What is Income Tax Audit Limit ?

Page Contents

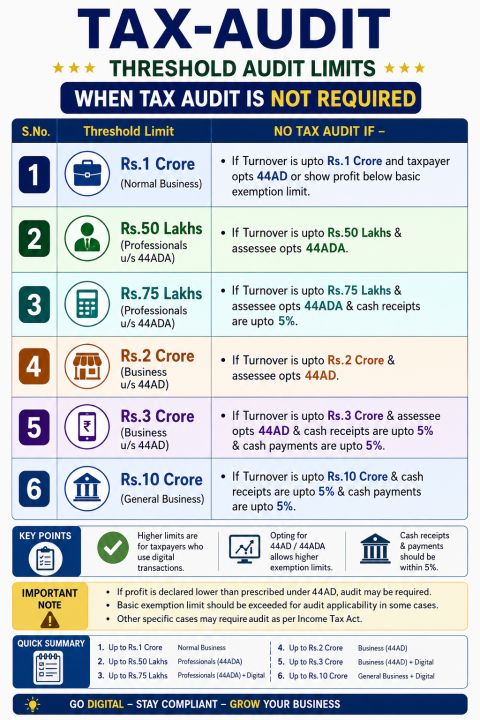

Tax Audit Limits Explained (FY 2025–26)

Tax Audit: A tax audit means accounts must be checked and certified by a chartered accountant u/s 44AB. When a tax audit under the Income Tax Act is NOT required, based on turnover, type of taxpayer, and conditions. A tax audit is no longer only about turnover; it depends heavily on the scheme opted for (44AD/44ADA), cash transactions, and profit declared.

Tax audit applicability = Turnover + Scheme + Cash % + Profit declared.

A small mistake (wrong scheme or underreporting profit) → Audit + Penalty + Notice

Presumptive Taxation: Instead of maintaining detailed books

- 44AD (Business): Profit deemed @6%–8%

- 44ADA (Professionals): Profit deemed @50%

This helps avoid audits and simplify compliance

- An audit may still be required if the taxpayer declares profit lower than prescribed %

- AND your income exceeds basic exemption limit

- Other audit cases: As per other sections (like 44AB clauses)

- Cash condition is very important: Cash receipts & payments must be ≤ 5% to get higher limits

Normal Business – INR 1 Crore Limit

- No audit required if:

- Turnover ≤ INR 1 crore

- OR profit declared under Section 44AD (presumptive taxation)

If turnover exceeds INR 1 crore → Audit required (unless eligible for higher digital limits).

