Timeline of completion of GST Audit by GST dept.

Page Contents

GST Audit by GST department Timeline as Section 65

What does the GST Department’s audit entail?

- According to Section 2(13) of the Central Goods and Services Tax Act, 2017, a “audit” is defined as the review of records, returns, and other required documentation as specified in the Central Goods and Services Tax Act, 2017. if the tax payer has kept records or provided information required by this Act or its implementing rules in order to confirm the accuracy of the declared turnover

- Examining a taxable person’s records, returns, and other paperwork is the procedure for conducting a GST audit. The objective is to confirm that the turnover is declared, taxes are paid, refunds are received, input tax credit claims are legitimate, and GST guidelines are being followed.

Section 73 of Central Goods and Services Tax Act, 2017

According to section section 73 provide that Authority will Determination of tax not paid, short paid, erroneously refunded or ITC wrongly availed or input tax credit utilized for any reason other than fraud or any wilful misstatement or suppression of facts.

Section 74 the Central Goods and Services Tax Act, 2017

According to section section 74 provide that Authority will Determination of tax not paid, short paid, erroneously refunded or ITC wrongly availed or input tax credit utilized by reason of fraud or any wilful misstatement or suppression of facts.

What are the best practices to be adopted for Goods and Services tax audit among authorities & professional

Appropriate Evaluation of company the internal control viz-a-viz Goods and Services tax will indicate the area to be focused. This could be done by verifying:

- Statutory Audit report which has specific disclosure in regard to maintenance of record, stock and fixed assets.

- Information System Audit report & GST related internal audit report.

- Normal Internal Control Questions incorporated or designed for Goods and Services tax compliance.

- Adaptation of use of generalised audit software to aid the Goods and Services tax audit would ensure modern practice of risk-based audit are adopted.

- GST reconciliation of the books of account or GST reports from the Enterprise resource planning’s to the GSTR return is imperative.

- Checking and review of gross trial balance for detecting any incomes being set off with booked expenses.

- Review of expenses and purchases to examine applicability of RCM charge applicable to services/goods.

- Foreign exchange outgo GST reconciliation would also be necessary for identifying the liability of import of services.

- Quantitative reconciliation of stock transfer within the State or for supplies to job workers under exemption.

- Ratio analysis could provide vital clues on areas of non-compliance.

- In GST audit, Appropriate checking & examination is done to verify & authenticate the correctness of;

- GST Turnover declared by the GST Registered Supplier,

- The GST Taxes Paid by the GST Registered Supplier,

- GST Refund claimed by the GST Registered Supplier

- ITC availed by the GST Registered Supplier, and

- Classification of Goods or Service by the GST Registered Supplier.

In audit checking & examination is also completed to assess the GST compliance with the provisions of CGST Act or related rules. While Under section 65 and section 66, the audit to be conducted by a chartered accountant

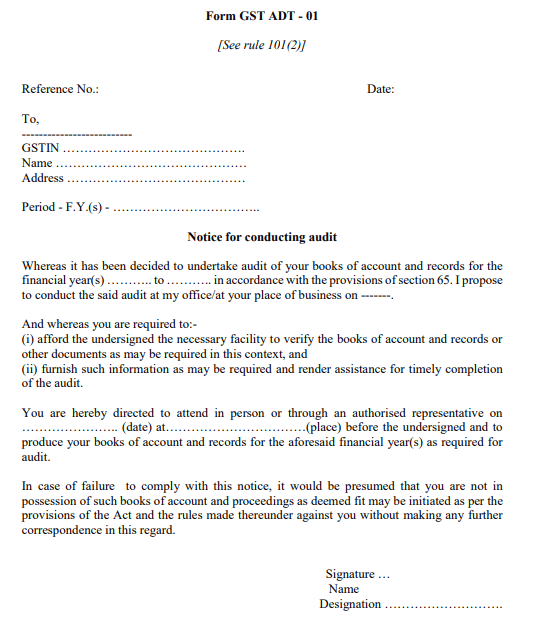

What is GST ADT Form 01?

- Tax authorities may conduct GST Audits under Section 65 of the Central Goods and Services Tax Act, 2017 . The approved officer has the power to issue a notification in FORM-GST-ADT-01 if they consider that any taxpayer needs to be audited. This form serves as notice that the audit will be conducted.

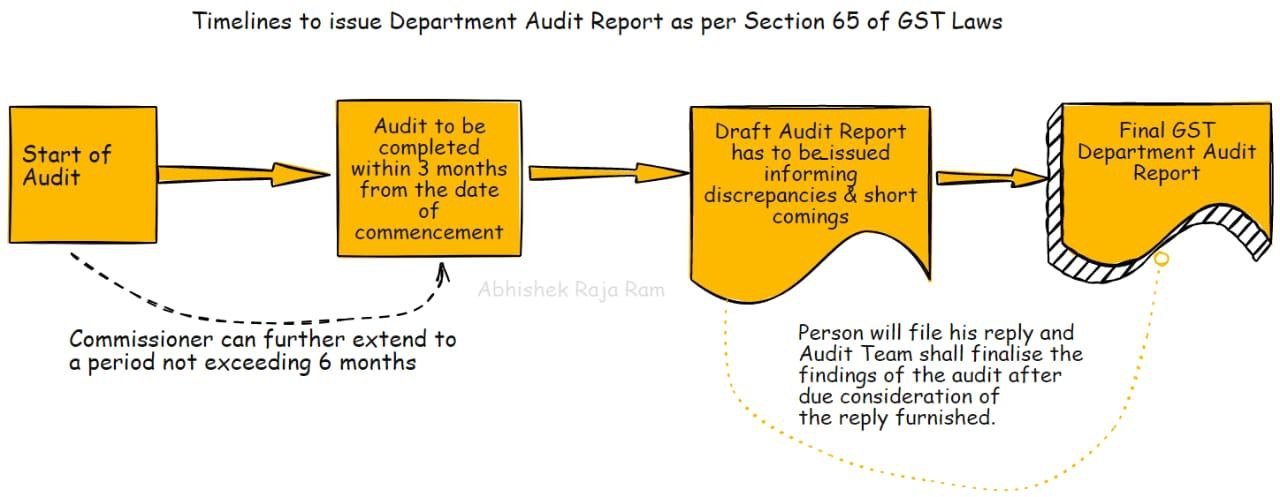

GST Audit by GST department Timeline as Section 65

- According to Section 65(1) of the Central Goods and Services Tax Act, 2017, the Commissioner or any officer designated by him may conduct an GST audit of any GST registered person for duration, with frequency, & in the way as may be specified,

- Section 65(4) of Central Goods and Services Tax Act, 2017 stipulates that an audit be completed within three months. But, if the commissioner decides that an audit cannot be performed in 3 months, the time frame may be extended by 3 months. These may be extended for an additional 6 months

Key Important Risk Factors that the GST Audit Commissioner may take into account while starting & during the conducting an GST audit include the below mention details

- Volume of Exemptions claimed by Goods & Services tax taxpayer’s year wise,

- Higher incidence of supplies without generation of E-Way Bills,

- Volume of Goods & Services tax Taxpayer’s net profit/ sale/turnover

- If any changes happened in Goods & Services tax Taxpayer’s net profit. turnover for previous years,

- Goods and services tax Taxpayer who does not file periodical return but issues E-Way Bills & inconsistency in the data declared in GSTR-1 Return & E-way Bills generated,

- Multitude of the Goods and services tax taxpayer’s legal relationships with other entities,

- Goods and services tax Taxpayer has multiple branches,

- Financial ratio analysis & if any major variations observations,

- Goods and services tax Taxpayer’s return was previously investigated for evasion,

- Goods and services tax Taxpayer who has not been audited in the pre- Goods and services tax era for a long period i.e. four to five years under Service Tax or value-added tax,

- Volume of Good and Services Tax Refund claimed by the GST taxpayer’s year wise comparison & if any variations observations,

- Goods and services tax Taxpayer categorized as High Risk,

- Any specific information received from other Govt authorities i.e. RBI, ROC, Local tax authorities, Income Tax, or any written compliant received from the person.

- Difference in Goods & Services tax turnover as declared in GSTR-3B Return or Form GSTR-1 returns for continuous period,

- Difference in Input tax credit availed & utilized as per GSTR-3B & input tax credit available as per GSTR-2A Return,

- Wrong classification of goods or services provide, effecting wrong levy of GST tax,

- Goods & Services tax Taxpayer who has requested waiver or is bankrupt,

- Mismatch in the details of Export mentioned under the GSTR-1 & information lodged on Indian Customs Electronic Gateway,