The dos & don’ts of Business Incorporation in India

Page Contents

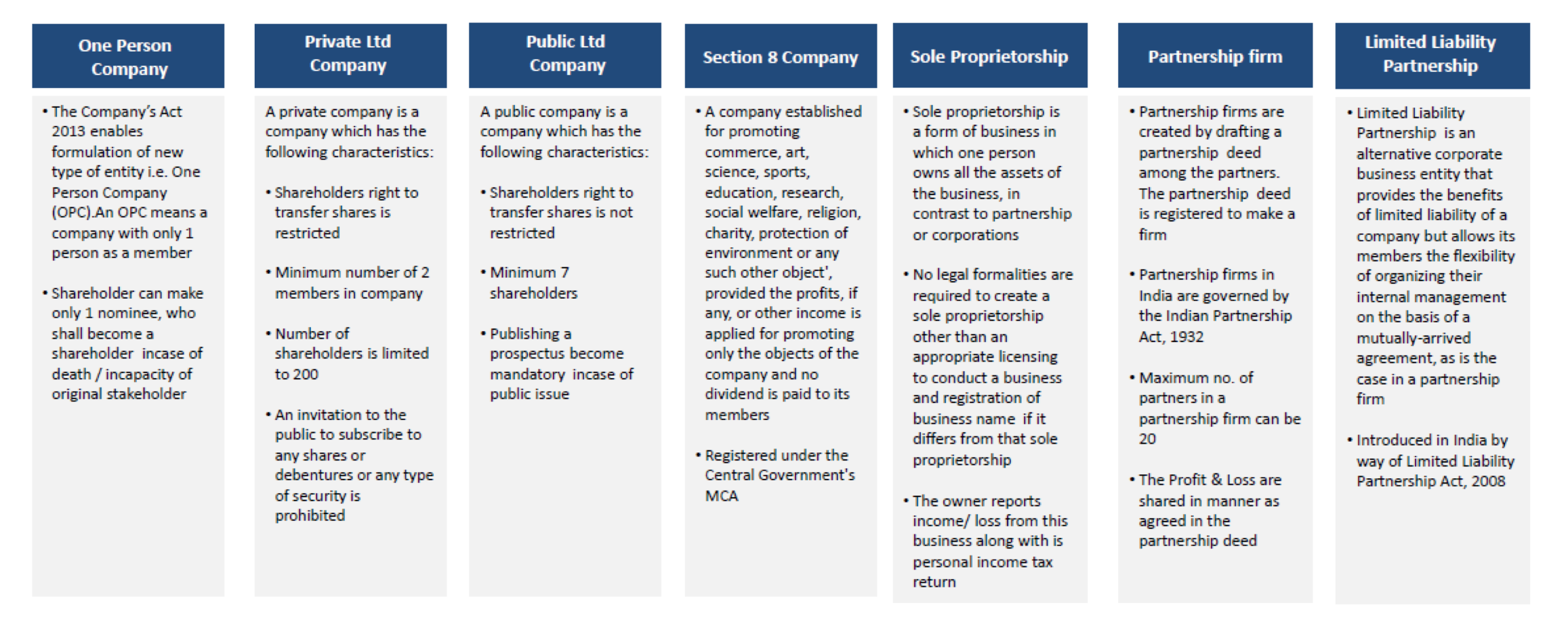

The dos & don’ts of business incorporation

It may initially appear difficult to start a formal company and incorporate your firm, especially when you have to take into account abiding by the various rules regulations surrounding incorporation guidelines for incorporation. incorporation of business has many benefits as well including as reduced liability in the event that your business gets sued or wishes to hire employee.

However, whether we want to incorporate or look at other choices for starting your own business, it’s important to understand what you need to do to get started the right way. This Post will go over many way that you can use to start a business, whether you decide to use them or not.

-

Trust

You can safeguard your interest in the property and start a business to benefit a particular beneficiary or beneficiaries if you establish a private trust. The establishment and administration of a trust are governed by the Indian Trust Act.

-

Nonprofit Organization

The Companies Act of 2013 also regulates the establishment and administration of nonprofit organizations. The public interest is safeguarded by “Section 8 companies,” which are prohibited from sharing earnings with their employees. People must register with the 2013 Companies Act in order to establish a NPO.

-

Solo Entrepreneurship

People who want to establish a business with small investment and are primarily looking for employment than the fist and foremost choose the sole proprietorship. Dealing with local suppliers is required, and these suppliers may be traders, Kirana shops, or wholesalers etc.

-

Partnership

When two or more persons decide to start a business and agree to give the enterprise resources like property, money or other assets based on a mutual understanding, a partnership is registered & formed.

Whether the partnership is registered is subject to debate. However, the formal form of partnership has many benefits over the unregistered firm, including priority in partner disputes and the capacity to sue other parties or ability to sue 3rd parties

- Limited Liability Company (LLP)

There is no specific amount of money required to establish an Limited Liability firm. With the safety of money comes the possibility to designate limited liability for partners and many other attractive advantages to enhance business operations.

An Limited Liability Company must also file an yearly MCA Return that which includes details of the holdings of partners, designated partners, & other Limited Liability Company operational details as required. MCA Form 8 of the yearly MCA return contains details about liabilities & assets along with operations.

Summary

- Whether to incorporate your business is one of the most significant and crucial decisions you will make during your business career. For some business owners, adding their company is the simplest and most prudent decision. After all, how much simpler could it be to establish an entity that legally divides you from your business if you want to protect yourself against being sued by a dissatisfied client or worker? There are additional possibilities for founding a Partnership firm besides just creating an Limited Liability Company , so incorporation isn’t as simple as some individuals may believe.

- It could be simple to lose track of all the documentation, contracts, and other procedures when getting ready to start your own company and Limited Liability Company. Incorporating a business is a crucial first step in launching any kind of business. Many large corporations may just take this one step, but other small and medium-sized enterprises should do the same if they want to be intelligent and forward-thinking.