All about Forensic Audit, Its Audit Techniques

Page Contents

All about Forensic Audit, Its Audit Techniques

Forensic Auditing is an independent examine a company’s financial accounts and establish whether they are accurate, free from any material misstatements, & most importantly to produce any evidence that may be used in court or legal proceedings, forensic auditing is an independent, comprehensive, and scientific procedure. Forensic Audit due to following reason.

- Growing No of Crimes, Scams etc so Forensic Audit services

- Need of expert in analysis of financial evidences – like are of Anti-Bribery Anti-Corruption

- Forensic Audit to explore in the area in the IBC Case, Mergers & Acquisitions, Fraud in Govt Bodies, Banks, Insurance Sector, Pvt as well as Public Sector undertaking’s,

- Fraud Increases the Forensic Technology Fraud Investigation and Whistle Blowing

- Fraud Risk & Non-performing asset Assessment & Litigation support

- Forensic Audit Opportunities needs of Govt Bodies, Banks, Insurance Sector, Public Sector undertaking’s,

- Investigating Agencies need Forensic Audit.

- Higher scrutiny or Tightening economic conditions of governance on companies increases sensitivity to fraud

What are the basic Limitations of Forensic Audit?

Forensic Audit as practiced by Chartered Accountants is limited to analysis of financial and operational working of the target, it lacks the scope of forensic science including verification of signatures, signs, stamps etc.

- Forensic auditing can be distracting.

- Limited time for working/analysis,

- Forensic auditing takes a lot of time. Forensic auditing

- non cooperation or Unavailability of data from the Company under audit

- High responsibility post submission of report,

- Forensic auditing can be expensive.

- Replacement of old staff with newer staff restricts / breaks the chain of audit cycle

- Limited and inconsistent sharing of data by the Banks and Company Mgt.

- Forensic auditing can affect employee morale.

The Fraud Category

| Ø Corruption

• Conflicts of Interest

• Bribery

• Economic Extortion

|

Ø Asset Misappropriation

• Cash Theft of Cash Receipts Theft of Cash on Hands • Skimming 1. Sales

2. Receivables

3. Refunds and Other • Cash Larceny

• Billing Schemes 1. Non-Accomplice Vendor 2. Shell Company 3. Personal Purchases • Payroll Schemes 1. Falsified Wages 2. Ghost Employee 3. Commission Schemes • Expense Reimbursement • Check Tampering • Register Disbursements • Inventory and All Other Assets |

-

Financial Statement Fraud

| Revenue/ Asset Understatements

o Understated Revenues o Timing Differences o Improper Asset Valuations o Overstated Liabilities & Expenses |

Revenue/ Asset Overstatements

o Fictitious Revenues o Timing Differences o Concealed Liabilities & Expenses o Improper Disclosures o Improper Asset Valuations |

Fraud Prevention measures

- Fraud prevention is the implementation of a strategy to banking actions or detect fraudulent transactions & prevent these actions from causing financial and reputational damage to the customer & financial institution.

- A strong fraud protection approach will only become more important as Fraud. Following effectiveness of Fraud Detection & Prevention step are mention below:

| Ø BANK

o Multi factor authentication

Ø INSURANCE o False claims o Algorithms to detect anomalies & patterns o Conduction of Forensic audit

Ø PUBLIC/PRIVATE SECTOR o KYE (Know your employee) o Fraud prevention software o Lay down of strong laws |

HEALTH CARE

o Payment integrity o Advance analytics OTHERS o Departmental rotation of employees o Segregating accounting duties o Guidance from forensic experts o Setting up reporting system |

Normal Forensic Audit Approach or Methodology

- Data collection with respect to correct sources and validation of the data & documents

- Record keeping in the form of hard as well as soft copies in the encrypted format

- Identifying fraudulent transactions & potential fraud

- Assess the quantum of fraud

- Differentiate between genuine business failure and fraud

- Evaluate the likely recourse available to the bank

- Need for further investigation/ action by the bank

Step by Step Approach for Methodology of Forensic Audit

- Step-1: Information available on Public domain : Legal cases by or against the company, fraud history, Promoters, background etc.

- Step-2: Information Provided by Bank: Bank statements, Loan documentations, Stock statements, committee of creditors, minutes etc.

- Step-3: Information Provided by Company’s Management: Financial data, accounting software, operational procedures etc.

- Step-4: Information review during plant visit: Working of plant, inventory, invoices, employee/worker’s records etc.

- Step-5: Information absorbed while interaction with suppliers & other stakeholders.

What is approach to be follow for Data Collection under Forensic Audit?

- Documents to be collected with a view to submitting it as an evidence in the court of law

- Maintaining several records

- Originality and authenticity of the documents should be retained

- Use of evidence as annexures

- Source of information drives the quality of evidence/ documents

Assessment Approach under Forensic Audit

| 1. Initial Tone

Ø Code of Ethics Ø Anti-Fraud Policies Ø Communication & training |

2. Proactive

Ø Forensic Data Analytics Ø Fraud Prevention Techniques 3. Reactive Ø Fraud response plan |

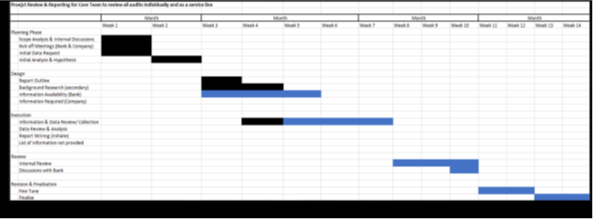

Scheduled Work Plan

What is Forensic audit Techniques?

| 1) Public document reviews and background investigations

§ Public Databases · Reliability of data · Increasing number of vendors · What type of data is available? § Regulatory Websites · Real Estate records; business registrations · Can vary by industry and state of operations § Corporate Records · Stock Transfer records; Accounting data; vendors; competitors; customers § Internet · News Sources/Newspapers · Telephone Numbers and Addresses · Legal Resources · Search Engines · Maps · Government Sites

|

2) Interviews of knowledgeable persons

Ø Interview vs. Interrogation Ø Interview the target only after completing the interviews of the peripheral witnesses Ø Gain additional information with each interview Ø Evidence from witnesses provides additional leads Ø Continuous process throughout an investigation Ø May identify additional witnesses 3) Confidential sources Ø Letters Ø Hotlines Ø Vendors & former vendors Ø E-mail Ø Former Employees Ø Current Employees Ø Customers & former vendors 4) Analysis of Physical and Electronic evidences Ø Protection/Validation of Evidence Ø Chain of Custody Ø Altered & Fictitious Documents Ø Physical Examination Ø Forgeries Ø Document Dating 5) Analysis of financial transactions Ø Horizontal/vertical analysis Ø Authorization of new vendors & employees Ø Comparison of employee & vendor addresses Ø Analysis of sales returns & allowance account Ø Management override of controls Ø Different reviews based on known industry fraud schemes |

In conclusion, financial frauds and white-collar crimes have nearly always occurred in every field and sector, laying the foundation for the development and widespread use of forensic auditing. The expertise of forensic audit professional businesses in the accounting and auditing industries is required for mitigating financial crimes.