REFERENCE TO TPO

Where value of international transactions entered into between assessee and its AE exceeded Rs. 5 crores, Assessing Officer was required to refer matter to TPO for determining ALP – [2015] 64 252 (Madras)

SECTION 151

INCOME ESCAPING ASSESSMENT – SANCTION FOR ISSUE OF NOTICE

Recording of satisfaction : SLP dismissed against High Court’s ruling that where Joint Commissioner recorded satisfaction in mechanical manner and without application of mind to accord sanction for issuing notice under section 148, reopening of assessment was invalid – [2015] 64 313 (SC)

SECTION 153C

SEARCH AND SEIZURE – ASSESSMENT OF INCOME OF ANY OTHER PERSON

Applicability of : Even in cases where Assessing Officer of person searched and assessee who is sought to be assessed under section 153C is same, still Assessing Officer is required to record his satisfaction that assets/documents seized belong to a person (assessee) other than searched person – [2015] 64 309 (Delhi)

SECTION 269UC

PURCHASE OF IMMOVABLE PROPERTY BY CENTRAL GOVERNMENT – RESTRICTIONS ON TRANSFER OF PROPERTY

Where immunity certificate issued by department under KVSS to vendor covered impugned transaction of sale of property, non-filing of form 37-I by vendor would not entitle department to launch prosecution under sections 269UC and 276AB against her – [2015] 64 254 (Madras)

SECTION 271(1)(c)

PENALTY – FOR CONCEALMENT OF INCOME

Recording of satisfaction : Before levying penalty under section 271(1)(c), it is incumbent upon Assessing Officer to state whether penalty was being levied for concealment of income or for furnishing of inaccurate particulars of income – [2015] 64 155 (Kolkata – Trib.)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances; Hope the information will assist you in your Professional endeavors. For query or help, contact: singh@carajput.com or call at 9555555480

Read our articles: