CBDT Clarify on Non-Deductibility of Settlement Exp. u/s 37

Page Contents

Non-Deductibility of Settlement Expenses u/s 37 of the Income-tax Act, 1961 : CBDT

Introduction

Section 37 of the Income-tax Act, 1961, allows deduction of business or professional expenses incurred wholly and exclusively for business purposes. However, Explanation 1 disallows deduction for expenditures incurred for any purpose that is an offense or prohibited by law. Section 37 of the Income-tax Act, 1961—Allows deduction for business or professional expenses incurred wholly and exclusively for business purposes. Conditions to Claim Deduction u/s 37 (General Rules). Expenditure must

- Be business-related (not personal or capital)

- Exp Be legal and not for prohibited acts

- Be incurred in the previous financial year

- Exp be wholly and exclusively for business/profession

Excludes:

- Capital or personal expenditures

- CSR expenses (as per Explanation 2)

- Expenses for offences or prohibited activities (Explanation 1)

- Now extended to include settlement-related expenditures (Explanation 3, amended)

Section 135 – Companies Act, 2013 (Applicability of CSR)

-

Applicable to companies (including holding/subsidiary and foreign companies with Indian branches) having:

-

Net Worth ≥ INR 500 crore, or

-

Turnover ≥ INR 1000 crore, or

-

Net Profit ≥ INR 5 crore

during the immediately preceding financial year.

-

-

Mandate: Spend at least 2% of average net profits (as per Section 198) of the 3 immediately preceding financial years on CSR activities.

-

The CSR Expenditure is not deductible under Section 37(1) since it is mandated by law and is considered an application of income, not an expenditure incurred wholly and exclusively for business.

-

CSR contributions made to specific notified funds (like Swachh Bharat Kosh or Clean Ganga Fund) can be claimed under Section 80G, provided all prescribed conditions are fulfilled.

The CSR Expenditure—Section 37 vs. Section 80G

| Aspect | Section 37(1) | Section 80G |

|---|---|---|

| Classification under Income Tax | Falls under PGBP as per Section 14. | Part of Chapter VI-A deductions, applicable after computing Gross Total Income (GTI). |

| Nature of Deduction | Allows deduction for expenses “wholly and exclusively” incurred for business purposes. | Provides specific deductions for donations to specified funds, charitable institutions, etc., not necessarily linked to business activities. |

| Treatment of CSR Expenditure | Explanation 2 to Section 37(1) (inserted via Finance Act 2014) disallows CSR expenditure as it is not deemed incurred for business. | Allowed only if contribution is made to specific notified funds like: Section 80G(2)(iiihk) – Swachh Bharat Kosh Section 80G(2)(iiihl) – Clean Ganga Fund Subject to fulfilment of prescribed conditions. |

| Timing and Manner of Claim | Cannot be claimed even if mandatory under Companies Act, 2013. | Can be claimed while filing return, if donation is to eligible fund, and supported by valid receipt and registration of donee. |

Budget Amendment—Finance Bill 2024- No Deduction u/s 37 for Settlement Amounts Paid for Legal Violations

The Finance (No. 2) Act, 2024 amended Explanation 3 to Section 37(1) to expand the scope of non-deductibility. Now, expenses incurred to settle proceedings for contraventions under certain notified laws are also non-deductible. The amendment is effective from 1st April 2025, and is applicable from Assessment Year 2025-26 onwards. CBDT issues FAQs on Notification No. 38/2025.

CBDT has clarified via Notification No. 38/2025 dated 23.04.2025 & issued FAQs:

Section 37 of the Income-tax Act, 1961 : Section 37 allows deduction of expenses incurred wholly and exclusively for business or professional purposes, provided they are not of a capital or personal nature or covered u/s 30 to 36.

Explanation 1 states it is linked to Explanation 3 by the Finance (No. 2) Act, 2024

- The Explanation 1 disallows any expense incurred for an offense or for purposes prohibited by law. It disallows deduction of any expenditure incurred for:

-

- Any offence, or

- In case of any activity prohibited by law, even if incurred during the course of business or profession.

- Explanation 3, introduced later, clarifies that such disallowed expenses include not only penalties or fines but also any expenditure incurred to settle proceedings initiated for such offenses. It clarified that “expenditure incurred in settlement of proceedings” for contraventions of law—notified by the Central Government—will also be disallowed.

- The amendment broadened Explanation 3 to include settlement expenses related to contraventions of any law notified by the Central Government. Such expenses are now considered as being incurred for a prohibited purpose.

Implications of CBDT FAQs on Notification No. 38/2025

- Any settlement expenditure related to contraventions/defaults under the above laws is non-deductible under the Income Tax Act. So any expenditure incurred to settle proceedings related to contraventions under the above laws cannot be claimed as a deduction or allowance under the Income-tax Act. This includes consent orders, settlement amounts, and penalty settlements. Settlement amounts paid to regulatory bodies like SEBI or CCI will not be eligible for deduction under Section 37. And applicable from AY 2025–26. Form 3CD of the Tax Audit Report has been amended via Notification No. 23/2025 to include disclosures of such expenses.

