Income Tax Deduction u/s 80C-80U

Page Contents

INCOME TAX DEDUCTION UNDER SECTION80C-80U TO INDIVIDUALS, HUF

Income Tax Deduction

The income Tax deduction is a decrease in tax liability from the gross taxable income. Tax deductions are reduced from total income, also known as adjusted gross income.

As per the provision of the income tax act, 1961 the amount of tax deductions varies as per different earnings are handled accordingly. An additional deduction of Rs. 1, 50,000 for home loan interest is given for the purchasing of affordable houses of up to Rs.45,00,000 for the current year ended on March 2020.

Section 80C-80U

Section 80C

Section 80C is by far the most commonly used choice for income tax savings. In this case, a person or a HUF (Hindu Undivided Families) who invests or spends on fixed tax-saving schemes can claim a tax deduction of up to Rs. 1.5 lakh.

With effect from 1st April 2016, the income tax abolished section 88 and introduced the new Section 80C in this place. This section analyzed the payment made under this provision. Eligible taxpayers are entitled to require gross deductions of up to Rs. 1,50,000 per year.

The Indian Government also supports some of them as tax-saving instruments (PPF, NPS, etc.) to enable individuals to save and accumulate in retirement. Spendings/investment u / s 80C is not approved as a deduction from profits resulting from capital gains.

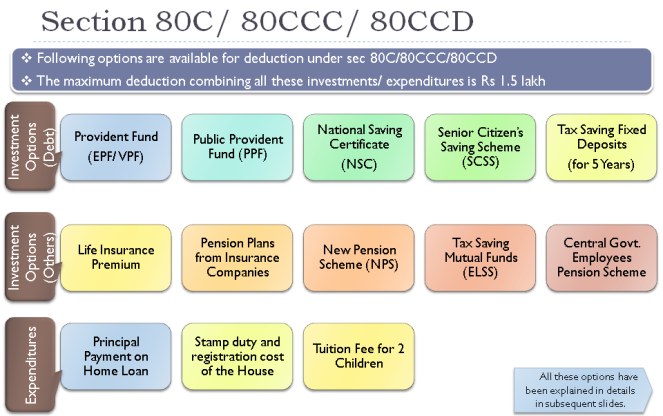

This ensures that if the individual’s income consists of capital gains on its own, Section 80C can not be used for the purposes of saving tax. Any of the investments mentioned below are eligible for exemption under Section 80C, 80CCC, and 80CCD(1) up to a limit of Rs 1.5 lakh. All the individuals and Hindu undivided families are eligible for deduction under section 80C of the income tax act, 1961.

