UDIN Dashboard for Tax Audit Assignments w.e.f. 1 April 2026

Page Contents

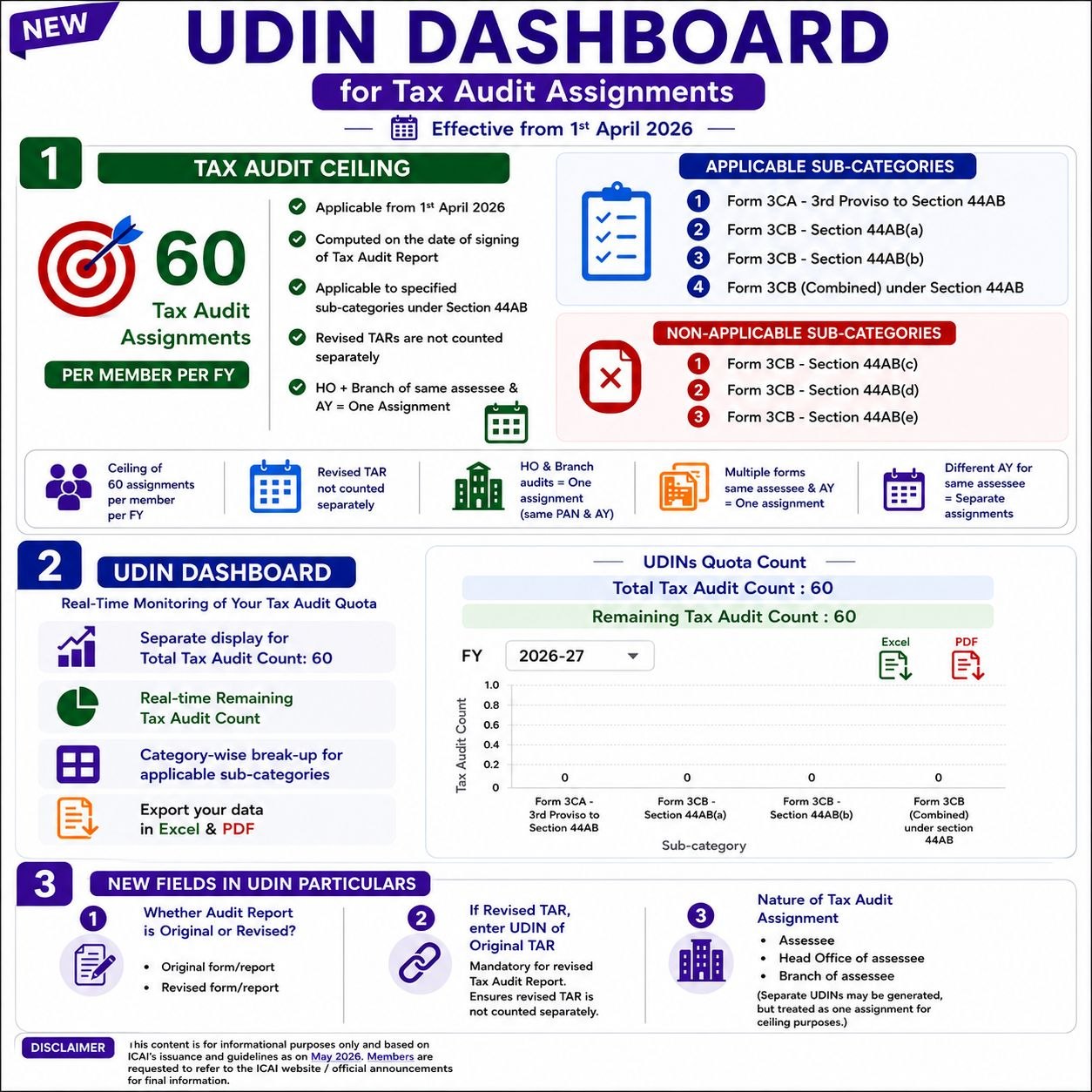

New UDIN Dashboard for Tax Audit Assignments (Effective from 1 April 2026)

