Input credit on Construction Services

Page Contents

Input Credit on Construction Services

ITC ON SERVICES TAX

RULE 2(l): Input Services

“Input Service” means any service,-

- It is used by a provider of output service for providing an output service; or

- used by the manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products, up to the place of removal, and includes services used in relation to modernization, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion, market research, storage up to the place of removal, procurement of inputs, accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, security, business exhibition, legal services, inward transportation of inputs or capital goods and outward transportation up to the place of removal;

But excludes services,-

(A) Specified in sub-clauses (p), (zn), (zzl), (zzm), (zzq), (zzzh) and (zzzza) of clause (105) of section 65 of the Finance Act (hereinafter referred as specified services), in so far as they are used for-

Construction of a building or a civil structure or a part thereof; or

laying of foundation or making of structures for support of capital goods, except for the provision of one or more of the specified services; or

| Sec. 65(105)(p) | Architect’s Services |

| Sec. 65(105)(zn) | Port Services |

| Sec. 65(105)(zzl) | Other Port services |

| Sec. 65(105)(zzm) | Airport Services |

| Sec. 65(105)(zzq) | Construction services in respect of commercial or industrial buildings or civil structures |

| Sec. 65(105)(zzzh) | Construction services in respect of residential complexes |

| Sec. 65(105)(zzzza) | Works contract service |

- The definition of input services excludes (a) Construction of a building or a civil structure or a part thereof; or (b) laying of foundation or making of structures for support of capital goods. Thus CENVAT CREDIT of service tax paid for such specified services are not allowed.

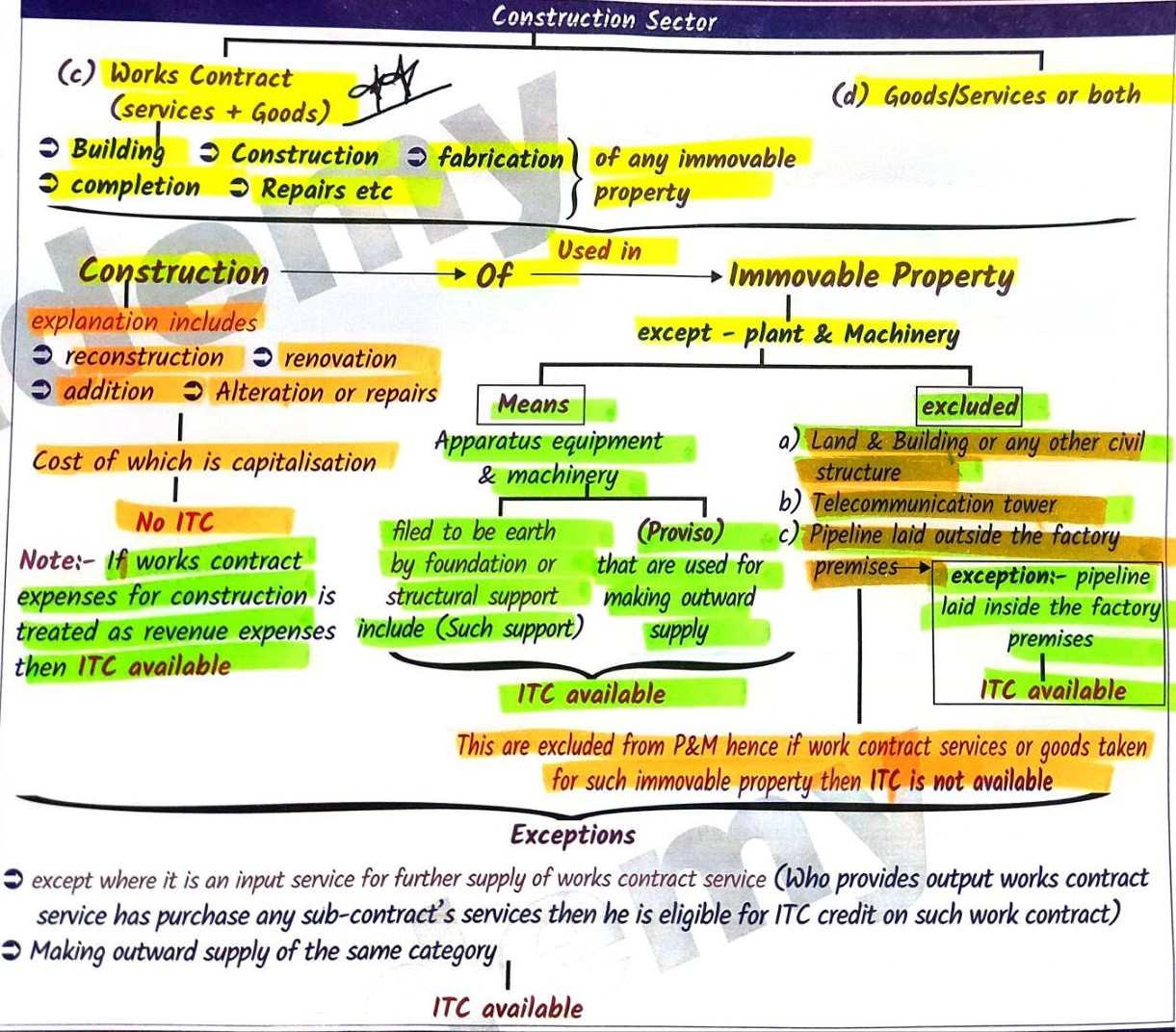

ITC IN CONSTRUCTION SECTOR

Availability of ITC for a Works Contract under GST :

- Except for plant and machinery, ITC is not applicable on works contract services supplied for the building of an immovable property.

- ITC for works contract, on the other hand, can only be obtained by those who are in the same line of business and who use such services for the continuing supply of works contract services.

ITC Availability for Self-Constructed Structures:

- ITC is not eligible for goods/services/both obtained by a taxable person for the building of an immovable property (other than plant or machinery) on his own account, even if such goods or services or both are utilised in the conduct or furtherance of his business. Can ITC be claimed for GST paid on the building of immovable property that will be rented out?

- With the help of an interesting case, Safari Retreats Private Limited against Chief Commissioner of Central Goods and Service Tax, we will shed light on this concept (Orissa High Court)

Summary of GST ITC in Constructed Sector