All about new Rule 86A of the CGST Rules

Page Contents

About the New Rule 86A of the CGST Rules

Rule 86A of the CGST Rules was introduced to block fraudulently availed Input tax credit. As per this Rule, any officer authorised or a commissioner by himself can block the Input tax credit available in the electronic credit ledger of the taxpayer if they has ‘reasons to believe’ that the Assessee has fraudulently availed Input tax credit (by the Govt vide Notification no. 75/2019 dated 26.12.2019)

Here are some situations where Rule 86A of the CGST Rules can be invoked –

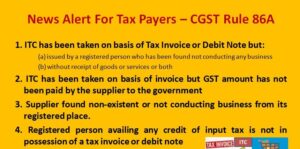

- Tax invoice has been issued by a GST registered person who is found to be non-existent.

- Input tax credit is availed on an invoice on which tax has not been paid to the Govt.

GST Registered person does not have the invoice or debit note basis which he is claiming Input tax credit.

Rule 86A of the CGST Rules itself has been a matter of great concern amongst assessees, who are worried about its over-reach.

- Read also : All about the Input tax credit

Rule 86A of CGST Rules- Blockage of ITC

- In the case of a non-existent supplier, the input tax credit is blocked. Surprisingly, a provision for blocking input tax credits was included in the payment chapter. It is found in Chapter IX of the CGST regulations. It gives officers the authority to halt the input tax credit.

- It is a severe hardship for assessees during the CVID lockout. Lot of firms are either run from home or closed. The non-existent conditions required to be updated to reflect the current circumstances. The virus could spread if the GST dept comes to visit.

What must you know about Rule 86A of CGST Rules?

- Input tax credit blocking via Rule 86A of the CGST Rules is valid up to 1 Year from the date of such blocking. However, notice or any proceedings can be initiated against the assessee in the meantime.

- If a notice is issued, the Input tax credit earlier blocked must be unblocked as a legal action will take over the issue. But, if notice was not issued during that 1 year, the Input tax credit must be unconditionally unblocked.

When will the GST blocking of Input Tax Credits cease?

- Blocking of Input Tax credit under GST cease restriction will cease only after the expiry of 1 year from the date of introduction of such restrictions under the GST Rule.

Ripe for Constitutional Challenge- Rule 86A of the CGST Rules

- According to a review of rule 86A of the CGST Rules subject to a bona fide assessee to undue hardship by freezing their electronic credit ledger, where Input Tax Credit was legitimately claimed, due to the default of their supplier,

- Furthermore, section 16 does not specify a procedure to be followed in such circumstances of credit denial. Given the fundamental constitutional issues outlined above,

- There are sufficient reasons for a jurisdictional high court to examine an order was issued under Rule 86A of the CGST Rules.

Tell me what happened

- A CA named Mr. Madhur Agarwal from Madya Pradesh, filed an Right to Information Act, 2005 application under RTI seeking details of Input tax credit blocked under Rule 86A of Central Goods and Services Tax (CGST) Rules 2017

- The first query was on the state-wise break-up & the 2nd query was on the total Input tax credit blocked under the Central Goods and Services Tax (CGST) Rules, 2017 Rule 86A as of 31st July 2021.

- These were responded to as below:

- UP recorded the highest value of Input tax credit blocked at INR 5,82,000/- Cr.

- Delhi had highest No of taxpayers with Input tax credit blocked under Rule 86A – a total of 13,539 taxpayers.

- Input tax credit blocked for all the Indian states cumulatively came up to INR 6,14,000/- Cr.

When the this backtrack on Input tax credit blocked under Rule 86A happened

- These figures, especially the INR 6,14,000/- crore were refuted, and it was told that the figure included Input tax credit blocked due to errors in data entries by taxpayers.

- It was said that the actual Input tax credit blocked was in fact INR 14,000 crore for 66,000 assessees. Seems the RTI reply overstated Input tax credit blocked by INR 6,00,000/- crores.

BOMBAY HIGH COURT – Rulings on Rule 86A

Blocking of Electronic Credit Ledger under GST – Judgement on Rule 86A

In the matter of ADVENT INDIA PE ADVISORS PRIVATE LIMITED Vs THE UNION OF INDIA AND ORS (WP)

- Throughout this case, the GST Officer unblocked the electronic credit ledger regardless of the fact that it had been blocked for one year since the petitioner had not presented a reconciliation statement between GSTR-2A and the ITC claimed.

Electronic credit ledger was ordered to be unblocked by the BOMBAY HIGH COURT on the reasons listed below:

- Strangely, the instructions do not refer to rule 86A(3). Respondent number 2 appears to be unaware of such a provision. The petitioner is entitled to assert that ITC should have been unblocked promptly after one year of the restriction being imposed, depending on the statutory mandate in Rule 86A(3).

- If the respondents were of the conclusion that petitioner was not cooperating with the department, they should have taken legal action against it.

- But, claiming that a response is pending and that the restriction has not been lifted as a consequence is clearly illegal.

Popular Articles :

Key takeaways about TDS under GST

Complete Guidance on TDS applicable on Goods and Services Tax