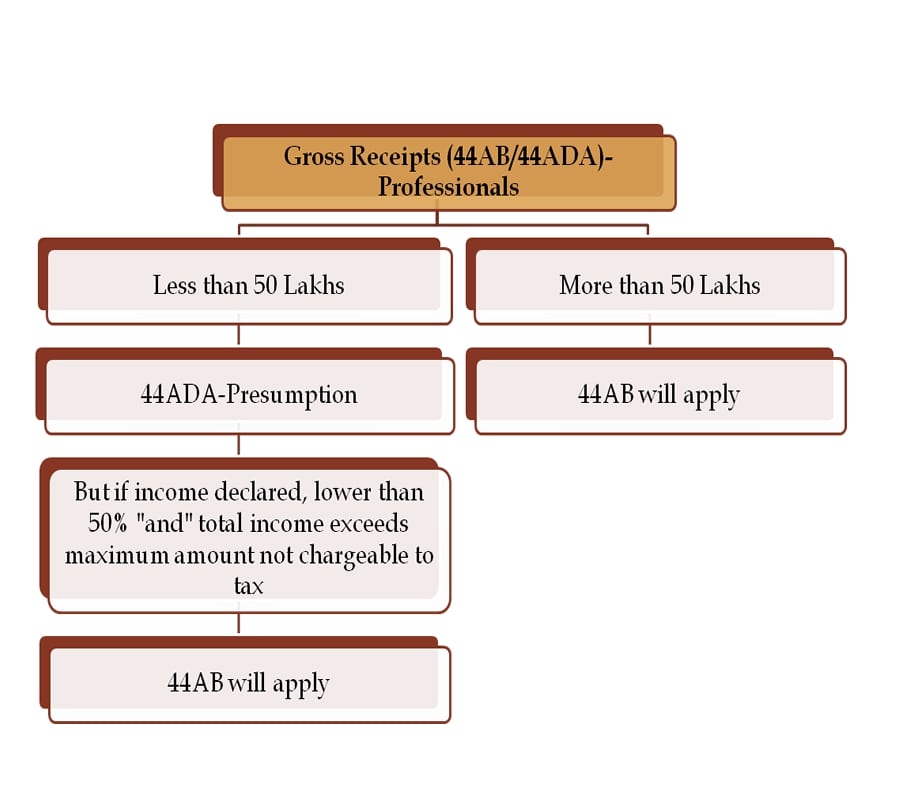

Professionals (Section 44ADA)—INR 50 Lakhs

- No audit required if:

- Gross receipts ≤ INR 50 lakh

- And taxpayer opts for 44ADA (presumptive scheme)

If receipts exceed INR 50 lakh → Audit required

Professionals (Digital Benefit)—INR 75 Lakhs

- No audit if:

- Receipts ≤ INR 75 lakh

- AND cash receipts ≤ 5%

A benefit is given for digital transactions

Business (Section 44AD) – INR 2 Crore

- No audit if:

- Turnover ≤ INR 2 crore

- And taxpayer opts for 44AD

This is basic presumptive scheme limit

Business (Digital Benefit) – INR 3 Crore

- No audit if:

- Turnover ≤ INR 3 crore

- AND:

- Cash receipts ≤ 5%

- Cash payments ≤ 5%

Higher limit for digital businesses

General Business – INR 10 Crore

- No audit if:

- Turnover ≤ INR 10 crore

- AND:

- Cash receipts ≤ 5%

- Cash payments ≤ 5%

Maximum relaxation for fully digital businesses

If a person is involved in a profession & chooses presumptive taxation under section 44ADA:

| Last year’s aggregate turnover, sales, or gross receipts limit | Profit Amount with respect to turnover (in %) | Status of Applicability of Tax Audit on Assesses |

| Excess than INR Fifty Lakhs | N.A. | Yes, a tax audit is applicable U/s 44AB(b) |

| Upto INR Fifty Lakhs | More than 50% | NO |

| Upto INR Fifty Lakhs | less than 50% (Under Section 44ADA) | Yes, a tax audit is applicable U/s 44AB(d) |

Specified professions—Sec 44AA.

U/s 44AA of the Income Tax Act, certain occupations are classified as “specified professions,” for which maintenance of books of accounts is mandatory. These include:

- Professional services rendered in the field of engineering, such as consulting engineers, structural engineers, and those engaged in technical certification, design, and drafting services. The legal profession covers services provided by advocates and law firms. Other specified professions include company secretaries, cost accountants, and chartered accountants.

- The medical profession comprises doctors and other healthcare practitioners. Services related to interior decoration, including planning, designing, and consulting, are also covered. The advertising profession, along with activities of film artists such as directors, actors, and cameramen, falls within this category.

- Further, the architectural profession includes services provided by architects and architectural firms. The scope also extends to technical consultancy, covering professionals such as business and marketing consultants.

- An authorised representative, being a person who represents another individual before any tribunal or authority for a fee, is also included. Additionally, sports professionals—including players, coaches, trainers, physiotherapists, commentators, umpires, event managers, and sports writers—are recognised under specified professions.

