All About Allowances & Income Tax Exemption

Page Contents

Key takeaways on Taxable, Non-taxable & Partly Taxable Allowances

What is Allowances?

- The allowance shall be the monetary benefit provided by the employer to the employee over and above the daily salary. These benefits are given to offset the costs that may be incurred in order to facilitate the discharge of the service, for example, the travel allowance shall be paid to the foot expenses incurred for going to the workplace.

- It is a defined amount of money that a salaried person earns from his employer to cover a certain form of expense over and above salary. for instance, Companies offer workers overtime allowances if they work longer than fixed regular hours. Likewise, there are many other allowances that are granted to salaried people.

- These are considered as part of the wages and are taxable, with the respect of those for which the various provisions of the Income Tax Act have given specific exemptions. Any of these deductions are taxable under the Head of Wages.

- Some of them may again be partially taxable and some others are non-taxable or entirely excluded from taxes. These allowances can be categorized into three buckets on the basis of their respective tax treatment-Taxable, Non-taxable & Partly Taxable under Income tax.

Basic Distinction between an allowance and a reimbursement:

- Allowance: Allowances are usually part of the pay package of an employee to cover expenses made or to be made that may occur in the course of his or her jobs. For eg, if a customer uses his own car to drive from home to work, then the employer would have to pay a transport allowance for the same.

- Likewise, for the good of employees, there are also such allowances provided by employers. Allowances are classified into three parts: allowances that are taxable, non-taxable, and partly taxable under the income tax act 1961.

Reimbursement:

- A reimbursement is a form of the cost incurred on behalf of the employer that is paid to the employee/worker. Reimbursements are typically related to company costs and do not add much to the employee’s salary. A reimbursement is, not taxable at all under the income tax Act 1961.

Partially-Taxable allowances |

Taxable Allowances |

Non-Taxable allowances |

|

|

|

· Sumptuary allowance paid to judges of Supreme Court and High Courts

· Compensatory allowance paid to judges of Supreme Court and High Courts · HRA up to 40% of basic salary (50% in case of employees staying in 4 metros – Delhi, Mumbai, Chennai, and Bangalore) subject to actual rent paid to be more than HRA plus 10% of basic · Conveyance allowance upto ₹ 1,600 per month or ₹ 19,200 per annum · Payments to government employees posted abroad · Allowance for UN employees |

