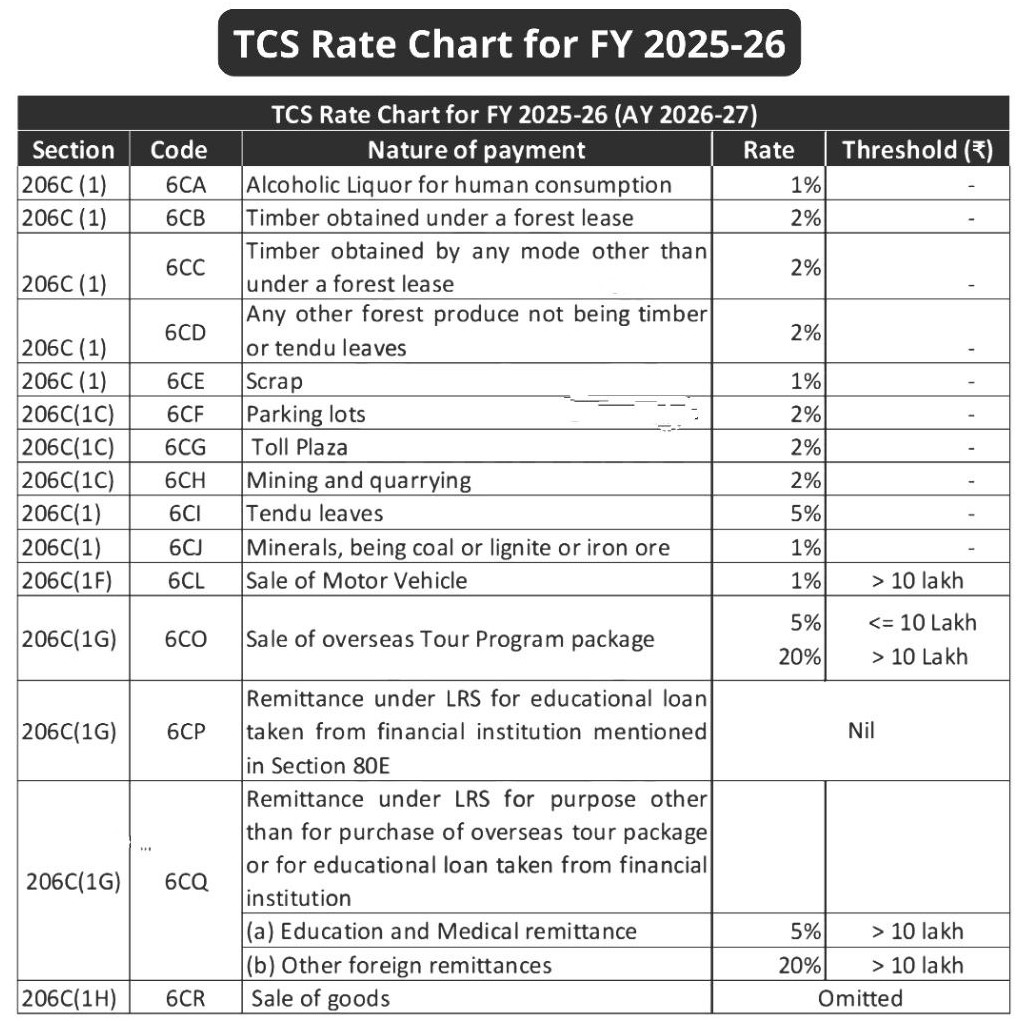

CBDT Announces 1% TCS on Luxury Goods Above INR 10 Lakh

Page Contents

CBDT Announces 1% TCS on Luxury Goods Above INR 10 Lakh

CBDT has notified that a 1% Tax Collected at Source (TCS) will now apply on sale of few prescribed Luxury goods valued above INR 10,00,000/-, with effect from April 22, 2025. This move expands the scope of Section 206C(1F) of the Income-tax Act, 1961, which previously covered only high-value motor vehicles. Key Changes U/s 206C(1F) – Finance (No. 2) Act, 2024.

Amendment to Section 206C(1F) of the Income Tax Act, 1961 via Finance (No. 2) Act, 2024, & Corresponding CBDT Notification No. 36/2025:

- Earlier income tax provision: Tax Collected at Source was applicable only on motor vehicles of value exceeding INR 10,00,000/-.

- Amendment in income tax provision: Tax Collected at Source will now also apply to other notified luxury goods exceeding INR 10,00,000/- in value, if priced above ₹10 lakh, will also attract TCS. TCS will be levied even on a single item of the above goods, if its value exceeds ₹10 lakh.

- List of Notified Luxury Goods: Luxury Goods of Value Exceeding INR 10 Lakh on Which Tax Collected at Source will Be Levied: As per CBDT Notification No. 36/2025 dated 22.04.2025, Section 206C(1F) is amended Effective from April 22, 2025

- Tax collected at the source at 1% of the sale value will be levied by the seller at the time of sale on the following goods if they exceed the INR 10,00,000/- threshold:

| S. No | Nature of Goods |

| 1 | Any wrist watch |

| 2 | Any art piece (antiques, painting, sculpture) |

| 3 | Any collectibles (coin, stamp) |

| 4 | Any yacht, rowing boats, canoes, helicopters |

| 5 | Any pair of sunglasses |

| 6 | Any bag (handbag, purse) |

| 7 | Any pair of shoes |

| 8 | Any sportswear/equipment (golf kit, ski-wear) |

| 9 | Any home theatre system |

| 10 | Any horse used for horse racing or polo |

Threshold for Applicability :

- Tax Collected at Source applies to each individual item of the specified luxury goods category if its value exceeds INR 10,00,000/-

Tax Collected at Source Rate on Luxury Goods :

- Rate: 1% of the total sale value.

Procedural Reporting & Compliance Update for Sellers/Buyers:

- Buyers: Ensure PAN is provided to the seller and check TCS credits in Form 26AS. If the buyer’s tax liability is less than the Tax Collected at Source amount, the excess can be claimed as a refund. This Tax Collected at Source will be reflected in the buyer’s Form 26AS and can be claimed as tax credit when filing the Income Tax Return (ITR).

- Sellers: Collect, deposit, and report Tax Collected at Source accurately using updated Form 27EQ. Sellers must deposit the collected tax collected at source against the buyer’s PAN. Deposit TCS against the buyer’s PAN and report in Form 27EQ. Issue TCS certificate to the buyer to support ITR claims.

- Form 27EQ (Quarterly Tax Collected at Source return) has been updated to include specific reporting codes for luxury goods u/s 206C(1F).

Rajput Jain and Associates provide end-to-end support whether you are buyers looking to claim TCS credit or a seller navigating the updated compliance and filing Form 27EQ. Get in touch for our expert assistance