ITR Verification: Six ways to do all this

Page Contents

Income Tax Return Verification: Here have been a Six approach to do all this

The final step in filing your income tax return (ITR) is to verify it. If you ever do not verify your income tax return, it will not be found to be adequate under income tax law.

- OTP based on Aadhaar

- Creating EVC through Net-Banking

- The generation of EVC via bank account

- generating New EVC through your ATM bank

- Verification of tax returns by means of a debit account

- Send sign copy of ITR-V/Acknowledgement Recipt

Sending signed Copy of ITR-V/Acknowledgement receipt

For the Last six sept – you would like to send ITR-V to verify your tax return, please follow the points below.

- ITR-V is a one-page document that must be signed in blue ink. It must be sent either through the ordinary post office or through the speed post. You cannot send an ITR-V courier.

- The address of the revenue tax department is-Address of CPC Bangalore for speed post: ‘CPC, Post Box No-1, Electronic City Post Office, Bangalore-560100, Karnataka, India.’

- You are not asked to send any other paper along with the income tax return (i.e. ITR-V.)

- You will obtain an intimation via SMS on your mobile phone and e-mail ID once your ITR has been received by the tax department. This intimation is for the receipt of ITR-V only, the intimation for the processing of the tax return is separate.

E-verifying your ITR Return using Aadhaar Card?

You can submit your verified ITR Returns online with the help of your Aadhar Card!

Taxpayers no longer need to send a 1-page verification document, i.e. the Income Tax Return-V, to the Bangalore Income Tax Dept. Conversely, they can validate their Income Tax Returns online using the Electronic Verification Code (EVC).

Taxpayers no longer need to send a 1-page verification document, i.e. the Income Tax Return-V, to the Bangalore Income Tax Dept. Conversely, they can validate their Income Tax Returns online using the Electronic Verification Code (EVC).

The Electronic Verification Code (EVC) is a 10-digit alphanumeric code that is sent to the registered mobile of the tax filer while filing its online Income tax Returns. It helps to confirm the identity of tax filers. Such tax filers include both individuals and HUF.

Individuals are needed to self-assess their returns, even when Karta must verify the Income Tax Returns of the Hindu Undivided Family. The EVC can be created via the e-filing portal of the Income Tax Department.

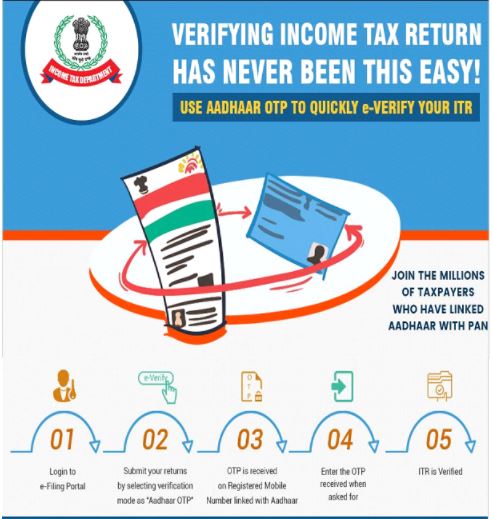

E- Verify Your Income Tax Return via Aadhaar Card

To verify your returns using an Aadhaar card, please ensure that your Aadhar card is connected to your PAN card.

Follow these instructions to link your Aadhar card with your income tax return.

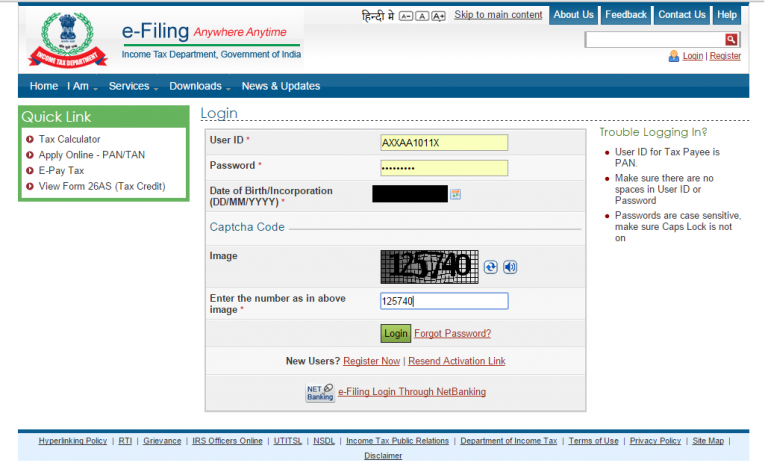

Step 1.

Log on to the e-filing website of the Income Tax Department.

Step 2.

Step 2.