|

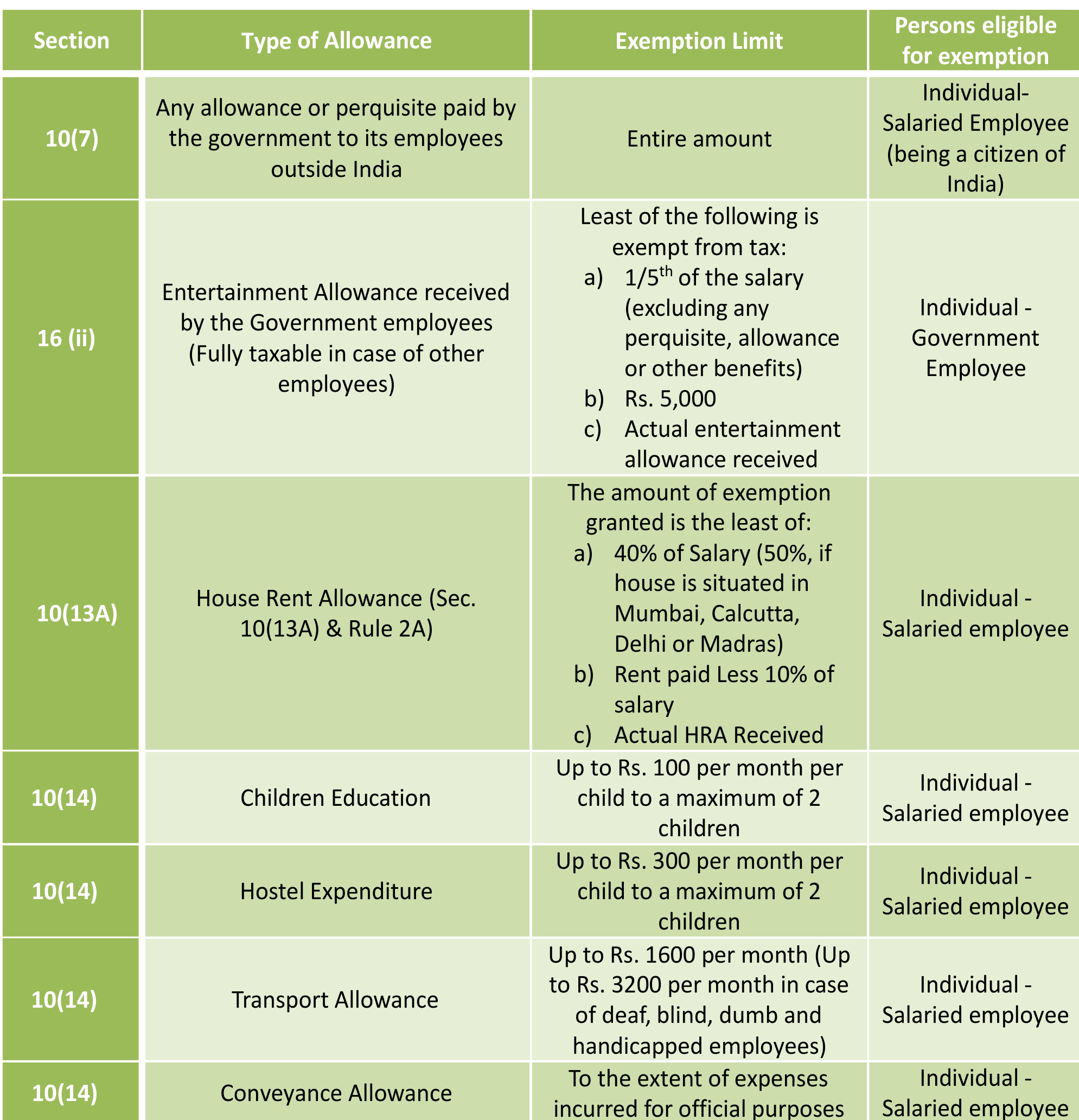

Income Tax Exemption

- There is a provision for exemption from income tax in compliance with Chapter III of the Income Tax Act, 1961. There are only a few forms of stated income that can be exempted from paying tax.

- This means that certain income will not be added at the time of the income tax calculation. The most common incomes excluded from income tax are listed below:

Taxable Allowance

- Taxable allowances are kinds of remuneration that are considered as part of a wage and are not exempted in entirety or in part under any of the Income Tax sections. Few below of the common allowances that are part of this verity are:

Special allowance Categories and Exemption

-

Entertainment Allowance:

Entertainment allowance is the Remuneration of money given to an employee to make payments for customer meetings, hotels, drinks, meals, business outings, and more towards their customers’ hospitality.

For all private-sector workers, the allowance is fully taxable. Moreover, Government workers may claim exemption from this tax, as alluded to in section16 (ii), and the amount of exemption is limited to the minimum of the following three;

-

- 20% of gross salary (excluding all other deductions, rewards and benefits),

- Real entertainment allowance, and

- 5,000.

-

Allowance for overtime:

Employees who tend to work longer than the operational hours determined by the company earn this payment. Because of immediate tasks and a firm schedule, that can happen. Any Overtime Allowance received by the workers is fully taxable remuneration under Income tax.

-

Dearness Allowance:

As a cost of living change to neutralize the effect of inflation, the Dearness benefit is required to be charged to public sector workers and pensioners and the disparity is the cost of living for workers living in various cities and towns.

-

Meal Allowance:

Meal allowances are provided to their staff for meals/refreshments / Tiffin facilities and are Fully taxed to be a levy on it under Income tax.

-

Compensatory City Allowance (CCA):

Companies provide Compensatory City Allowance to their workers to compensate for comparatively high housing expenses in urban areas. This allowance is used in towns and communities where the cost of living is greater relative to workers working in other places to encourage and maintain staff.

- Interim allowance: The interim allowance is an allowance given ahead of a final allowance by the employer. The interim allowance is solely subject to taxation under Income tax

- Cash Allowance: Cash allowance for expenses such as vacation allowance, marriage allowance, and other similar employer-provided allowances, and it is wholly taxable under the Income tax act 1961.

- Servant Allowance: The allowance given to employers for the procurement of servant workers is always taxable.

- Project Allowance: When a company gives workers with an allowance to liquidate the costs of a job, it is considered a job allowance that is entirely taxable.

- Warden Allowance: If an employee pays tax to an employee who serves at every institute as a warden/keeper. This allowance is probably considered to be taxable.

