Amended rules for submission of Form 15CA & 15CB

Page Contents

Amended rules for submission of Form 15CA & 15CB

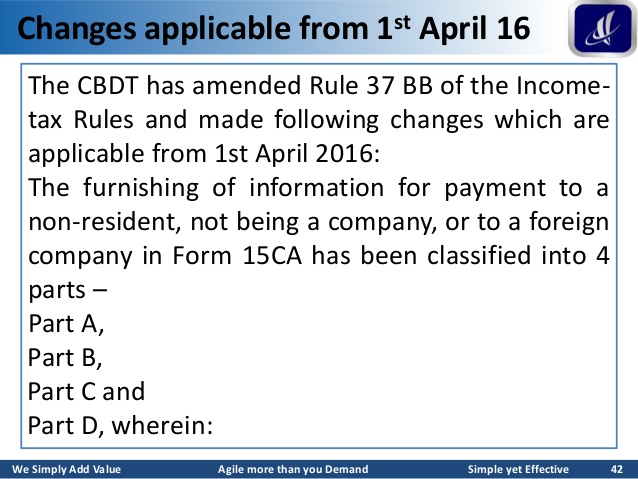

Rule 37BB of the IT Rules amended w.e.f.1st April 2016 to bring Major Changes in the Requirements of Form 15CA & 15CB and Foreign remittances covered under Sec 195: The Income Tax Depart amended the rules for the preparation and submission of Form 15CA & Form 15CB. The revised rules became effective as of 1.04.2016. The big changes are as follows

- Form 15CA & 15CB not to be furnished by an individual for remittance which does not require RBI approval.

- CA certificate in Form No.15CB will be required for taxable payments exceeding Rs.5 Lac made to non-residents during a Financial Year.

- The list of payments of a specified nature referred to in Rule 37BB, which do not require the submission of Forms 15CA and 15CB, has been extended from 28 to 33, which include payments for imports details mentioned below:

Brief requirement of 15CA and 15CB?

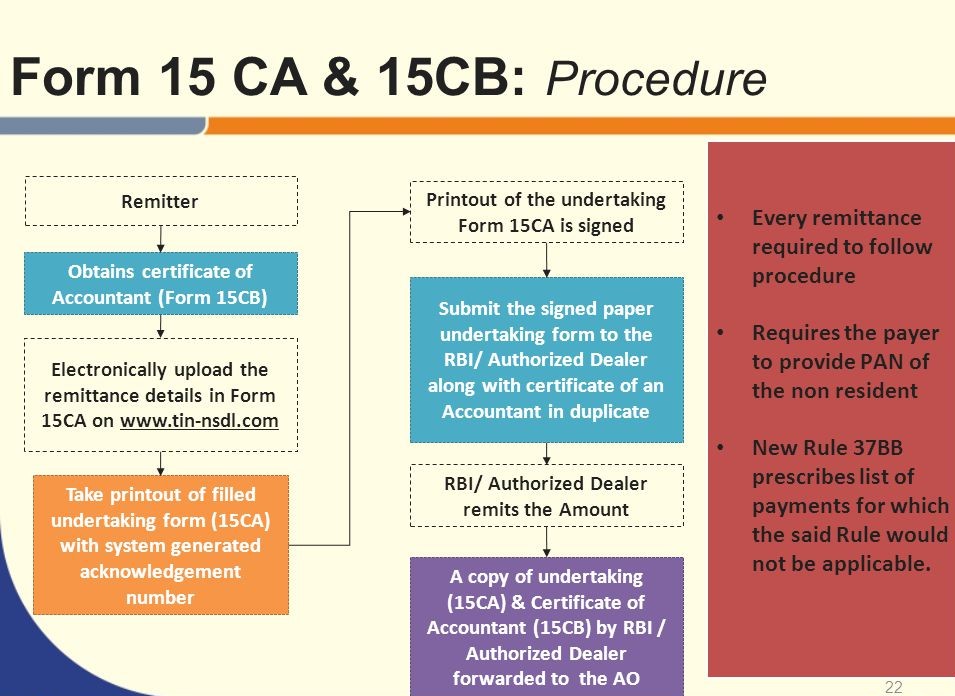

- Form15CA is a declaration issued by the Remitter and is used as a tool by statutory authorities to collect information on payments that are subject to tax in the hands of non-resident recipients.

- Form15CB-A person who makes a payment must receive a certificate from a chartered accountant in the form 15CB.

- A person seeking to make a payment to a non-resident or foreign company must conform to the requirements of Form 15CA & 15CB.

- Form15CB is the Income Tax Determination Certificate where the issuer Chartered Accountants examines the remittance as per the provisions of the IT Act 1961 & the provisions of the DTAA with the Recipient’s Residence Country.

What is Form 15CA?

Certain payments made by a resident to a Non-resident must be made under the IT ACT 1961. The concept behind the deduction and subsequent reporting of taxes at the source is to make sure that taxes are collected on time. Form 15CA is a declaration made by the person remitting the money, stating that he has TDS from any payments to the non-resident. Details format of Form 15CA

What is Form 15CB?

Form 15CB, fortunately, is not a declaration, but a certificate issued by the Chartered Accountant to ensure that the provisions of the Double Taxation Avoidance Agreement and the Income Tax Act were complied with in respect of tax deductions while making payments. Contains the following details

- Information & nature of payment made to a non-resident.

- Compliance with Article 195 of the I T Act 1961.

- Rate of TDS Deducted.

- Applicability of the DTAA.

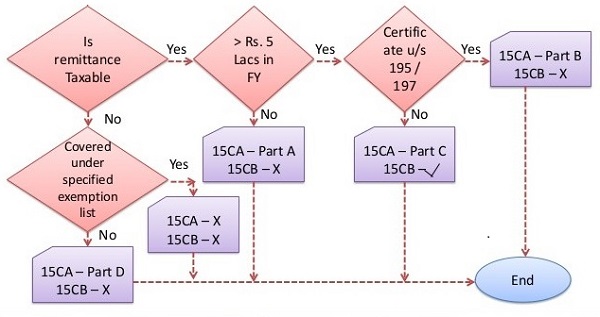

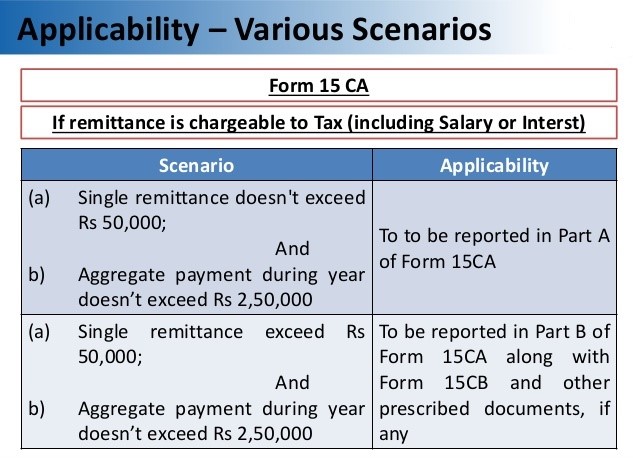

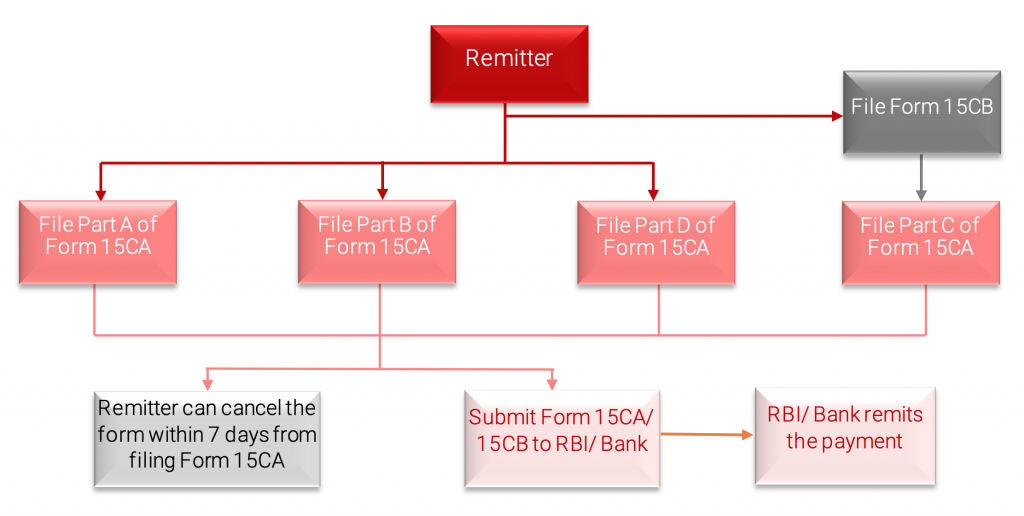

Applicability of 15CA

- If the amount of the remittance is not tax-chargeable, then-No Forms 15CA are required.

- If the remittance falls within the scope of the prescribed exemption list, only Part D of Form 15CA shall be submitted.

- Where the remittance in a particular financial year is less than INR 5,00,000/– Only Form 15CA—Part A to be submitted

- Unless the remittance exceeds INR 5,00,000/– Form 15CA – Part C and Form 15CB to be issued

- Where even the remittance exceeds Rs. 5 lakhs and the certificate referred to in Section 195(2)/195(3)/197 of the Income Tax has been obtained Form 15CA – Part B that is to be submitted.

Kind of Parts in the Form 15CA

The form is divided into 4 parts to be filled out on the basis of a circumstance that is relevant at the time. There are 4 parts –

Part B of 15CA

- To be completed when the Certificate under Section 195(2)/195(3)/197 of the Income Tax Act has been obtained from the Assessing Officer.

Part C of 15CA

- To be filled if the remittance or its cumulative exceeds INR 5,00,000/- in the FY. and the remittance is subject to tax.

Part D of 15CA

- If, as issued for in domestic law, the remittance is not subject to income tax.

