Guidelines Issued By CBDT on Sec 194R

Page Contents

Clarifications/ Guidelines Issued By CBDT on Section 194R

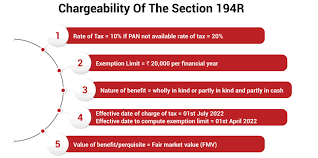

1). The deductor is not needed to check whether the amount of perquisite/ benefit that he is providing would be taxable in the hands of the recipient under section 28. Income tax Section 194R casts an obligation on the person responsible for providing any benefit or perquisite to a resident, to deduct tax at source @ 10%. There is no further needed to check whether the amount is taxable in the hands of the recipient or under which section it is taxable. Moreover, Section 194R would apply irrespective of the fact whether the perquisite/ benefit is in the nature of capital asset or not.

2) Tax deducted at source provisions given under section 194R would not be applicable in case of one-time loan settlement with borrowers or waiver of loan granted on reaching settlement with the borrowers by the below origination:

➢ Public company engaged in providing long term finance for construction or purchase of houses in India for residential purpose and which is registered in accordance with the direction/ guidelines issued by the National Housing Bank formed under National Housing Bank Act 1987

➢ State Financial Corporation

➢ State Industrial Investment Corporation being a Govt company, engaged in the business of providing long[1]term finance for industrial projects;

➢ Deposit taking NBFC

➢ PFI – Public Financial Institution

➢ Scheduled Bank

➢ Cooperative bank (other than a primary agricultural credit society)

➢ Primary co-operative Agricultural & Rural Development Bank

➢ Systemically Important Non-deposit Taking NBFC

➢ Registered ARC – Companies

-

-

Valuation Of Perquisite/ Benefit :

-

➢ Where the perquisite/ benefit provider has purchased the perquisite/ benefit before providing it to the recipient, the value of such perquisite/ benefit shall be the purchase price.

➢ In case perquisite/ benefit provider manufactures such items given as benefit/perquisite, the value of such benefit/perquisite shall be the price that it charges to its customers for such items. It has been further clarified that Goods and Services tax would not be included for the purposes of valuation of benefit/perquisite for Tax deducted at source under section 194R.

4) Threshold of INR 20,000 is with respect to the financial year, calculation of value or aggregate of value of the benefit or perquisite triggering deduction under section 194R has to be counted from 1.04.2022.

if the value or Total value of the perquisite or benefit provided or likely to be provided to a resident exceeds INR 20,000 during Financial Year 2022-23 (including the period up to 30th June 2022),

Provisions of Income Tax Section 194R shall apply on any perquisite or benefit provided on or after 1st July 2022. But, it is to be noted that the benefit or perquisite which has been provided on or before 30th June 2022, would not be subject to tax deduction under Section 194R.

- The Tax deducted at source Implications Where Product Is Given To A Social Media Influencer For Using The Product And Reviewing The Same By Making An Audio/Video About The Same:

➢ In case of benefit or perquisite being a product like car, mobile, outfit, cosmetics, etc and if the product is returned to the manufacturing company after using for the purpose of rendering service, then it will not be treated as a benefit/perquisite for the purposes of Section 194R.

➢ But, if the product is retained then it would be in the nature of benefit/perquisite and tax is required to be deducted accordingly under section 194R.

6) Company “XYZ ” Gifts A Car To Its Dealer “ABC” And Deducted Tax On This Benefit under section 194R. Dealer “ABC” Uses This Car In His Business. Will He Get Deduction For Depreciation In Calculating His PGBP Income? Once Company “XYZ ” has deducted tax on gifting of car in accordance with Section 194R and dealer “ABC” has included this benefit as income in his Income tax return, it would be deemed that the “actual cost” of the car for the purposes of Section 32 shall be the amount of benefit included by dealer “ABC” as income in his Income tax return. So, dealer “ABC” can get depreciation on fulfilment of other conditions for claiming depreciation.

7) Tax deducted at source under section 194R is not required to be deducted on issuance of bonus or right shares by a company in which the public are substantially interested, where bonus shares are issued to all shareholders by such a company or right shares are offered to all shareholders by such a company, as the case may be