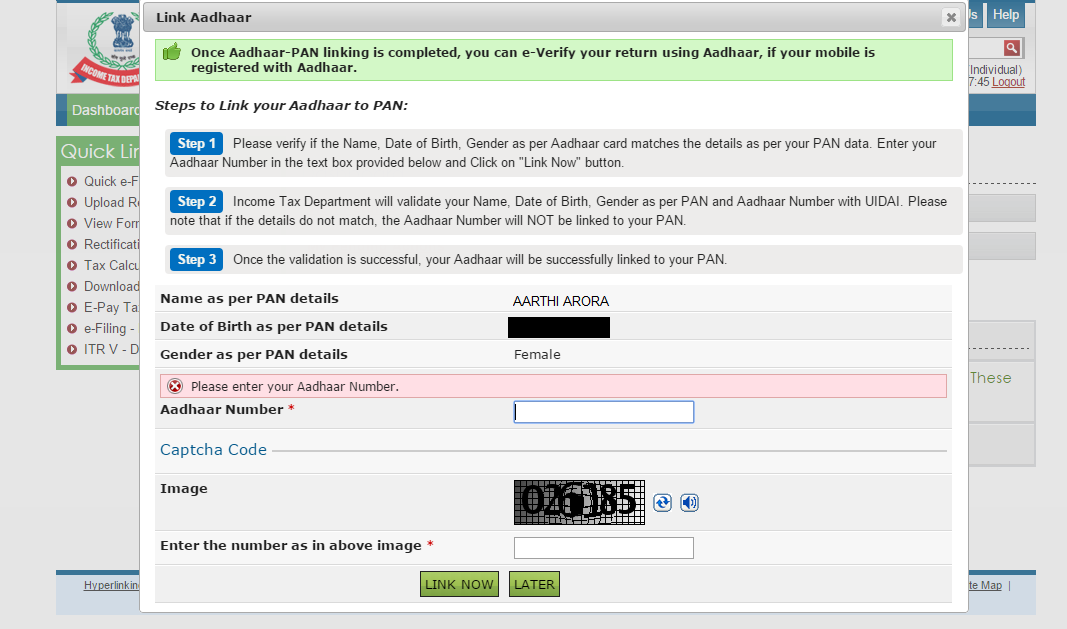

As shortly as you log in, a popup cause potential you to link your Aadhar number to your e-filing account. If you are not seeing a popup, go to the blue tab called ‘Profile Settings’ on the top bar and click the ‘Link Aadhaar’ button.

Step 3:

Pls validate your PAN information and enter your Aadhar number. Please ensure you save this information by clicking the ‘Save’ tab.

After validation, your Aadhar number will be connected to your PAN.

But when your Aadhar has been connected to your PAN, follow the link to e-check your returns:

Step 1: Upload your ITR via the Income Tax e-filing webpage.

Step 2: Once this is done, the mode of verification for your returns will be required.

You’ll see the following step:

- We have already got an EVC to e-verify my return.

- I don’t have an EVC, and I’d like to generate an EVC to e-Check my return.

- I’did like to create Aadhaar OTP to e-Check my return.

- We do not like to send ITR-V/I’d like to e-verify Later.

Select the 3rd option that says that – Create Aadhaar OTP. A one-time password will be sent to your Aadhaar registered phone number; this OTP has been only be valid for 10 minutes.

Step 3: Finally, complete the OTP number on the site and click ‘Submit. Tab’

You will then receive a letter that says “Return e-Verified successfully. Download the Acknowledgement. The same acknowledgment will be automatically sent to your registered email ID.

You have now appropriately e-filed and e-certified your income tax return.