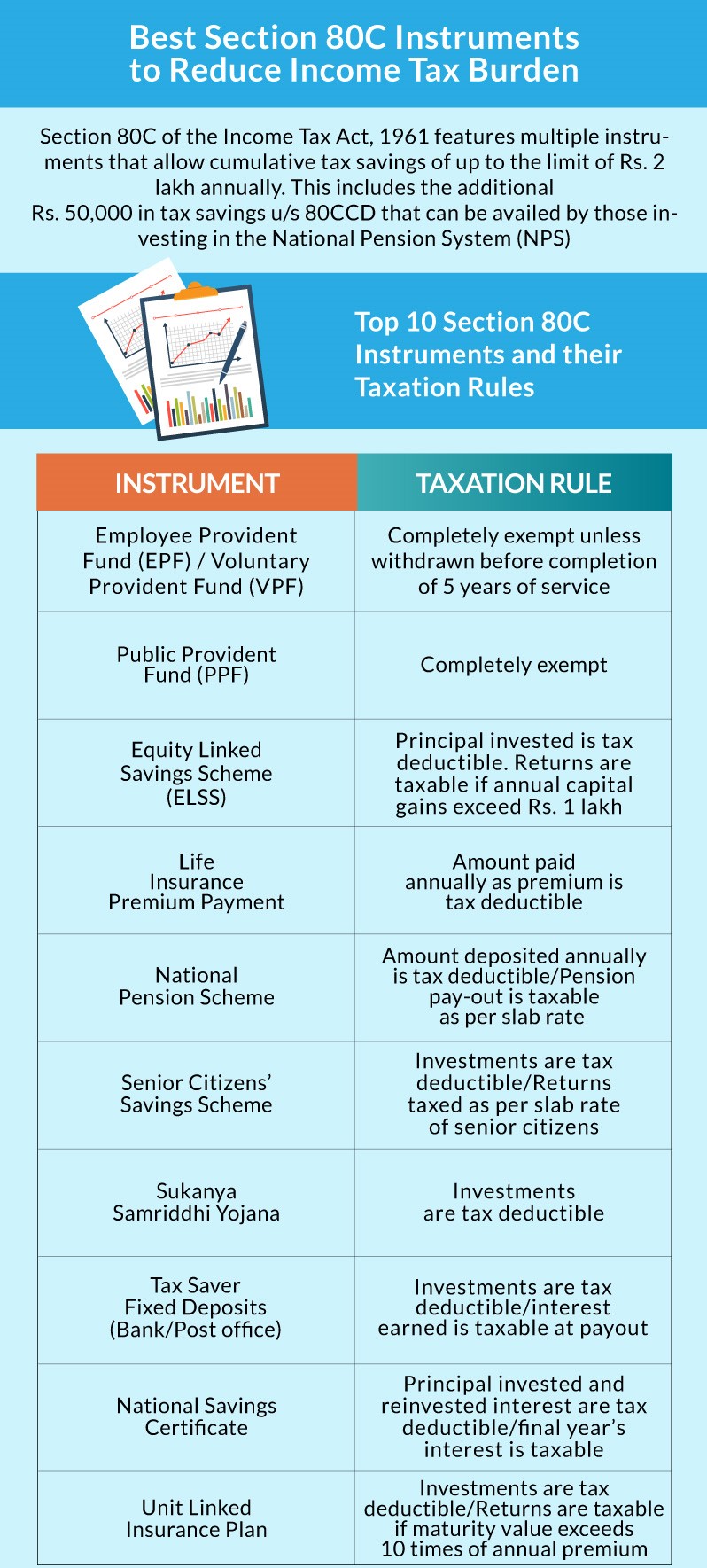

Best Section 80C instruments That can reduce your tax Burden

The following investments and expenditures are included in this section:

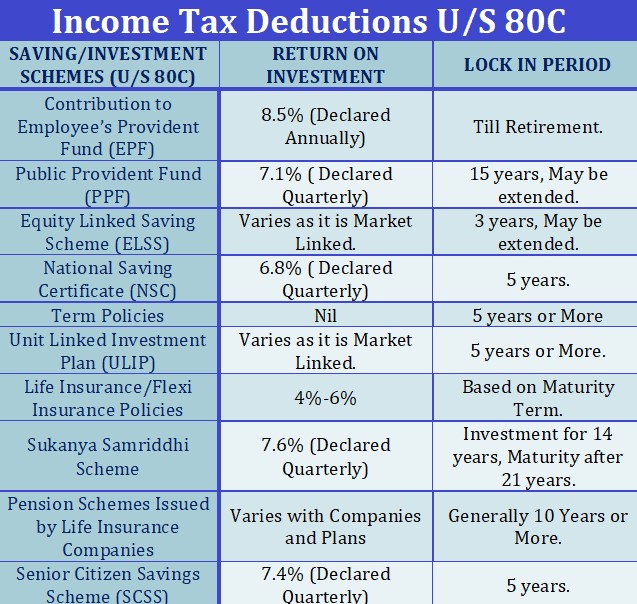

Tax Saving Investment Options under section 80C

| 80C Investment Option | Lock-In Period | Return | Risk | Taxability |

|---|---|---|---|---|

| PPF | 15 Years | 7.9% | Risk-Free | Interest: Exempt Withdrawal: Exempt |

| SSY | 21 Years | 8.4% | Risk-Free | Interest: Exempt Withdrawal: Exempt |

| ELSS | 3 Years | 10-15% (approx) | Risky | Dividend is exempt |

| FD | 5 Years | 7-8% (approx) | Risk-Free | Interest is taxable |

| NSC | 5 Years | 7.9% | Risk-Free | Interest is taxable |

| SCSS | 5 Years | 8.6% | Risk-Free | Interest is Taxable |

| ULIP | 5 Years | 8-10% (approx) | Risky | Returns are taxfree subject to certain conditions taxable |

| NPS | Till Retirement | 8-10% (approx) | Risk | Return: Partially exempt |

-

Investment in Public Provident Fund:

You will claim a deduction for Rs. 1,50,000 per year for contributions made in the Public Provident Fund account. Receipts are tax-free on maturity and withdrawal.

-

Investment in National Savings Certificate:

under section 80C, the National Savings Certificate is liable for deductions in the year of acquisition. Interest earned on such certificates is liable for tax deductions, but it becomes taxable at the date of retirement.

- Fixed deposit investment: According to section 80C, interest received on fixed deposits for a period of not less than five years is eligible for a tax deduction. Tax-exemption on interest earnings on deposits with banks has been raised from 10,000 to 50,000 only for senior citizens. In addition, under section 194A, TDS is not required to be excluded and it has been applied to both FD and RD schemes.

-

The premium on a Life insurance policy:

As per section 80C of the income tax act, 1961, You will claim a refund for the premium charged for a life insurance policy.

- Contribution to Employee Provident Fund: You will demand a tax exemption for the payment made under section 80C to the Employee Provident Fund. The government will contribute 12% of the EPF contribution to new workers (with less than 3 years of employment) in all sectors. In contrast to the contribution made 12 percent earlier, for new women employers (with less than 3 years of employment) contribute just 8 percent of the wage as an EPF contribution.

- Equity-oriented mutual funds: A tax-deductible can be claimed on contributions made in any mutual fund unit, whether or not it is listed on the stock exchange.

-

Repayment of the principal on the housing loan:

You will demand a tax deduction under section 80C for the principal amount charged on the home loan.

- Payments of Tuition fees: You can demand a tax deduction for the tuition fees charged under section 80C. The deduction for each individual is available for 2 children. Thus, a deduction can be requested for up to 4 children, 2 for each parent.

ADDITIONAL DEDUCTION CAN BE CLAIMS NOT COVERED U/S 80C

Section 80CCC and 80CCD : Tax deductions U/s 80CCC and 80CCD for investments in pension fund

For the contribution made in Pension Funds, you can claim a tax deduction under Section 80CCC and 80CCD. If you have contributed any amount to earn a pension under any insurance plan, then you will demand a tax exemption under 80CCC.

Even so, if you have paid up to 10 percent of your income to any pension fund launched by the Govt, such as the National Pension Scheme, then you can claim a tax deduction U/s 80CCD.

Note: According to the Income-tax act, 1961, a Total deduction that can be demanded under Sections 80C, 80CCC and 80CCD is Rs. 1, 50,000. Under section 80CCD, an exclusive tax advantage is available for NPS subscribers.

As per the Income-tax act, 1961, Tier 1 account holders earn an extra savings allowance of up to Rs.50, 000 in NPS. This Tax deductions under Section 80CCC and 80CCD is over and above the deduction applicable U/s 80C i.e of Rs. 1, 50,000.

Section 80TTA: Interest on savings accounts

Under Section 80TTA, you will demand a tax deduction on interest received on a savings bank account. A maximum amount of Rs.10,000/- is entitled to the deduction. The income received will first be added under the head of income other sources, only after that, the deduction will be asserted.

Section 80CCF: Investment made in long-term infrastructure bonds

Under section 80CCF, you can claim a tax exemption on an investment made in government-notified long-term infrastructure bonds. An overall deduction of up to around Rs. 20,000 can be claimed.

Section 80CCG: Investment made in equity saving scheme

The deduction is also known as the Rajiv Gandhi Equity Saving Scheme. For an investment made in listed shares or mutual funds, you will demand a tax deduction. The amount of deduction is 50% of amt. invested in equity share. However, the maximum deduction permitted under the provision cannot exceed Rs. 25,000.

Income Tax Deduction under Section 80D

There could be Five various situations U/s 80D for claiming the deduction; these are:

- If the individual and parents are both aged more than 60 years, the deduction available is Rs.25,000 each, i.e. a total of Rs.50,000.

- If the individual, family, and parents all are aged more than 60 years, then the deduction available is of ₹50k each, i.e., a total of ₹1,00,000.

- The individual and family are aged less than 60years, but the parents are aged more than 60 years, then the deduction for self and family is Rs. 25000, in addition to Rs.50,000 for parents. The cumulative deduction is allowed is Rs.75k.

- For HUF members, the total deduction is Rs. 25,000 each (self and family plus parents), i.e. a total of Rs. 50k.

- The available deduction is also Rs. 25,000 each for non-resident individuals, i.e. a total of Rs. 50k.

Section 80D Payment for the medical insurance premium and health check-ups

Under this section, you can claim a tax deduction for the payment of medical insurance premiums for yourself, your spouse, or any child. In addition, tax exemptions that may not surpass Rs.5k can also be demanded on money spent on health check-ups.

Section 80E: Interest paid on the Education Loan

Under section 80E, you will claim a tax deduction on interest paid on the repayment of the Education Loan. The deduction may be demanded only on the interest paid on the repayment of the loan and not on the amount of the principal.

Section 80EE: Interest on loan taken for the purchase of residential property

Under section 80EE, you can demand a tax deduction for interest payable on a loan taken for the purchase of a residential property. The overall claimed deduction is Rs. 50k under the income tax Act.

Section 80G and Other: Deduction on made donations Under Section 80G, 80GGA, 80GGB and 80GGC

- For a general contribution received within a financial year, you will demand a tax deduction under section 80G.

- If a contribution is made for scientific research or rural development, deductions under section 80GGA may be demanded.

- If contributions are made to any political party, deductions under sections 80GGB and 80GGC may be demanded

Section 80GG: Tax exemption for leases purchased in favors of FY-20-21

For the house rent expenses, you can demand a tax deduction under section 80GG. Nevertheless, in Section 80GG, you can only demand a deduction if you have not earned a house rent allowance. If you earn an HRA, you are not entitled to a deduction in this section. Under section 80 GG, you can demand a deduction, if

- rent paid by you is greater than 10% of your total income subject to a maximum of Rs. 5,000 per month or

- 25% of your total income, whichever is less.

Summary of Different type of Income-tax exemption as per the Income-tax Act, 1961

| Section | Permissible limit | Type of investment, expense, or income | Eligible claimants |

| 80C | Maximum ₹ 1,50,000 (aggregate of 80C, 80CCC and 80CCD) | PPF, EPF, Bank FD’s, NSC, LIC premium, tuition fees | Individuals, HUFs |

| 80CCC | Maximum ₹ 1,50,000 (aggregate of 80C, 80CCC and 80CCD) | Pension funds | Individuals |

| 80CCD | Maximum ₹ 1,50,000 (aggregate of 80C, 80CCC and 80CCD) | Pension fund initiated by the central government | Individuals |

| 80TTA | Up to ₹ 10,000 per year | Interest on bank savings account | Individuals and HUFs |

| 80CCG | 50% of amount invested subject maximum of ₹ 25,000 | Equity saving schemes | Individuals |

| 80CCF | Up to ₹ 20,000 | Long term infrastructure bonds | Individuals and HUFs |

| 80D | For individual taxpayers– Premium up to ₹ 25,000 in case of individuals and up to ₹ 50,000 for senior citizens For HUFs- Premium up to ₹ 25,000 and up to ₹ 50,000 in case the member insured is a senior citizen or super senior, citizen |

Medical insurance premium and Health check-up | Individuals and HUFs |

| 80E | No limit defined | Interest on repayment of Education loan | Individuals |

| 80EE | Maximum ₹ 50,000 | Interest on loan payable for acquiring a residential house property | Individuals |

| 80G | Differs with the amount of donation | General donations of any recognized society | Individuals, HUF’s, Companies, Firms |

| 80GGA | Depending on the quantum of donation | Donations to Scientific Research or Rural development | Those who do not have income from business or profession |

| 80GGB | Depending on the quantum of donation | Donations to political parties | Indian companies |

| 80GG | ₹ 5,000 per month or 25% of total income whichever is less | Rent paid if HRA is not received | Individuals not receiving HRA |

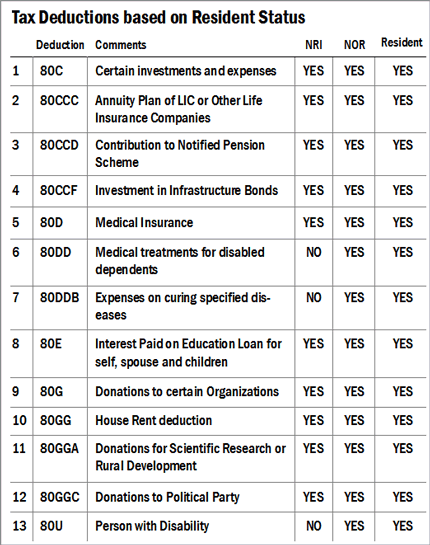

Summary View on Tax Exemption on the bases of residence status

The above list of tax deductions under the income tax law makes us the most of tax deductions with careful tax planning which will decrease your tax liability & you may save on taxes

Popular Blog:-

Deduction u/s 80CCD of Income Tax Act, 1961

New TDS deduction No cash transactions exceeding 1 Crore -Section 194N