This blog explains the new Unique Document Identification Number Dashboard introduced for monitoring tax audit assignments under Section 44AB and tracking the tax audit ceiling applicable to chartered accountants. The Unique Document Identification Number Dashboard is intended to give chartered accountants a transparent mechanism to monitor tax audit limits and ensure compliance with the ceiling prescribed for tax audit assignments

Tax Audit Ceiling

60 Assignments per Member per Financial Year: The dashboard introduces a maximum ceiling of 60 tax audit assignments per member for each financial year. Important features are as follows:

- Effective from 1 April 2026

- The count is computed on the date of signing the Tax Audit Report (TAR)

- Applicable only to specified tax audit categories under Section 44AB

- Revised Tax Audit Reports (TARs) are not counted separately

- Head Office and Branch audit of the same assessee and same Assessment Year are treated as one assignment

- Multiple forms relating to the same assessee and same Assessment Year are treated as one assignment

- Different Assessment Years for the same assessee are counted as separate assignments

Applicable Categories Included in Ceiling:

The following tax audit assignments will count toward the 60-audit limit:

Form 3CA: Audit covered under the 3rd Proviso to Section 44AB

Income tax Form 3CB – Section 44AB(a) : Business audit under specified turnover limits

Form 3CB – Section 44AB(b) : Professional receipts crossing prescribed limits

Income tax Form 3CB (Combined) under Section 44AB : These categories are reflected in the Unique Document Identification Number Dashboard count.

Categories Not Counted in the Ceiling: The following categories are shown as non-applicable in the image:

- Form 3CB – Section 44AB(c)

- income tax Form 3CB – Section 44AB(d)

- Form 3CB – Section 44AB(e)

- These audits will not be included in the dashboard count according to the infographic.

Unique Document Identification Number Dashboard Features:

The dashboard provides real-time monitoring of tax audit utilization. Information Available and Total Tax Audit Count. Shows total allowable tax audit assignments. Example shown: Total Tax Audit Count: 60. Remaining Tax Audit Count: Displays the balance audits available for acceptance.

Example shown: Remaining Count: 60

-

- Category-wise Breakup: Separate counts are available for Form 3CA, Form 3CB (44AB(a)), Form 3CB (44AB(b)), and the Combined Form 3CB.

- FY Selection: Member can select the relevant Financial Year, such as FY 2026-27

- Export Facility: Dashboard data can be downloaded in Excel, PDF.

- Example of Counting Assignments:

-

-

- Example-1: One assessee head office audit, branch audit, then same PAN and same AY. Then Count = 1 Assignment

- Example-2: One assessee, Form 3CB, Revised Form 3CB, then Count = 1 Assignment. The revised report will not increase the count.

- Example 3: Same assessee AY 2025-26 and AY 2026-27, then it will count as 2 assignments. Different assessment years are counted separately.

-

New Fields Added in Unique Document Identification Number Particulars:

Here are highlights of three important additional disclosures.

Whether the audit report is original or revised: Members must specify “Original Tax Audit Report” and “Revised Tax Audit Report.” This helps the system distinguish fresh audits from revised reports.

- Unique Document Identification Number of Original Tax Audit Reports: Where a revised TAR is issued Unique Document Identification The number of the original TAR must be entered and be mandatory in revised TAR cases. Purpose: To avoid duplicate counting and track revision history.

- Nature of Tax Audit Assignment: The member must specify whether the assignment relates to Assessee : Regular tax audit assignment, Head Office of Assessee :Audit relating to the Head Office. And Branch of Assessee : Audit relating to a branch.

Although separate unique document identification numbers may be generated, they are treated as one assignment for ceiling purposes if the PAN and assessment year are the same.

Key Takeaways—For Chartered Accountants

- Maximum 60 tax audit assignments per financial year

- Real-time dashboard monitoring available

- Revised TARs do not consume additional quota

- Head Office and Branch audits of the same assessee count as one audit

- Original and revised reports must be identified separately

- Dashboard provides category-wise and remaining quota tracking

- Original Unique Document Identification Number mandatory while generating revised TAR Unique Document Identification Number