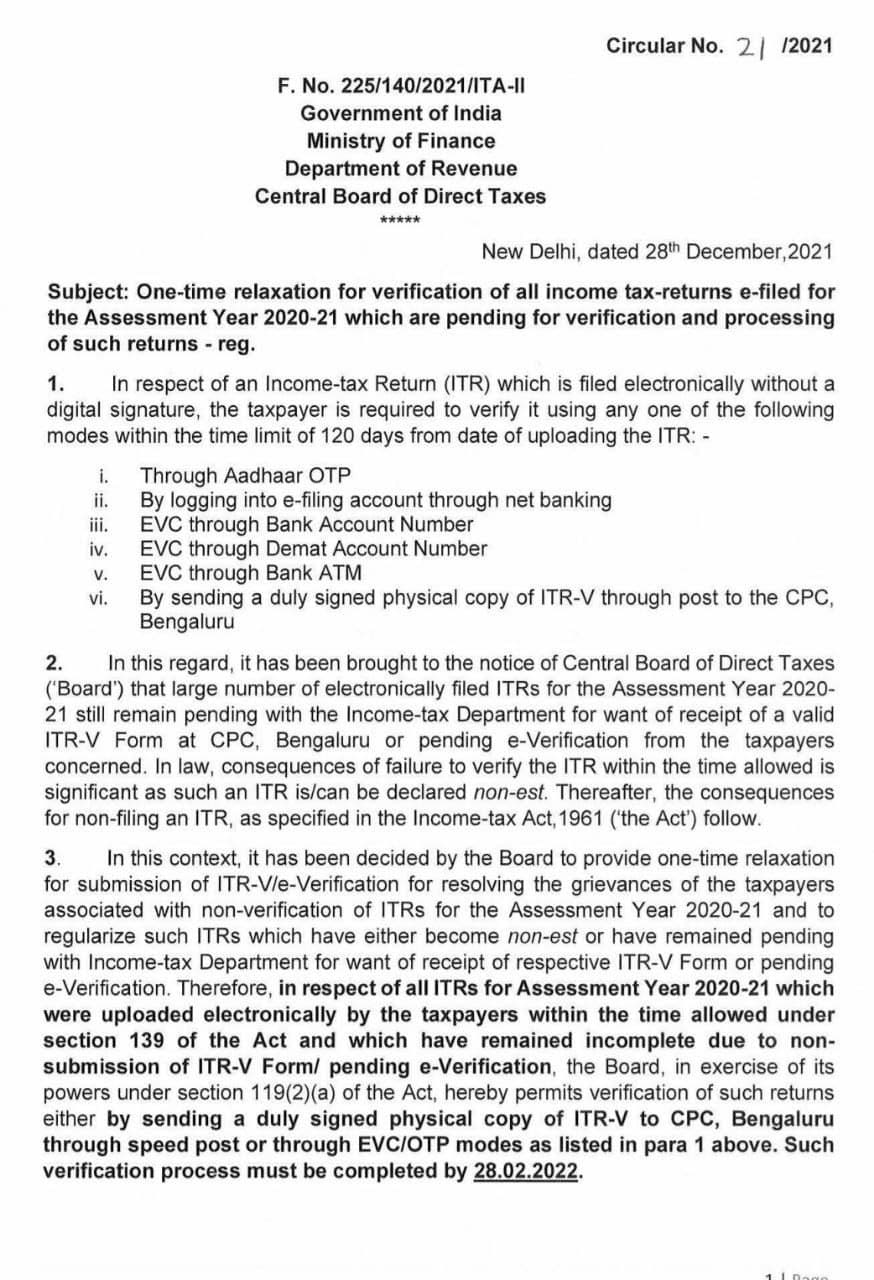

Relaxation for verification of all Income Tax Returns

- 1 Time Relaxation for verification of all income tax returns e-filed for the AY 2020-2021

- Income tax return Verification can be done till 28/02/2022.

- Income tax return Intimation Processing U/s 143(1) will be done till 30 June 2022.

New Income tax Rules for Income tax return’s verification

If Income tax return’s for Assessment Year 2022-23 filed today or in months to come upto 31.12.2022 and not verified within 30 days

- The date of verification will be taken as the date of filing. So interest and late fees will be levied accordingly

- Where these 30 days expire at any time in 2023 then the income tax return will be treated as never filed because post 31.12.2022 the income tax return cannot be filed.

- But for income tax returns filed up to 31.7.2022 time limit of 120 days shall be available.