- Non-practicing allowance: Every non-practicing allowance paid to them is taxable when a practitioner is affiliated with clinics with different laboratories or medical institutes.

Non-Taxable Income

Non-taxable allowances are such allowances which are entirely excluded from taxation and are part of an individual’s salary. Here is the collection of totally non-taxable deductions.

- Allowances owed to government employees overseas: This payment is deemed to be non-taxable as Indian government servants are paying when completing their job term in other countries.

- Income tax Allowances paid to employees of UNO: Allowances given to workers of UNO are totally non-taxable.

- An Allowances paid to HC & SC Judges: The allowances paid to the judges of the High Court and the Supreme Court are fully tax-free. Such allowances are referred to as sumptuary allowances.

- Compensatory Allowances: If any compensatory allowances are earned by the Judges of the High Court and the Supreme Court, these allowances are fully exempted under income tax.

Allowances that are partially taxable

- As defined in Income-tax Rule & regulation, partially taxable allowances are those allowances which, may be exempted from tax to a certain extent. Here is some allowances which are partially taxable;

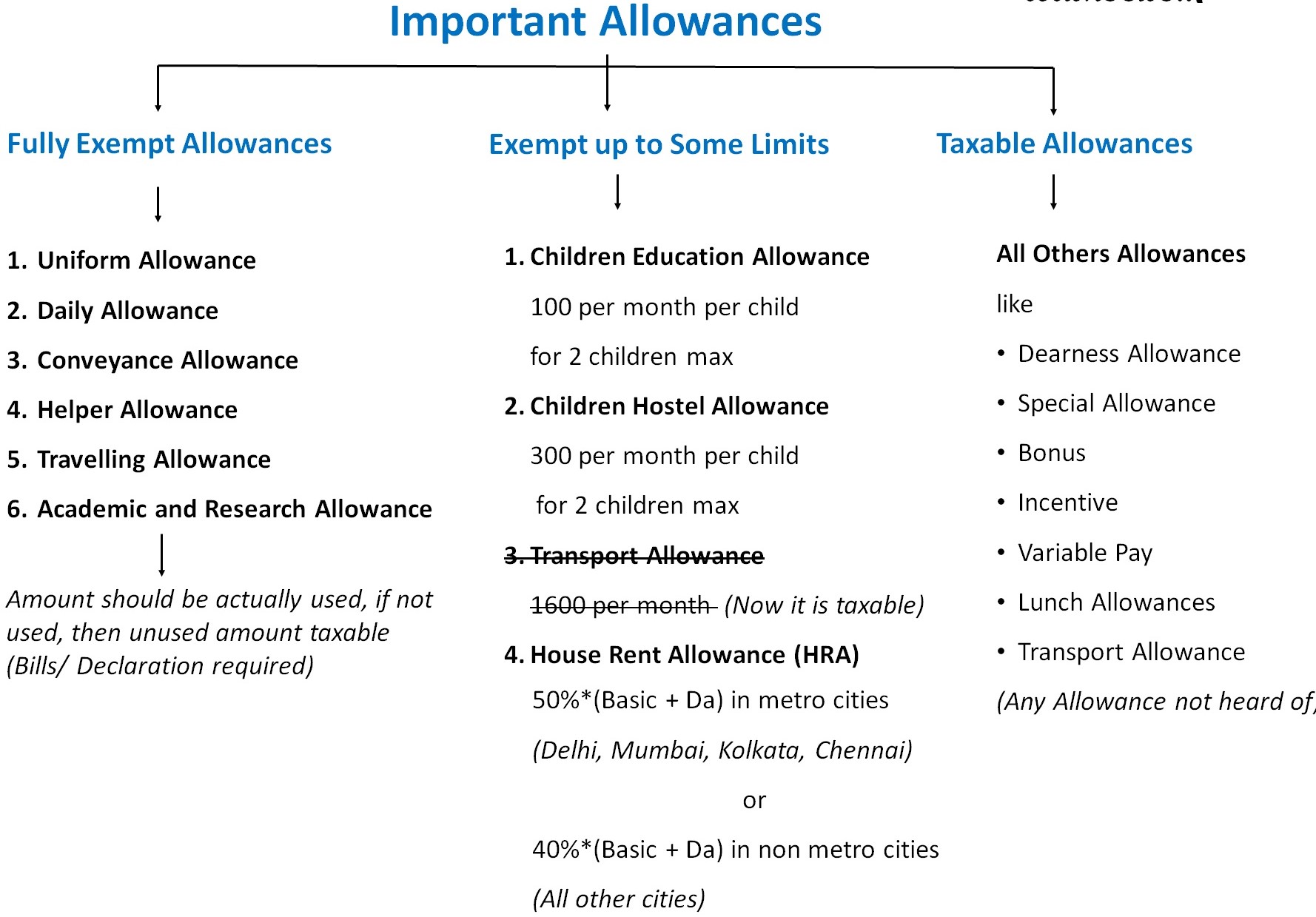

- Limit on Conveyance Allowance Exemption:

This kind of allowance is given to workers every day for traveling from home to their office. With compliances of Income Tax Act, 1961, if allowances is received up to Rs. 1600, then it is fully exempt but If a conveyance allowance is received in excess of Rs. 1,600, it will be declared as Taxable.

-

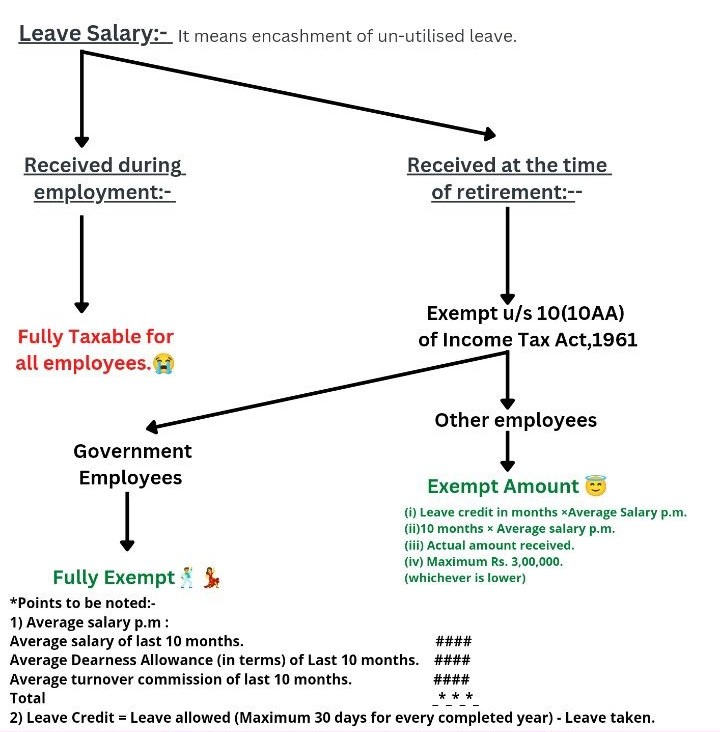

Leave Travel Assistance – LTA tax exemption

Leave travel assistance (LTA) obtained from the employer for the expense of domestic travel to the hometown or for holidays once every two years by train or air may be reported as excluded income for self-employed and family members.

This deduction can be asserted explicitly by an individual from the employer only. The LTA is entitled to argue twice in the four-year block. 2018-21 is the new block. Employees, however, are now permitted to carry one unclaimed LTA until next year.

-

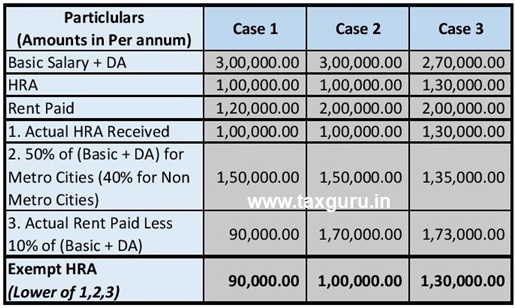

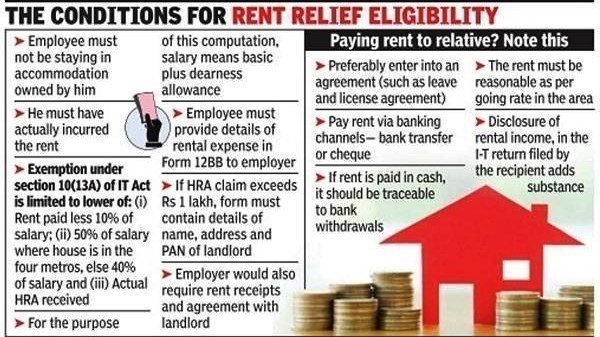

Limit on House Rent Allowance (HRA) Exemption:

Salaried individuals receive house rent allowance (HRA) from their employer. If the employee lives in rental accommodation and pays rent to the owner, an exemption from HRA under Chapter 10 of the Income Tax Act is possible.

