Digital Currency different from Virtual Digital Assets

Page Contents

Digital Currency & Virtual Digital Assets

What are means of Virtual Digital Assets?

- Finance bill 2022 defined the term “virtual digital asset” by entering a new clause (47A) under the income tax

- According to proposed new clause under the definition of a a virtual digital asset is proposed to mean any information or code or No or token (not being Indian currency or any foreign currency), generated Via cryptographic means.

The Cryptocurrency by whatever name called, would be considered a virtual digital asset, taxable in India. if it meets the below conditions:

- Cryptocurrency in the form of information, code, numbers, or tokens;

- It acts as a digital representation of value;

- It’s generated through cryptographic means or otherwise;

- It has some inherent value; and

- Cryptocurrency allows for the storage and transfer of its units or tokens.

Govt issued digital currencies both foreign as well as Indian have been particularly excluded from the scope of virtual digital assets as per Budget 2022;

What is advantages of Cryptocurrencies?

Few of advantages of Cryptocurrencies are mentions below:

- Cryptocurrency investments can create big profits, values have skyrocketed over last last few years.

- No involvement of 3rd parties such as banks & financial institutions.

- faster money transfers with decentralized systems & Cheaper which do not collapse at a single point of failure.

What is Disadvantages of Cryptocurrencies?

Few are some disadvantages of Cryptocurrencies are mention below:

- Leaves a digital trail which can be deciphered allowing authorities to track financial transactions of individuals.

- Cryptocurrencies include high energy consumption for mining activities, price volatility & use in criminal activities.

Above provided digital nature, transactions are prone to be hacked.

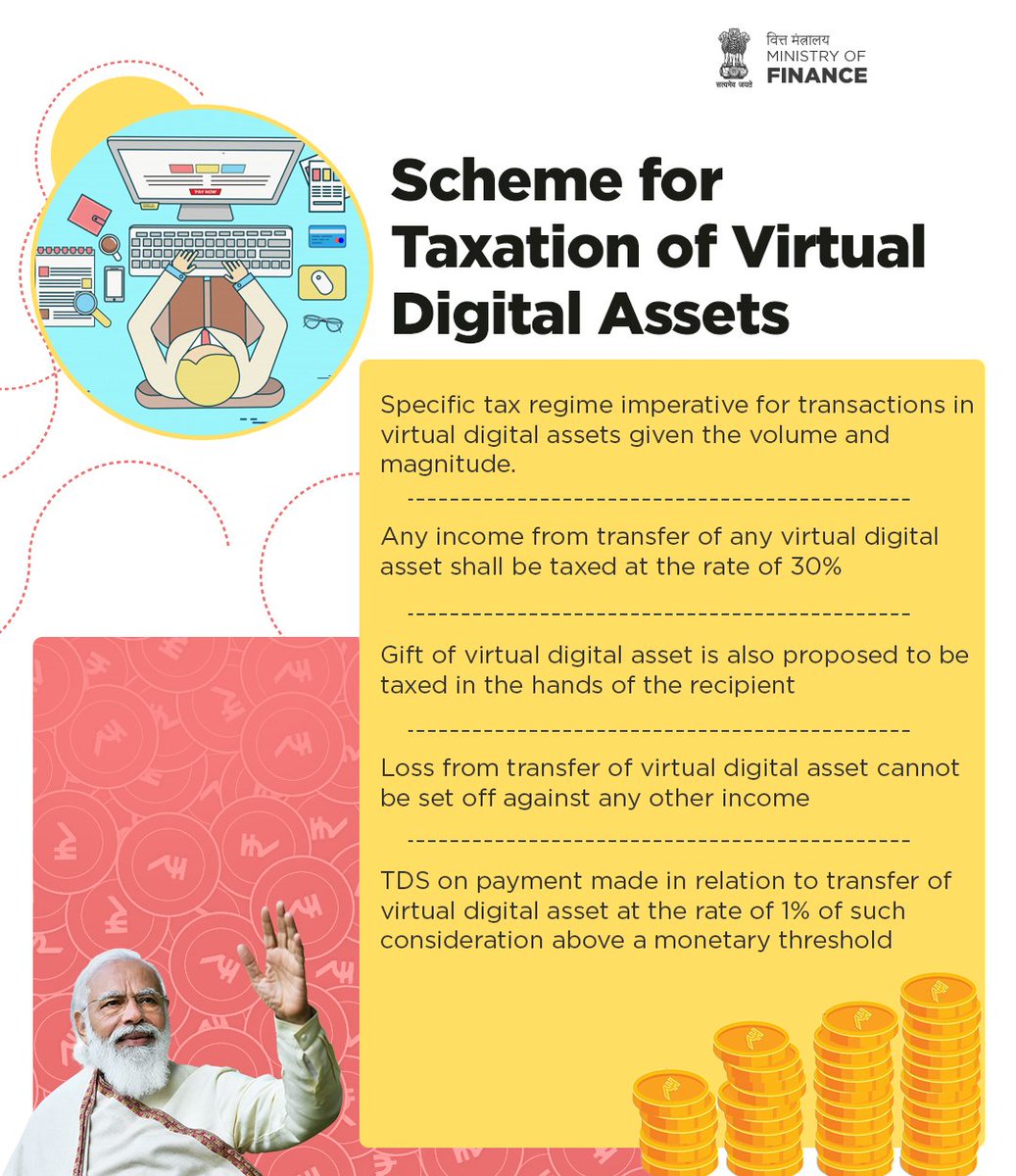

What is Justification Behind Taxation in india?

- In recent times, virtual digital assets have grown in popularity, and the amount of trading in these assets has significantly increased.

- Furthermore, a market is forming in which payment for the transfer of a virtual digital asset can be performed using another virtual digital asset.

- These considerations have required the creation of a specific tax regime.

TDS on virtual digital assets.

- India’s Finance Minister in her Budget 2022 recommended a 30% tax on income from virtual digital assets.

- Finance Minister also recommended a 1% above a monetary threshold Tax Deduction at Source (TDS) on payments made in relation to the transfer of virtual digital assets.

Providing Virtual Digital Assets as a Gift

- Gifts of virtual digital assets would be taxable as well, probably at prices reflected in mainstream indices, or at fair market value or ready reckoner rates set by the government from time to time.

- But because NFTs are non-fungible by nature, and each token’s worth is independent of the value of other tokens, this approach may not be viable for assessing their value.

Digital Currency of India’s Central Bank

- While the Indian government continues to reject cryptocurrencies as legal tender, the Finance Bill recognises the potential applications of blockchain technology and announces India’s very own Central Bank controlled Currency (CBDC), which will serve as the digital counterpart of the Indian rupee.

- So because RBI would be the regulator for such a digital currency, it would be different from other cryptocurrencies, which are now decentralised.