- This will affect companies involved in regulatory settlements with SEBI, CCI, or similar bodies. As per CBDT Notification No. 38/2025, the following laws have been notified:

- Securities and Exchange Board of India Act, 1992

- Securities Contracts (Regulation) Act, 1956

- Depositories Act, 1996

- Competition Act, 2002

- Any compliance changes: Tax Audit Report Form 3CD has been amended via Notification No. 23/2025 dated 28.03.2025 to mandate disclosure of such expenses. Income Tax Form No. 3CD has been amended via CBDT Notification No. 23/2025 (dated 28.03.2025) to require disclosure of such expenses during tax audits.

Action Points:

- Review all legal settlements and verify their nature.

- Update accounting policies and tax planning documentation.

- Disclose appropriately in tax audit reports and notes to accounts.

- Educate clients and teams on the implications of the amended Explanation 3.

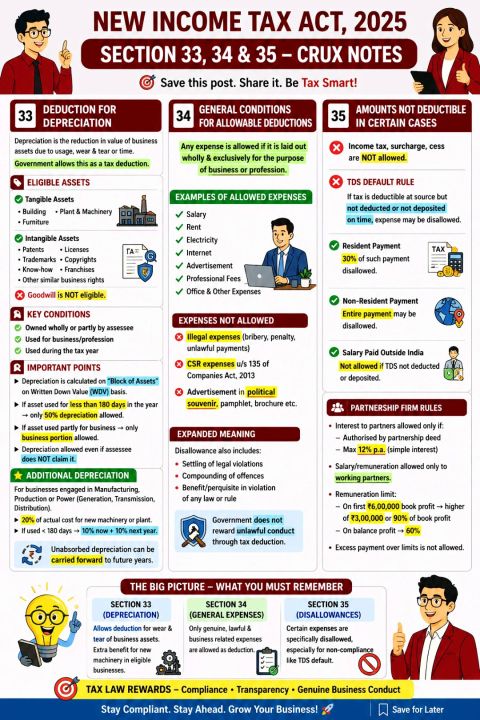

Complete Crux Under Section 33, 34 & 35 in Simple Language – NEW INCOME TAX ACT, 2025

SECTION 33 – DEPRECIATION DEDUCTION

- Depreciation means reduction in value of business assets due to usage, time or wear & tear. Government allows this reduction as a tax deduction.

- Eligible Assets: Building, Plant & Machinery, Furniture, Patents, Trademark, License, Copyright etc.

- Goodwill is NOT eligible.Conditions:

- Asset must be owned wholly/partly by assessee, Used for business/profession, Used during tax year

Important Points

Depreciation calculated on “Block of Assets” (WDV basis)

• If asset used for less than 180 days → only 50% depreciation allowed

• Personal use portion not allowed

• Depreciation allowed even if assessee does not claim itAdditional Depreciation: Manufacturing & power sector businesses can claim:

- 20% extra depreciation on new machinery/plant,

- If used <180 days → 10% now + 10% next year

- Unabsorbed depreciation can be carried forward.

SECTION 34 – GENERAL BUSINESS EXPENSE RULE

Basic Principle:

- Any expense is allowed only when it is wholly & exclusively for business, a genuine business expense, and not personal or capital in nature. Examples: Salary, Rent, Electricity, Professional fees and Advertisement.

- Expenses NOT Allowed : Expenses NOT Allowed, like if Illegal payments/bribes, penalties for law violations, and CSR expenses u/s 135 of Companies Act and Political advertisement expense

Main Principle: “Only lawful and genuine business expenses are deductible.”

SECTION 35 – EXPENSES DISALLOWED IN CERTAIN CASES

DISALLOWANCE PROVISIONS

- Income tax, surcharge & cess are NOT allowed as deductions.

- TDS Default Rule: If TDS is applicable but not deducted, or not deposited on time then expense may be disallowed. If Resident payment: 30% disallowance.

- In case of non-resident payment: The entire expense may be disallowed.

TDS Default

| Case | Disallowance |

| Payment to resident | 30% disallowed |

| Payment to non-resident | 100% disallowed |

Allowed later when TDS is deposited

Income Tax Not Allowed

Income tax, surcharge & cess → Not deductible

PARTNERSHIP FIRM RULES

Interest to partners allowed only if authorised by partnership deed and maximum 12% p.a.

Salary/remuneration allowed only to working partners.

FINAL UNDERSTANDING—Core Principle of Tax Law

Section 33 → Asset deduction

Section 34 → Genuine expense deduction

Section 35 → Disallowance for non-compliance

FINAL UNDERSTANDING

| Topic | Section | Meaning |

| Depreciation | Sec 32 | Asset-based deduction |

| Business Expenses | Sec 37 | Genuine expense allowed |

| Disallowances | Sec 40 & others | Non-compliance / illegal |

Tax law rewards: Genuine business spending, legal compliance, and proper TDS compliance. and penalizes illegal expenses, TDS defaults, Personal/capital expenses

You may also review the following blogs: