Online in 54EC Capital Gain Bonds help to Save LTCG

Page Contents

Online in 54EC Capital Gain Bonds help to Save Long Term Capital Gain Tax

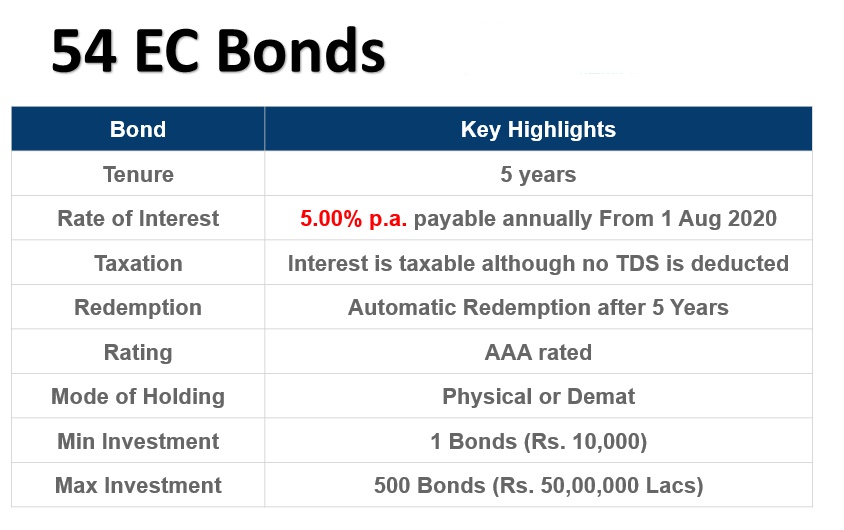

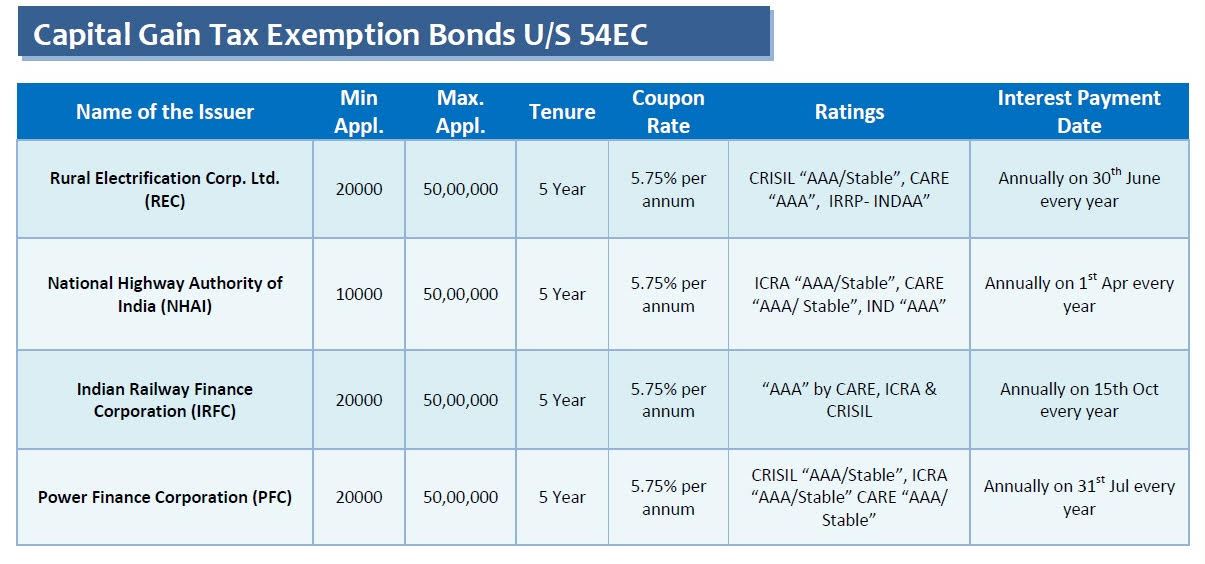

The below are the provisions of Section 54EC:

- The long or short Capital gain will not to be charged on investment in certain specific bonds.

- Investment of the long-term asset specified by the acquirer (by the capital gain from the transfer of one or more property or buildings or both) cannot exceed INR 50 Lakhs for the financial anniversary and in subsequent financial years in which the property or building or both are transferred.

- Exemption amounts are available in accordance with section 54EC of the Act on income tax. The exemption amount allowed under section 54EC is less than:

- Capital gains are invested on the stipulated long-term assets.

- 50 lakhs of INR

- An exemption advantage under Section 54EC of the Revenue Tax Act is qualified for all categories of persons.

- The exemption is only available for the profit resulting from the transfer of capital assets on a long-term basis (being land or building or both).

- A capital gain (wholly or partially) has been invested by the assessee in the long-term assets specified.

- The investment is to be made within six months of the transfer date.

- An assessee may not exceed 50 lakhs of INR investment in the long-term assets specified during the FY.

Withdrawal of U/s 54EC exemption

-

- In the case of transferring the long-term specified asset or converting it into the money prior to the end of the 3 year or 5-year period, the exemption claimed under section 54EC is withdrawn.

- The exemption claimed in respect of Section 54EC, in the event of transfer/conversion, is considered to be income in the form of capital gains in the preliminary year of the long-term transfer or conversion of specified capital.

- It must be noted here that if the assessee took any loan or advances for the fixed asset for the long term, the same shall be considered as converted to money on the date of the loan or advance.

Salient Features of Finance Bill

- No change in Tax Rate. All persons including individuals, HUF, Firms, and Companies to pay the same tax. However, Education cess is being increased from 3 to 4 % to be known as Education and Health cess.

- However for Domestic Companies having total turnover or gross receipts not exceeding Rs 250 crores in the Financial year 2016-17 shall be liable to pay tax at 25% as against the present ceiling of Rs 50 crore in the Financial year 2015-16.

- Long-term Capital gain exemption under section 10(38) in respect of listed STT paid shares being withdrawn.

- However, capital gain up to 31.1.2018 shall not be taxed as cost of acquisition will be taken as Fair Market Value as of 31.1.2018.

- Tax on STT paid long-term capital Gain will be 10% under Section 112A. Further such tax will be liable for TDS.

- Standard Deduction of Rs 40,000 for salaried employees. However, the benefit of transport allowance of Rs 19,200 and Medical Reimbursement of Rs 15,000 under Section 17(2) is being withdrawn. Thus net benefit to the salaries class is only Rs 5,800.

- Agriculture Commodity Derivative income /loss also not to be considered as speculative under section 43(5).

- Income Computation and Disclosure Standards (ICDS) being given statutory backing in view of the decision of Delhi High Court decision.

- Marked to market loss computed as per ICDS to be allowed under section 36.

- Gain or loss in Foreign Exchange as per ICDS to be allowed under new section 43AA.

- Construction Contract income to be computed on percentage completion method as per ICDS.

- Valuation of Inventory including Securities to be as per ICDS.

- Interest on compensation, enhanced compensation. Claim or enhancement claim and subsidy, incentives to be taxed in the year of receipt only as per new Section 145B.

- Conversion of stock in trade to the capital asset to be charged as business income in the year of conversion on Fair Market value on the date of conversion.

- 54EC benefit of investment in Bonds to be restricted to Capital gain on land and building only. A further period of holding being increased from 3 years to 5 years.

- PAN to be obtained by all entities including HUF other than individuals in case aggregate of financial transaction in a year is Rs 2, 50,000 or more. All directors, partners, members of such entities also to obtain PAN.

- All companies irrespective of income to file the return and in case it is not filed, such companies will be liable for prosecution irrespective of the fact whether it has a tax liability of Rs 3,000 or not.

Provisions

- Provision of Section 43CA, 50C and 56(2) (x) being amended to allow 5% of sale consideration in variation vis a Vis stamp duty value. On account of location, disadvantage etc.

- Provision of sections 40(IA) and 40A (3) and 40A (3A) are being made applicable to Charitable Trust. Hence expenditure incurred without deduction of tax and in cash will not be eligible as the application of income under section 10(23C) and section 11(1) (a).

- Deemed dividend to be taxed in the hands of the company itself as Dividend Distribution of tax @ 30%.

- Penalty for non-filing financial return as required under section 285BA being increased to Rs 500 per day.

What is Capital Gain Exemption ?

Term of Capital gains exemption is referred to as benefit provided by the government to taxpayers, easing the burden of paying tax on capital gains, The requirement to pay capital gains tax arises when a taxpayer sells an asset (other than personal property and stock used in the business) for a profit.

Income tax rate in case of capital Gain regulation in India