If a person is involved in business & chooses presumptive taxation U/s 44AD:

| Last year’s turnover limit | Profit Amount with respect to turnover (in %) | In case cash receipts less than 5 percent of Turnover | In case cash payment less than 5 percent of total payment | Status of Applicability of Tax Audit |

| Exceeds INR Ten Cr. | N. A. | N. A. | N. A. | Yes, a tax audit is applicable |

| Exceeds than INR Two Cr but is up to INR Ten Cr | N. A. | Yes | Yes | No |

| Exceeds than Two Cr but upto INR Ten Cr | N. A. | No | No | Yes, Tax Audit is applicable |

| Exceeds one Cr but upto Two Cr | Excess than 8 percent or 6 percent of Turnover | N. A. | N. A. | No |

| Exceeds than INR One Cr but upto Two Cr | Less than 8 percent or 6 percent of Turnover | N. A. | N. A. | Yes, a tax audit is applicable. |

| Less than INR One Crore | More than 8 percent or 6 percent of Turnover | N. A. | N. A. | No |

| Less than INR One Crore | Less than 8 percent or 6 percent of Turnover | N. A. | N. A. | Yes, a tax audit is applicable |

Key Note:

- If total income is more than the basic exemption limit, only then is a tax audit applicable.

- Where the income taxpayer is covered under section 44AB, then he is required to get the books of accounts audited by a CA.

- Income tax Audit report would be furnished under the form 3CB CD, where a report of a tax audit complete by the CA is to be filed in Form No. 3CB & details of the audit are to be reported in Form No. 3CD.

- In case the income taxpayer is liable for income tax & that person fails to complete the tax audit of the firm’s books of accounts, then he is responsible for a payment of penalty of the lower of the two below:

- Rs. 150,000 or

- 0.5 percent of total receipts.

Quick Summary of Tax Audit Limits Explained (FY 2025–26)

| Category | Limit | Condition |

| Business (Normal) | INR 1 Cr | Basic |

| Professionals | INR 50 L | 44ADA |

| Professionals (Digital) | INR 75 L | Cash ≤ 5% |

| Business (44AD) | INR 2 Cr | Presumptive |

| Business (Digital) | INR 3 Cr | Cash ≤ 5% |

| Business (General Digital) | INR 10 Cr | Cash ≤ 5% |

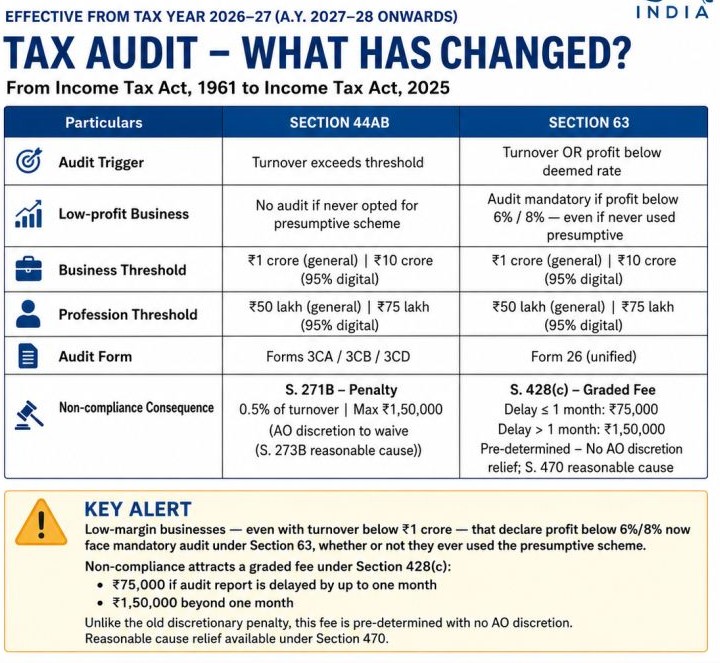

New Criteria for Tax Audit Applicability under Income Tax Act, 2025

Key Highlights of Tax Audit Changes in Income Tax Act, 2025

Earlier under Section 44AB (1961 Act), the audit was primarily based on turnover thresholds

Now under Section 63 (Income Tax Act, 2025): An audit is required if turnover exceeds prescribed limits OR profit is below the prescribed presumptive rate (6% / 8%). This means even businesses with turnover below ₹1 crore may require an audit if profits are low.

Tax Audit Changes for Businesses: Affected Groups: Small traders, retail businesses, contractors, and startups with low profit margins. Tax audits may have compliance issues. Impact like Higher audit coverage, Increased documentation requirements, Need for accurate bookkeeping and early planning before ITR filing. Businesses must reassess their audit position if

- Turnover is below INR 1 crore

- Profit margins are below 6% / 8%

Such businesses may now fall under mandatory tax audit, even if they were previously exempt.

Major Shift for Low-Profit Businesses

Under the old law, if a taxpayer never opted for presumptive taxation, an audit was generally not triggered based on profit level. Under the new law:

- Audit becomes mandatory if profit < 6% / 8%

- Applicable even if presumptive taxation was never adopted

This significantly expands audit coverage to Low-margin businesses, Cash-intensive industries and Startup / early-stage businesses

Old vs New Tax Audit Framework under Income Tax Act, 2025

| Particulars | Income Tax Act, 1961 | Income Tax Act, 2025 |

| Audit Trigger | Turnover exceeds threshold | Turnover OR low profit |

| Low Profit Case | No audit if presumptive not opted | Audit mandatory if profit < 6% / 8% |

| Audit Forms | 3CA / 3CB / 3CD | Unified Form 26 |

| Penalty | 0.5% of turnover (max ₹1.5 lakh) | Fixed graded fee |

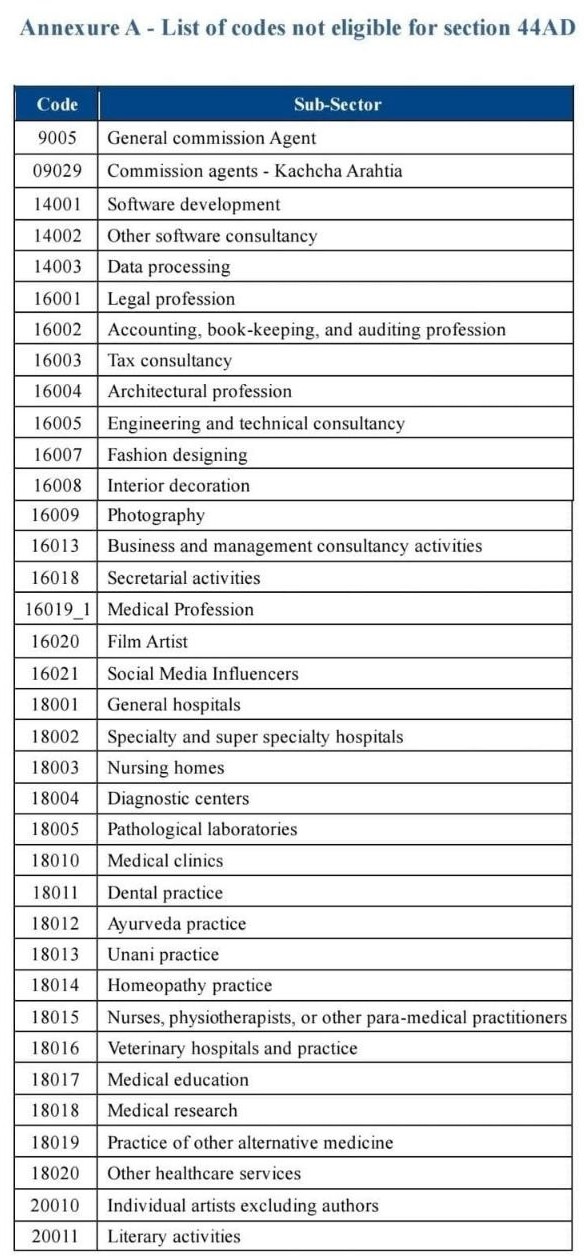

𝐋𝐢𝐬𝐭 𝐨𝐟 𝐜𝐨𝐝𝐞𝐬 𝐧𝐨𝐭 𝐞𝐥𝐢𝐠𝐢𝐛𝐥𝐞 𝐟𝐨𝐫 𝐒𝐞𝐜𝐭𝐢𝐨𝐧 𝟒𝟒𝐀𝐃 𝐩𝐫𝐞𝐬𝐮𝐦𝐩𝐭𝐢𝐯𝐞 𝐭𝐚𝐱𝐚𝐭𝐢𝐨𝐧

lists business/profession codes not eligible for presumptive taxation under Section 44AD because Section 44AD is generally available for eligible businesses and not for specified professions covered under Section 44AA(1). The codes shown are:

Commission Agents

- 9005 – General Commission Agent

- 09029 – Commission Agents (Kachcha Arhatia)

Software & IT Services

- 14001 – Software Development

- 14002 – Other Software Consultancy

- 14003 – Data Processing

Professional Services

- 16001 – Legal Profession

- 16002 – Accounting, Book-keeping and Auditing Profession

- 16003 – Tax Consultancy

- 16004 – Architectural Profession

- 16005 – Engineering and Technical Consultancy

- 16007 – Fashion Designing

- 16008 – Interior Decoration

- 16009 – Photography

- 16013 – Business and Management Consultancy Activities

- 16018 – Secretarial Activities

- 16019_1 – Medical Profession

- 16020 – Film Artist

- 16021 – Social Media Influencers

Healthcare Services

- 18001 – General Hospitals

- 18002 – Specialty and Super Specialty Hospitals

- 18003 – Nursing Homes

- 18004 – Diagnostic Centres

- 18005 – Pathological Laboratories

- 18010 – Medical Clinics

- 18011 – Dental Practice

- 18012 – Ayurveda Practice

- 18013 – Unani Practice

- 18014 – Homeopathy Practice

- 18015 – Nurses, Physiotherapists and Other Para-medical Practitioners

- 18016 – Veterinary Hospitals and Practice

- 18017 – Medical Education

- 18018 – Medical Research

- 18019 – Practice of Other Alternative Medicine

- 18020 – Other Healthcare Services

Artists & Authors

- 20010 – Individual Artists (excluding Authors)

- 20011 – Literary Activities

Important Note: These activities are generally not eligible for Section 44AD. Depending on the nature of the activity, many of them may instead be covered under Section 44ADA (for specified professionals with gross receipts up to the prescribed limit), subject to satisfaction of applicable conditions under the Income-tax Act. For CAs, advocates, doctors, architects, engineers, interior decorators, technical consultants, film artists, and other notified professionals, Section 44ADA is the relevant presumptive taxation provision rather than Section 44AD.

Introduction of Unified Audit Form 26

The new law replaces multiple audit forms: Forms 3CA / 3CB / 3CD. With a single: Form 26 (Unified Audit Report). Benefits of New Tax Audit Simplified compliance, Standardized reporting and Reduced complexity.

Graded Fee for Delay in Audit Report

A major structural change is the replacement of penalties with fixed fees. New Fee Structure:

- INR 75,000 → Delay up to 1 month

- INR 150,000 → Delay beyond 1 month

Key Difference in Tax Audit: Fee is predetermined and no discretionary relief by the Assessing Officer (AO). Earlier: Penalty depended on AO discretion; Now Strict and predictable compliance cost

Relief Provision as per Tax Audit Changes: Although fees are fixed. Relief may still be available in genuine cases under reasonable cause provisions; however, the flexibility is significantly reduced.

No Penalty for Failure of Tax Audit U/s 271B in Case of Reasonable Causes with Case Laws.

- If the tax audit report is not submitted on time or before the deadline, no penalty under section 271B will be enforced. The provisions of section 271B must be applied, however, if the audit report is not submitted by the deadline.

- No Penalty for Failure of Tax Audit under section 271B of the Income Tax Act, 1961, in case of Reasonable Causes with Case Laws

Hope the information will assist you in your professional endeavors. For query or help, contact: singh@carajput.com or call at 9555555480

Popular blog: