Post incorporation compliances filings of LLP

Page Contents

POST INCORPORATION COMPLIANCES FILINGS OF LLP

The Limited Liability Partnership is one of the most prominent and popular form businesses across the world. LLPs are a combination of elegant and easy means of combining entrepreneurial initiative with requisite capital, professional expertise, and creative knowledge all under a single roof.

LLPs are taxed at par with partnership firms, which is comparatively less than that of a company. LLP has a separate legal entity and is an optimal business form that offers advantages of limited liability of a company and the adaptability of a partnership.

LLP, unlike a partnership firm, is a body corporate having separate legal entities from its partners. Thus, the LLP can own assets in its own name and can also sue or be sued by any other person. Accordingly, they can have a bank account and can enter into legal contracts with different persons. Thus, it is legally recognised as a person in the eyes of law.

Running and working of any business-like LLP, OPC, Private Limited, is not an easy task. Investing money, time and determination is required to a great extent. To cope up the formalities, registration efforts, GST filings and lots more, require great extent of expertise and therefore these businesses require services of professional experts for the same.

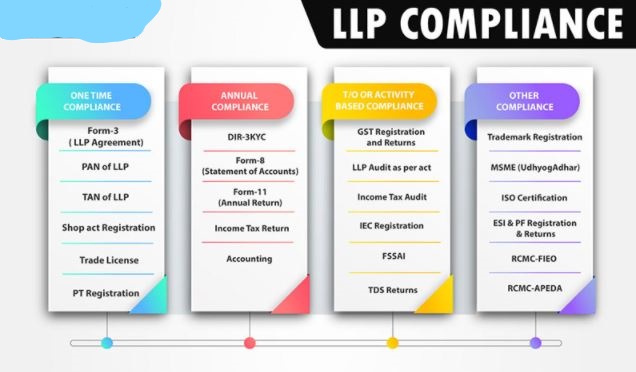

MAJOR COMPLIANCES & DUE DATE OF ANNUAL FILINGS OF EVERY LIMITED LIABILITY PARTNERSHIPS

Every Limited Liability Partnerships (LLPs) which are registered with the Ministry of Corporate Affairs (MCA) have to file the Annual Returns and Statement of Accounts for the FY. here are three main compliances which should be red-flagged by all the designated partners of LLP:-

- Preparation and filing of Annual Return under the LLP Act, 2008;

- Preparation and filing of Financial Statements of the LLP

- Filing of Income Tax Returns under the Income Tax Act, 1961.

The majority of the Stakeholders are ambiguous to the fact that whether filings of the Annual Returns are the mandatory thing even if they are not doing the business?

& the answer to the dubious question is YES! Every LLP has to be compliant even if there are no operations in the organization.

It is the responsibility of the organization to file all the required documents even if there are no operations or business during the financial year.

POST INCORPORATION COMPLIANCES FILINGS OF LLP

Let’s understand which LLP’s have to file the Annual Returns and Income Tax Return for the year :

FILING ANNUAL RETURN OF LLP:-

Annual Returns in LLP i.e… Form 11 is a Summary of LLP’s Partners like whether there are any changes in the management of the LLP.

Every LLP is required to file Annual Return in Form 11 to the Registrar within 60 days from the closure of the financial year i.e. the Annual Returns has to be filed on or before 30th May every year and for the financial year ended on 31st March the last date for filing the annual return is 30th May.

Also Read About :Post-Incorporation Compliances Filling of LLP

FILING ANNUAL ACCOUNTS OR STATEMENT OF ACCOUNTS OR P&L AND BALANCE SHEET:-

Every LLP or any other legal entity from a solo firm to a Private limited company has to prepare their accounts to get the information regarding your business that how much profit is earned by your LLP.

Every LLP has to close their accounts till 31st March this year. They are required to maintain the Books of Accounts in the Double Entry System and has to prepare a Statement of Solvency (Accounts) every year ending on 31st March.

LLP Form 8 to be filed with the Registrar of LLPs on or before 30th October every year. Therefore, 30th October is the last date for filing annual accounts this year.

Note:– Form 8 or Annual Statements for the year is applicable to those LLP which is registered till the 30th of September. If your LLP is registered on or after the 1st September 2017 then you do not require to file LLP Annual Statements in the year.

FILING INCOME TAX RETURNS FOR THE LLP:-

Every LLP has to file the Income Tax Returns for the year. In simple words, LLP is a separate legal entity so with the partner’s income tax return you have to always file the LLP Income tax return where you show your LLP’s Income and calculate the tax liability and pay the taxes to the government of India. LLP have to calculate their tax liability from their financial statements for the year.

Mostly Income Tax Return the Last date is 31st July 2017 (unless extended) this year for the Individual and legal entities. However, in the case where an Audit is required, the last date for filing Income Tax returns is 30th September.

If the LLP has not carried any business during the year ended 31.03, the LLP has to file a NIL IT RETURN with Income Tax Authorities.

Note:- Filing of Income Tax Return is Applicable on all the LLPs which are registered during the financial year. Therefore, it’s not a matter if your LLP is registered after 01-10-20… still you have to file an Income tax return from the date of incorporation till 31-03.

AUDIT REQUIREMENT UNDER LLP ACT, 2008:-

Only those LLPs whose annual turnover exceeds Rs. 40 lakhs or whose contribution amount exceeds Rs. 25 lakhs are required to get their accounts audited by a qualified Chartered Accountant. Meaning thereby, All the statements of accounts are certified by the CA.

More read: Procedures for the conversion of partnership firm into Private limited company

AUDIT REQUIREMENT UNDER INCOME TAX ACT, 1961:-

Audit of accounts is a mandatory requirement under the Income Tax Act when the annual turnover of LLP is more than Rupees one hundred lakhs.

CERTIFICATIONS FROM COMPANY SECRETARY IN PRACTICE (PCS):-

In the case of LLPs with a turnover of more than five crore rupees in a financial year or a contribution of more than Rupees fifty lakh, the annual return shall be certified by a Company Secretary in Practice.

A Summarized way Post Limited Liability Partnership formation return Compliances is prescribed below:-

| S. No. | Particulars | Due Date/Status |

| 1) | LLP Agreement Form 3 | It is required within Thirty days of the formation of Limited Liability Partnership |

| 2) | Filling of PAN Application | It is essential Required to be obtained PAN immediately, acts as an identification number for every taxpayer, and is required for opening Bank Account also |

| 3) | Freshly Opening of Bank Account in Limited Liability Partnership Name | The current account needs to be opened for carrying out business transactions |

| 4) | Statement of Account and Solvency in Form 8 | It required to be file within 30 days from the end of six months of the FY to which it relates |

| 5) | Annual Return of Limited Liability Partnership- Form 11 * | It required to be file within sixty days of closure of the FY |

| 6) | Filing of ITR Return

If an Audit is not required to be made if an Audit is required to be made |

31st of July every year 30th of Sept every year |

| 7) | KYC Compliance of designated Partner’s | it should be completed on or before the thirty of Sept every year |

| 8) | Compulsory Audit of Accounts of books of Account | If Capital contribution exceeds twenty-five Lakhs or Turnover exceeds Rs. forty Lakhs |

Also Read About: LLP Incorporation and Annual Compliances

CONSEQUENCES FOR NON-FILING LLP ANNUAL RETURNS AND ACCOUNTS:-

If there is a delay in filing Form No. 8 and Form No. 11 of LLP, you will have to pay a penalty as applicable on today’s date. If the filing is not done within the stipulated time, there is a penalty of Rs. 100 per day till it is compiled. You cannot close or wind up your LLP without filing Annual Accounts.

So if you don’t file mandatory forms on time with the MCA, your LLP turns into unlimited statutory liability until the day it is compiled.

The provisions of the Act require LLPs to file the documents like Statement of Account and Solvency (SAS) in Form 8 and Annual Return (AR) in Form 11 within the time specifically indicated in relevant provisions.

The LLP Act contains provisions for compounding of offenses which are punishable with fine only. Further, for defaults/non-compliance on procedural matters such as time limits for filing requirements provisions have been made for charging default fees (on daily basis) in a non-discretionary manner.

To avoid the consequences of heavy penalties, it would be advisable to comply on time within the stipulated due date of filing.

Also Read About: Key takeaway on the conversion of LLP

Actions are taken by the Registrar of Companies against the LLPs who have not filed their Returns and Statement of Accounts:-

Apart from the above consequences and penalties, the Registrar has the right to strike off the LLPs who are not filing their Financial Statements (Form 8) and Annual Returns (Form 11) for a period of two immediate financial years.

In the line of the above right and under the provisions of Section 75 of the LLP Act, 2008 read with Rule 37 of the LLP Rules, 2009, the following registrar of Companies has issued the public notice proposing striking of the name of LLPs who are not filing their Annual Returns and Financial Statements:

Popular Blog:-