FAQ’s On Form 15CA & CA certificate Form 15CB

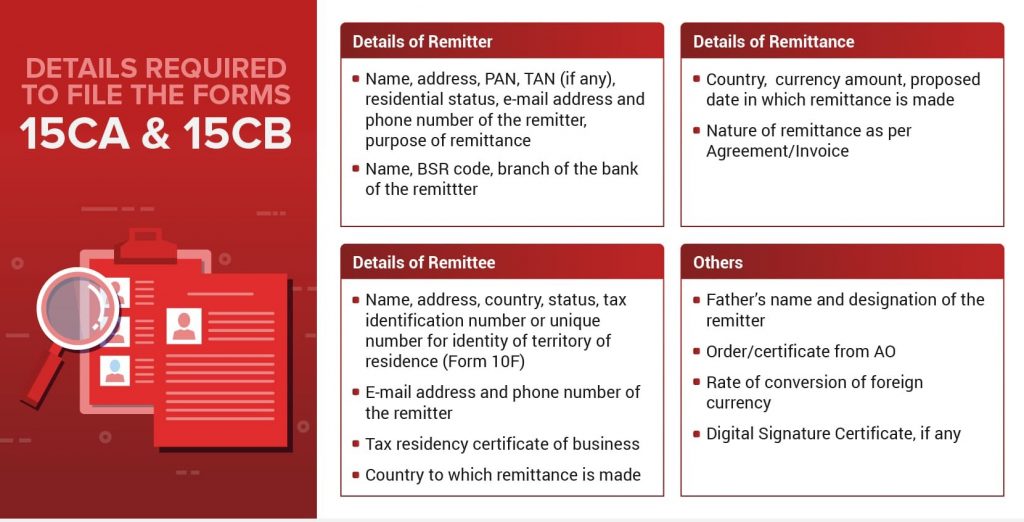

Q1. : What are the details required for filling Form 15CA 15CB?

Ans : Here are all the details

The person responsible for making the payment to a non-resident or a foreign company must provide the following details

www.carajput.com: Details-required-to-file-the-forms-15CA-15CB

Q2. When the Person required to made payment is made below Rs 5 lakh

- Information on such payments is needed in Part A of Form 15CA

Q3. When a person required to make payment is made more than Rs 5 lakh

- Certificate from the Accountant in Form 15CB

- Form 15CA Part C

- Part B of Form 15CA must be provided

Q4. Where payment is not subject to tax under the IT Act

- Form 15CA Part D

- In the following circumstances, no information is needed

- The remittance shall be made by an individual and shall not require the prior approval of the RBI [as provided for in Section 5 of the FEMA, 1999 (42 of 1999) as set out in Schedule III of the FEMA Regulations, 2000].

As per Rule 37BB: The remittance shall be of the nature specified in the following list:

| Advance payment against imports | |

| Payment towards imports-settlement of invoice | |

| Imports by diplomatic missions | |

| Intermediary trade | |

| Imports below INR 5,00,000-(For use by ECD offices) | |

| Travel for pilgrimage | |

| Travel for medical treatment | |

| Freight insurance – relating to import and export of goods | |

| Payments for maintenance of offices abroad | |

| Maintenance of Indian embassies abroad | |

| Remittances by foreign embassies in India | |

| Remittance by non-residents towards family maintenance and savings | |

| Booking of passages abroad -Airlines companies | |

| Remittance towards business travel. | |

| Travel under basic travel quota (BTQ) | |

| Contributions or donations by the Government to international institutions | |

| Indian investment abroad -in subsidiaries and associates | |

| Indian investment abroad -in real estate | |

| Loans extended to Non-Residents | |

| Operating expenses of Indian Airlines companies operating abroad | |

| Remittance towards donations to religious and charitable institutions abroad | |

| Remittance towards grants and donations to other Governments and charitable institutions established by the Governments. | |

| Payment- for operating expenses of Indian shipping companies operating abroad. | |

| Remittance towards personal gifts and donations | |

| Remittance towards payment or refund of taxes. | |

| Refunds or rebates or reduction in invoice value on account of exports | |

| Payments by residents for international bidding. | |

| Travel for education (including fees, hostel expenses etc.) | |

| Indian investment abroad-in branches and WOS (Wholly owned subsidiaries) | |

| Construction of projects abroad by Indian companies including import of goods at project site | |

| Indian investment abroad -in equity capital (shares) | |

| Indian investment abroad -in debt securities | |

| Postal Services |

Q5. What are the implications for the non-filing of Form 15CA 15CB?

If the Assessor who is supposed to file Form 15CA 15CB fails to provide the same information prior to the transfer to a non-resident, the Assessor shall be liable for penalties regulations in accordance with Section 271I of the I T Act 1961.

Such an unlawful provision shall be attracted even if the person has provided incorrect information. The amount of penalty that the Assessing Officer may ask the Assessor to pay for non-compliance is Rs.1lakhs.

Q6 Can be revised or canceled Form 15CA Form 15CB

Yes, Form 15CA may be withdrawn within 7 days from the date of submitting. The respective link to withdraw the file form will be available on the Income-tax portal of the Assessee relevant concerned.

For query or help, contact: singh@carajput.com or call at 9555555480

Popular blog:-