- It is also possible to claim an HRA exemption by submitting proof of rent paid to the employer or at the time of filing the ITR. After adjusting the exemption, the taxpayer just needs to find out how much exemption he can take advantage of and then recalculate the total taxable income.

- House rent allowance is given by an organization to workers to support them with helping with their housing costs. But this allowance is completely taxable if a person does not live in a rented space. employees can demand a deduction under section 10 (13A) for the house rent allowance if:

- Actual HRA received

- These should be up to 50% of the basic salary, If the worker stays in metro cities such as Delhi, Mumbai, Chennai, or Bangalore,

- 40% of basic salary, if the worker stays in non-metro cities

- Excess rent charged annually exceeding 10% of the basic salary + DA

- You need the PAN of the Landlord When do you need to pay rent More than 1 lakhs to the

- Landlord: If you really have taken a rented house and pay more than Rs 1 lakh annually – remember to provide the landlord with a PAN.

- Otherwise, you can miss out on the HRA exemption. Landlords without a PAN must be able to send you a declaration by reference to Circular No. 8/2013 of 10 October 2013.

Requirements for the use of HRA exemptions:

The eligibility requirements for the HRA exemption are as follows:

- The individual is to be a salaried employee.

- In his salary structure, he has the HRA part.

- He’s going to be staying in rented accommodation.

List of metropolitan areas for HRA exemption needs to be revised

Renters paying rent to NRI owners must note to subtract TDS by 30% before paying for rent.:

If you really have taken a rented house and pay more than Rs 1 lakh annually – remember to provide the landlord with a PAN. Otherwise, you can miss out on the HRA exemption.

Landlords without a PAN must be able to send you a declaration by reference to Circular No. 8/2013 of 10 October 2013. Renters paying rent to NRI owners must note to subtract TDS by 30% before paying for rent.

Exemption from Medical Allowance:

This is an allowance provided by an employer if the worker or any of the members of his family becomes ill and needs extended medical attention.

Moreover, If the treatment bill is up to Rs. 15000 than it is fully exempt but if the bill is more than Rs. 15,000 it becomes taxable. But For the FY 2019-20 Medical Allowance is removed from the exemption list from the income tax act.

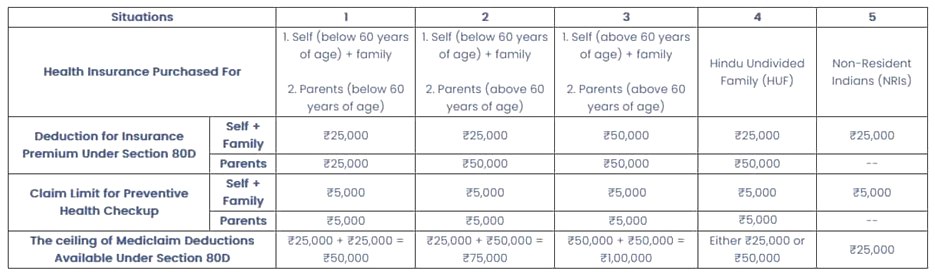

In addition, the budget also proposed to enhance the allowance from Rs. 30,000 to Rs. 50,000 for health insurance premiums under Section 80D of the Income Tax Act.

This often comes to the people as a great relief. And, in the case of senior citizens suffering from serious illnesses, the deduction would now be a huge Rs.1 lakh. The benefits of the new standard deduction implemented in the 2018 budget of the Union will be enjoyed by an unprecedented 2,5 crore people made up of salaried workers and pensioners.

Tax benefit of Health Insurance

Special allowance:

- As per section 14(i), a special allowance is given to an individual for the execution of his duty. This allowance does not come under the prerequisite range and it is partially taxable under the income tax act.

Nine salary elements that will help workers reduce their tax pressure

- Children education allowance

- Phone bill reimbursement

- Food coupons

- House Rent Allowance (HRA)

- Gift voucher

- Employees’ Provident Fund (EPF)

- Leave Travel Allowance (LTA)

- Car maintenance allowance

- Hostel expenditure allowance

Popular blog:-