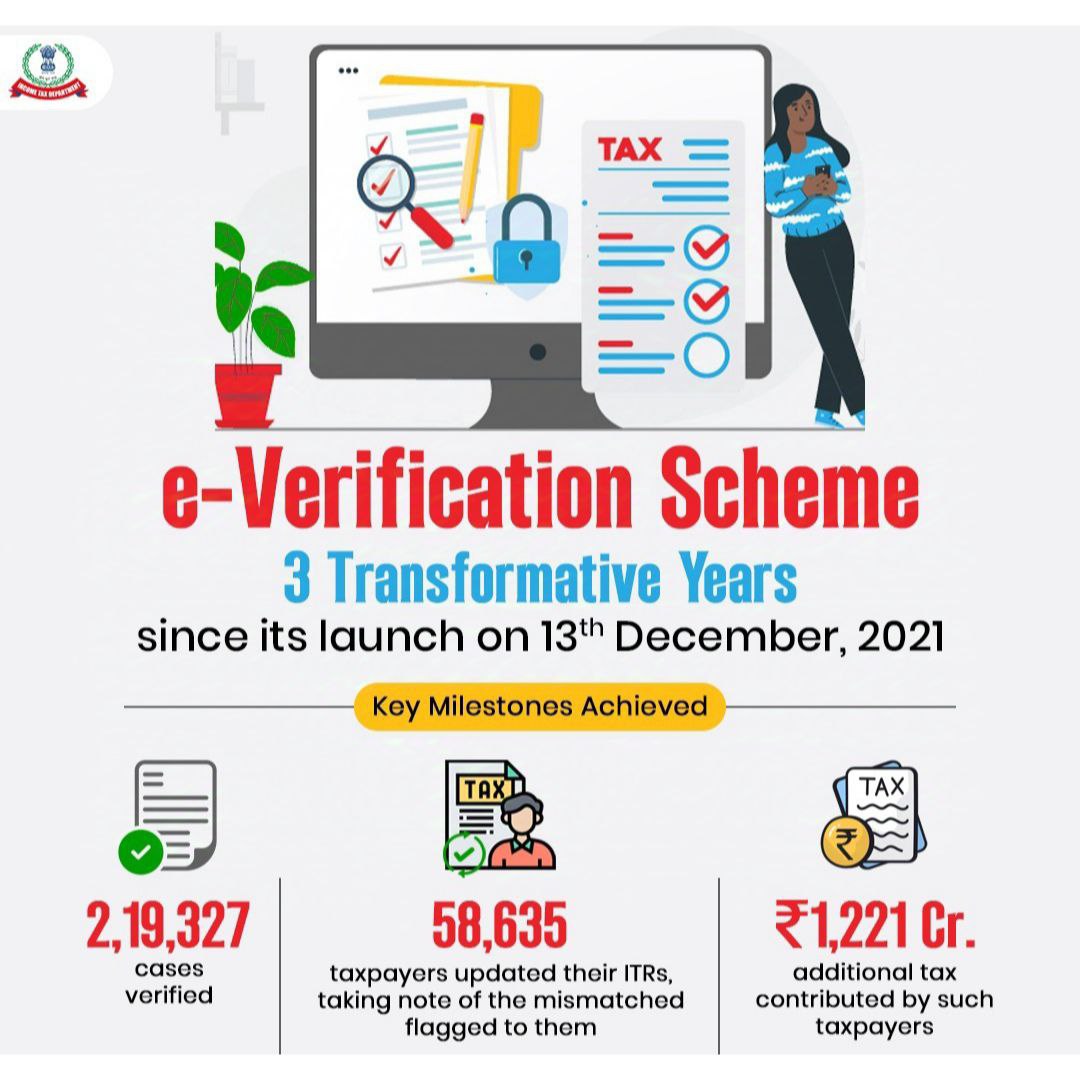

Electronic campaign: e-Verification Scheme 2024

The Central Board of Direct Taxes has launched an electronic campaign to address mismatches in income and transactions reported in the Annual Information Statement and those disclosed in Income Tax Returns for the financial years 2023-24 and 2021-22. The initiative also targets non-filers with taxable income or high-value transactions recorded in the AIS but who have not yet filed ITRs. SMS and emails are being sent to taxpayers and non-filers where discrepancies or high-value transactions are noted. This initiative, part of the e-Verification Scheme, 2021, encourages taxpayers to review their AIS, resolve mismatches, and file revised or belated returns promptly.

E-Verification Scheme 2024: Key Highlights of the e- Campaign:

- Purpose:

- To identify and resolve mismatches between transactions in AIS and ITRs filed.

- To-remind taxpayers with high-value transactions to file their ITRs.

- Encourage voluntary compliance and facilitate corrections through revised, belated, or updated ITRs.

- Target Years and Deadlines:

- FY 2023-24: Taxpayers can file revised or belated ITRs by December 31, 2024.

- FY 2021-22:Taxpayers can file updated ITRs under Section 139(8A) by March 31, 2025.

- Communication to Taxpayers: Taxpayers and non-filers will receive informational messages via SMS and email regarding discrepancies or unfiled returns. The campaign serves as a reminder to correct or file ITRs.

- Feedback on AIS: Taxpayers can review and respond to the information reported in the AIS. Disagreements with the AIS data can be addressed through the AIS portal on the e-filing website: https://www.incometax.gov.in/iec/foportal/.

- Technology-Driven Compliance: The campaign is part of the e-Verification Scheme, 2021, leveraging third-party data to identify mismatches. It reflects the government’s focus on transparency, accountability, and promoting a culture of voluntary compliance.

- Government’s Vision: This initiative aligns with the government’s vision for “Viksit Bharat” (developed India), emphasizing the role of taxpayers in contributing to economic growth.

Key Actions for Taxpayers on E-Verification Scheme 2024

This campaign highlights the Income Tax Department’s commitment to utilizing technology for simplifying compliance while promoting fairness and voluntary tax disclosure. Income Tax Dept’s suggestion is the following action on review of tax returns via E-Verification Scheme 2024 :

- Review the AIS data regularly on the e-filing portal.

- File revised or belated ITRs for FY 2023-24 by December 31, 2024.

- File updated ITRs for FY 2021-22 by March 31, 2025.

- Respond to discrepancies or inaccuracies reported in AIS through the AIS portal.

Popular article :

Tax filing Changes are taken into account when filing ITR for FY-2019-20

How to e-file a return using EVC without sending a signed copy of ITR-V?