CBDT Notified Rule 11UD Prescribing thresholds for SEP

Page Contents

CBDT notifies Rule 11UD prescribing thresholds for determining ‘Significant Economic Presence’ in India

- CBDT has set revenue & user base threshold limits for determining ‘Significant Economic Presence’ in Notification No. 41 dated May 2021.

- Legislators have established circumstances in which foreign corporations are regarded to have a “business tie” in India, bringing their operations in India under the jurisdiction of our tax system.

- Indian legislators have devised scenarios in which such foreign corporations are deemed to have a “business link” in India, bringing their Indian operations under the Indian tax system’s jurisdiction.

- The Indian income tax legislation was revised in 2018 by the Finance Act, which expanded the meaning of the existing word ‘business connection’ to include Significant Economic Presence (SEP).

What is Significant Economic Presence (SEP)?

Significant Economic Presence (SEP) was defined to mean, inter-alia transaction of services and goods with any person in India which including provision of download of data or software in India, if one of two conditions are satisfied:

-

- Engagement with Indian consumers cross a specified No. or

- Total Aggregate of payments arising from such transactions crosss a specified limit

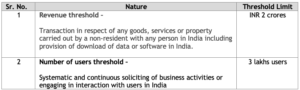

What is Significant Economic Presence (SEP) threshold limit specified by CBDT ?

India economy went ahead & specified the threshold limits with effective date April 1, 2021 to operationalise the Significant Economic Presence (SEP) for Non-Resident E-commerce companies by including activity of ‘software/ download of data’

-

- Amount of revenues exceeding INR 2 Cr from Indians or

- a threshold of INR 3,00,000/- No of Indian users

- with whom such companies continuous business activities and ‘solicit systematic or engage in interaction’ with them

Threshold limit CBDT notified for specific object of Significant Economic Presence (SEP) has been summaries as below:

The Basic outline of Rule 11UD is addressed in this Tax Update including its potential impact.

More read:Three-tier TP Documentation & threshold Requirement

More read :TP : LIBOR IS THE BEST BENCHMARK FOR INTEREST-FREE LOAN GRANTED TO AE

For query or help, contact: singh@carajput.com or call at 9555555480